The practical answer

- Short answer

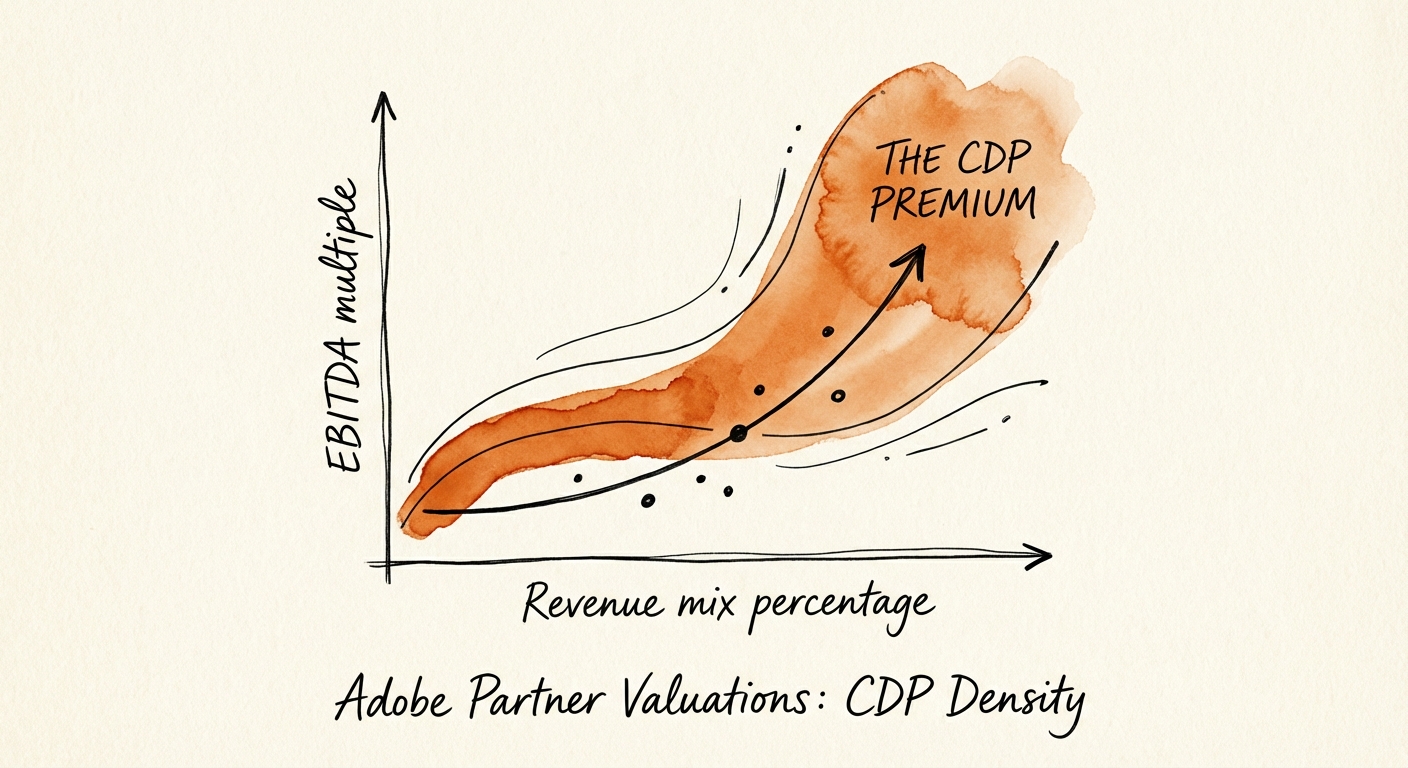

- Why Adobe Real-Time CDP specialists command 14x EBITDA multiples while AEM generalists stall at 8x. M&A benchmarks for Adobe partners in 2026.

- Best fit

- Industry: Professional Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for Adobe partners with >40% revenue from Real-Time CDP / AEP projects.

The 'Content Supply Chain' is a Commodity; The Data Layer is the Gold Mine

For the last decade, the Adobe partner ecosystem was defined by one dominant acronym: AEM. If you could implement Adobe Experience Manager at scale for the Fortune 500, you had a license to print money. The labor arbitrage was simple: hire Java developers, train them on AEM components, and bill them out at $225/hour. But in 2026, the 'Content Supply Chain' has become a race to the bottom.

Generative AI and 'Agentic' workflows are rapidly commoditizing the production and management of content. What was once a high-margin technical service—building custom AEM components and templates—is now being automated by Adobe’s own Firefly and Sensei capabilities. As a result, 'Classic' AEM agencies are seeing valuation multiples compress from 10x-12x down to 6x-8x EBITDA.

The smart money in Private Equity has moved down the stack. They are no longer buying the 'Face' of the experience (Content); they are buying the 'Brain' (Data). This is the CDP Premium. Partners who specialize in Adobe Real-Time CDP (RT-CDP) and Adobe Experience Platform (AEP) are trading at 12x-15x EBITDA. Why? Because while content is ephemeral and increasingly automated, unified customer profiles are the persistent, defensive asset of the enterprise.

The Valuation Bifurcation: Creative vs. Data

We are witnessing a sharp bifurcation in the Adobe partner market. On one side, you have the 'Creative Implementation' shops—these firms focus on AEM Sites, Assets, and Workfront. They compete on rate cards and capacity. On the other side, you have 'Data Architecture' consultancies—firms that implement Real-Time CDP, Customer Journey Analytics (CJA), and AEP. They compete on intellectual property and architectural authority.

According to our 2025 IT Services M&A data, the multiple gap is widening:

- Generalist AEM Partner: 6x - 8x EBITDA (High competition, rate pressure)

- AEP / CDP Specialist: 12x - 15x EBITDA (Scarcity premium, strategic stickiness)

The days of trading at 10x EBITDA for implementing AEM Sites are over. The 'Content Supply Chain' is a race to the bottom. The alpha in the Adobe ecosystem has moved to the data layer—Real-Time CDP is the new system of record.

The Mechanics of the Premium: Why AEP Drives Higher Multiples

Private Equity investors aren't paying a premium for 'better' code; they are paying for stickiness and scarcity. An AEM implementation can be ripped and replaced. A website redesign happens every 3-4 years. But a Real-Time CDP implementation rewires the fundamental data architecture of the enterprise. It connects online behavior, offline POS data, call center interactions, and ad exposure into a single 'Golden Record'. Once a partner is the architect of that record, they are effectively impossible to displace.

This 'Data Gravity' creates a moat that justifies the higher multiple. Furthermore, the talent supply/demand curve is broken. While there are thousands of certified AEM developers globally, there is a severe shortage of AEP Architects who understand data schemas, identity resolution, and privacy governance. This scarcity allows CDP specialists to command bill rates 40% higher than their AEM counterparts, driving superior gross margins.

Benchmarks: The 'CDP Density' Metric

When we evaluate Adobe partners for exit, we look at 'CDP Density'—the percentage of revenue derived from Data & Insights projects vs. Content projects. The correlation with valuation is stark:

- < 15% Data Revenue: The 'Agency' Discount. Buyers view you as a staffing firm. Valuation ceiling: 7x.

- 15% - 35% Data Revenue: The 'Hybrid' Zone. You have capabilities, but lack authority. Valuation range: 8x - 10x.

- > 40% Data Revenue: The 'CDP Premium'. You are viewed as a strategic data consultancy. Valuation floor: 12x.

This is similar to the trend we see in the Snowflake partner ecosystem, where 'Data Product' shops trade at nearly double the multiple of 'Body Shop' integrators.

Strategic Pivot: Moving from Campaigns to Journeys

If you are a PE operating partner running an Adobe practice stuck in the 'AEM Trap,' you cannot simply hire your way out. You must fundamentally restructure your GTM and delivery models. The pivot requires moving from 'Campaign-based' revenue (launching a site, running a promo) to 'Journey-based' revenue (optimizing perpetual customer lifecycles).

1. Re-skill Your Architects: Your Lead AEM Architects need to become AEP Architects. The shift is from 'Pages and Components' to 'XDM Schemas and Datasets.' This is non-trivial. It requires understanding data lineage, governance, and identity graphs—skills often found in marketing agency analytics teams but rarely in engineering pods.

2. Productize Your Identity Models: The highest-value partners have pre-built 'Industry Data Models' for Retail, FinTech, or Healthcare. Instead of starting from scratch, they deploy a pre-configured AEP schema that accelerates time-to-value. This IP is what convinces a buyer that you are a platform, not a service.

3. Audit Your Revenue Quality: Look at your top 10 accounts. Are you just the 'arms and legs' building pages? Or are you the 'brain' defining audiences? If you aren't managing the Real-Time CDP, you are at risk of being commoditized by a low-cost offshore vendor. As noted in our guide to customer concentration risk, being the 'strategic brain' is the only hedge against vendor consolidation.

The window to claim the CDP Premium is open, but closing. As AEP maturity increases, the 'Generalist' partners will catch up. For now, the 14x exit belongs to those who own the data layer.