The practical answer

- Short answer

- Is your biggest client killing your exit? New 2025 data shows customer concentration >30% triggers a 20-35% valuation discount. Here is the diagnostic for Salesforce partners.

- Best fit

- Industry: Private Equity / Tech Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 30% Concentration threshold that triggers a 20-35% valuation discount.

The 35% Valuation Haircut: The New Math of Concentration

You are looking at a Salesforce partner with $20M in revenue and $4M in EBITDA. On the surface, it’s a healthy asset ready for a platform acquisition or a strategic tuck-in. But dig one layer deeper into the revenue mix, and you find the 'Whale Trap': 40% of that revenue comes from a single enterprise logo. To a founder, this contract is a badge of honor—proof they can serve the Fortune 500. To you, the Operating Partner, it is a single point of failure that turns an asset into a liability.

In 2025-2026 due diligence cycles, we are seeing buyers treat high customer concentration not just as a risk factor, but as a direct valuation subtractor. Recent deal data indicates that single-customer concentration above 30% now triggers a weighted valuation discount of 20-35%. It is not just about a lower multiple; it is about deal structure. Buyers are shifting risk back to the seller, moving 40-50% of the purchase price from cash-at-close to contingent earn-outs tied specifically to that whale’s retention.

The Concentration Danger Zones

We classify revenue concentration into three risk tiers based on current PE buyer sentiment:

- Safe Zone (<10%): The Gold Standard. Buyers pay full platform multiples (e.g., 10-12x EBITDA). The revenue is viewed as diversified and resilient.

- The Warning Track (10-20%): Manageable, but invites scrutiny. Expect heightened due diligence on the specific contract terms (auto-renewal vs. termination for convenience) and a "stickiness analysis" to prove high switching costs.

- The Kill Zone (>30%): This is where the math breaks. If one client holds the power to wipe out your EBITDA margin overnight, you don’t own a business; you own a contract. Buyers will price it accordingly, often capping the multiple at 4-6x on the concentrated portion of earnings.

For a deeper dive on how acquirers analyze this, review our Customer Concentration Analysis Framework.

If one client holds the power to wipe out your EBITDA margin overnight, you don’t own a business; you own a contract. And in 2026, buyers are pricing contracts at a 35% discount.

The Double Dependency: Channel Risk in the Salesforce Ecosystem

Salesforce partners face a unique compounding variable that generic service firms do not: Channel Concentration. When we audit these businesses, we often find that the "Whale Client" was not acquired through organic marketing, but handed over by a specific Salesforce Account Executive (AE) or RVP. This creates a double dependency.

If 40% of revenue comes from one client, and that client relationship is effectively owned by a Salesforce AE who could change territories or leave tomorrow, the risk profile explodes. We call this "referral concentration." In pricing services acquisitions, savvy buyers will map revenue not just by end-customer, but by lead source.

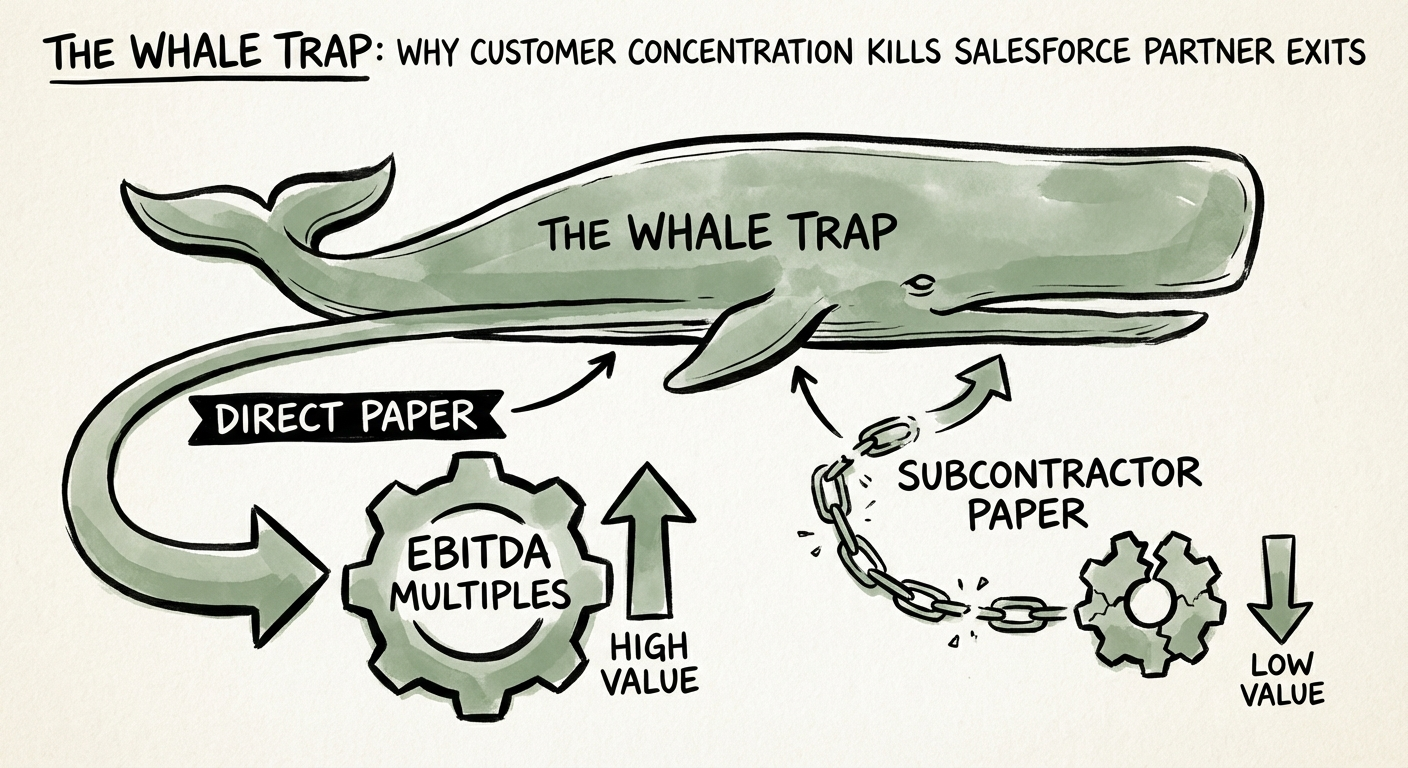

The "Paper" Problem

Another nuance is the contracting vehicle. Is the partner on "direct paper" (direct contract with the client) or "subcontractor paper" (under Salesforce Professional Services or a GSI)?

If your portfolio company is doing $10M a year as a subcontractor to a GSI or Salesforce itself, that revenue is treated as lower quality (Quality of Revenue). It commands a lower multiple because the partner does not own the customer relationship, the renewal, or the pricing leverage. In 2025, we are seeing valuations for "sub-paper" revenue trade at a 2x-3x turn discount compared to direct prime contracts. The market is effectively saying: "We pay for customer ownership, not just billable hours."

Remediation: Fixing the Mix Before the Sale

You cannot fire a whale client to fix your percentages—that kills EBITDA. But you can dilute them. If you are 18-24 months from an exit, the only mathematical way to escape the concentration penalty is to grow the rest of the business aggressively. This is where structuring the exit begins years before the LOI.

The "Ring-Fence" Strategy

If dilution isn’t possible in time, prepare a "Ring-Fence" defense for the negotiation table. Instead of accepting a blanket valuation discount, propose isolating the concentrated revenue.

- Tranche A (Diversified Revenue): Valued at the full market multiple (e.g., 10x).

- Tranche B (Whale Revenue): Valued separately, perhaps at a lower multiple (e.g., 4x) or subject to a specific earn-out.

This structure protects the valuation of the core business while acknowledging the specific risk of the large account. It signals to the buyer that you understand the risk and are willing to share it, rather than having them hammer the entire enterprise value.

Operational Inoculation

Finally, deepen the hooks. If a client is 30% of revenue, you need 100% of their wallet share. Ensure you are multi-threaded (working with IT, Sales Ops, and Marketing). If your relationship is single-threaded with one CIO, you are gambling the entire exit on one person's career. Buyers will interview that stakeholder during diligence; ensure they are an advocate, not a risk factor.