The practical answer

- Short answer

- Analysis of Zendesk partner growth milestones, valuation multiples, and the 'CX Premium' that drives 12x exits in 2026. A diagnostic for founders.

- Best fit

- Industry: Professional Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x EBITDA multiple for 'AI-Enabled' CX Partners (vs. 5x for implementation shops).

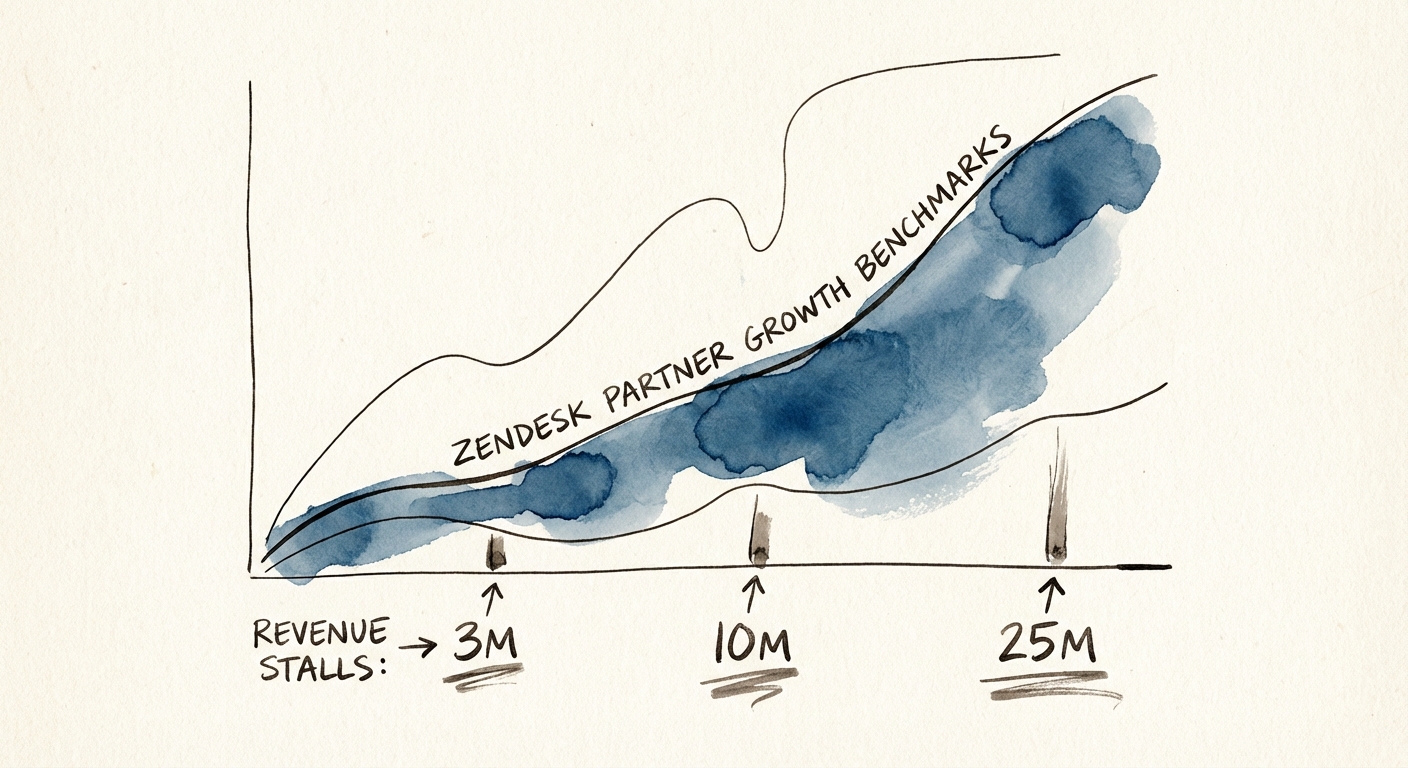

The Three Growth Stalls: From Help Desk to CX Strategy

In the Zendesk partner ecosystem, revenue growth is rarely linear. We observe a distinct staircase pattern where firms stall due to specific operational or strategic ceilings. In 2026, the gap between a "reseller" and a "strategic partner" is no longer just about margins—it is about existential relevance.

Stall 1: The $3M "Ticket Shop" Ceiling

At this stage, the firm is typically founder-led and reliant on high-volume, low-complexity implementations. The value proposition is technical: "We configure your queues and triggers." While profitable, this model hits a hard ceiling because it competes directly with Zendesk’s own Professional Services and low-cost offshore providers. The revenue per employee often stagnates at $150k, making it impossible to hire the mid-level management needed to scale.

Stall 2: The $10M "Generalist" Trap

Firms that break $3M often do so by broadening their service catalog—adding basic managed services or reselling third-party marketplace apps. However, they stall at $10M because they lack a differentiated "reason to buy" for enterprise clients. They are "Premier" partners by volume but "Generalists" by capability. In 2025, PE buyers are discounting these firms (trading at ~5-6x EBITDA) because their revenue is tied to "staff augmentation" rather than strategic IP.

Stall 3: The $25M "Platform" Transformation

To break $20M and approach $50M, a partner must pivot from "implementation" to "transformation." This means leading with Zendesk AI, autonomous agents, and workforce engagement management (WEM). Partners at this level are not fixing tickets; they are redesigning the client's entire customer journey. This shift requires a fundamentally different talent mix—data scientists and CX strategists instead of just system admins—but it unlocks the premium multiples seen in the Salesforce ecosystem.

Zendesk's push into AI Agents has created a bifurcation. You are either a mechanic fixing queues for $150/hour, or an architect designing autonomous service layers for 12x EBITDA.

The Valuation Bifurcation: The "AI Premium"

The 2025 market has bifurcated the valuation landscape for CX consultancies. Private equity firms and strategic acquirers (like Accenture or large GSIs) are no longer paying premiums for capacity. They are paying for capability—specifically, the ability to deploy and optimize AI Agents.

The "Mechanic" Discount (4x - 6x EBITDA)

Firms that focus primarily on Help Center setup, ticket routing, and license resale are viewed as commoditized service providers. Their revenue is non-recurring (project-based) and highly susceptible to churn if Zendesk automates the configuration process. Due diligence often reveals high customer concentration and low barriers to entry.

The "Architect" Premium (10x - 12x EBITDA)

Firms that position themselves as AI & CX Strategists command double the multiple. These partners:

- Deploy Zendesk AI Agents to deflect 30%+ of ticket volume (delivering measurable ROI).

- Integrate Zendesk with backend ERP/OMS systems (creating technical stickiness).

- Sell proprietary "Optimization" retainers rather than reactive support hours.

For an acquirer, the "Architect" provides a defensive moat. The client cannot leave because the partner owns the logic of the customer interaction, not just the settings.

The "Exit Ready" Operating Model

To command a 12x multiple, your P&L must reflect a strategic consultancy, not a VAR. Below are the benchmarks "Elite" partners hit before going to market.

1. Revenue Mix: The 40% Rule

Top-tier partners generate at least 40% of their gross profit from Managed Services and IP (e.g., proprietary connectors, AI tuning packages), not license resale. Resale margin is pass-through; Managed Services margin is enterprise value. If your "recurring revenue" is just software margin, you will fail the Quality of Earnings (QofE) analysis.

2. Utilization & Realization

While "Ticket Shops" run hot at 85% utilization (burning out staff), "Strategic Partners" aim for 72% utilization with higher bill rates ($250+/hr). This capacity buffer allows consultants to upskill on new Zendesk features (like Voice AI) without impacting delivery.

3. The "Trendsetter" Badge

Zendesk’s own 2025 classification of "CX Trendsetters" (companies adopting AI) is a proxy for partner value. Partners who can credibly demonstrate they have moved clients from "Traditional" to "Trendsetter" status (using AI to drive revenue, not just cut costs) are the primary targets for M&A activity in the 36-month exit window.