The practical answer

- Short answer

- Benchmarks for scaling a Workday partner practice from $10M to $50M. Revenue per employee, EBITDA targets, and the specialization strategy that drives 12x exit multiples.

- Best fit

- Industry: Professional Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x-14x Target EBITDA Multiple for specialized Workday partners >$40M revenue

The $12M Ceiling: Why Generalist HCM Shops Stall

In the Workday ecosystem, the climb from $0 to $10M is often fueled by the “rising tide” phenomenon. If you have a certified team and a pulse, the ecosystem’s 12-14% annual growth will carry you. Founder-led sales combined with relationship-based delivery work well here. But at $12M, the physics of the business break.

This is where we see the “Generalist Trap.” You built the firm on core HCM implementations, but that market has commoditized. Rates for generic HCM resources have stabilized, while the cost of talent continues to rise. If your firm is still essentially a staffing agency for HCM deployments, your EBITDA margins will begin to compress from a healthy 25% down to 15% as overhead creeps in.

The “Body Shop” Discount on Your Multiple

At $10M-$15M, if you are selling capacity (hours) rather than capability (outcomes), Private Equity buyers view you as a “body shop.” The valuation multiple for a generalist Workday partner in this revenue band is typically 6x-7x EBITDA. Buyers know that without specialized IP or deep vertical expertise, your revenue is constantly at risk from lower-cost competitors or Workday’s own direct services arm.

To break through this ceiling, you must pivot from “doing Workday” to “solving specific business problems with Workday.” This means moving beyond HCM into high-value niches like Workday Financial Management (FINS), Adaptive Planning, or the newly emerging Workday Agent ecosystem. Partners who specialize here command bill rates 30-40% higher and trade at significantly higher multiples.

The climb from $10M to $50M requires a fundamental identity shift. You stop being a 'Workday shop' and start being a specialized consulting firm that happens to use Workday. If you don't make that shift, you will grind your margins to dust.

The $25M Valley of Death: Margins vs. Scale

Getting from $12M to $25M is the most dangerous phase of the journey. This is “Adolescence,” where you are too big to be small, but too small to be big. You need professional management—a VP of Sales, a CFO, Practice Leads for FINS and Planning—but these hires add $1.5M+ to your OPEX before they generate a single dollar of ROI.

We call this the “Valley of Death” because it’s where EBITDA margins historically dip. A firm that ran at 25% margin at $10M often drops to 12-15% at $20M as they invest in infrastructure. The goal is to survive this dip and emerge at $30M with a scalable engine.

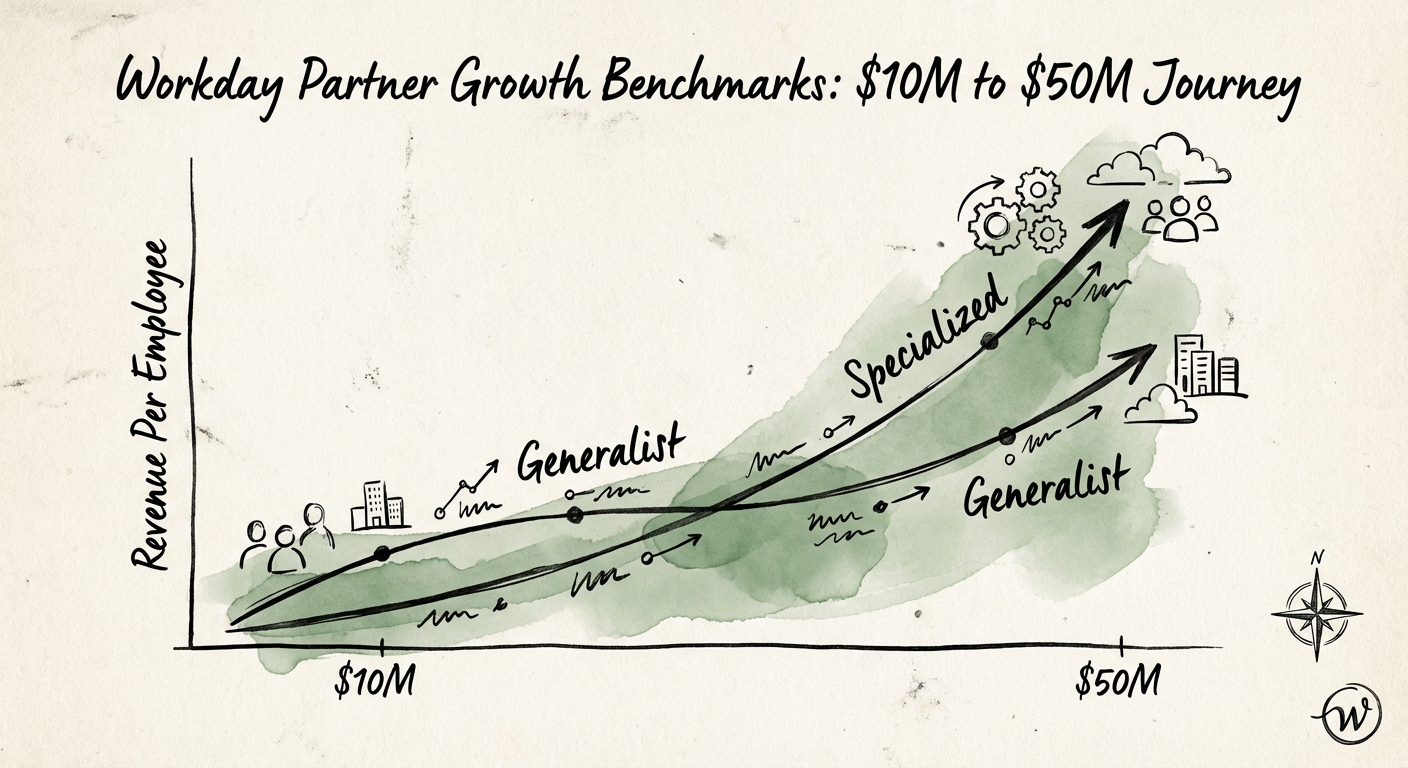

The Metric That Matters: Revenue Per Employee (RPE)

At this stage, your most critical efficiency metric is Revenue Per Billable Employee. In the “Generalist Trap,” this metric hovers around $175,000. To scale profitably to $50M, you must target $225,000+.

How do you hit $225k? You cannot do it with time-and-materials implementations alone. You need:

- Managed Services (AMS): Transitioning project customers into multi-year AMS contracts. Best-in-class partners have 40-50% of revenue in recurring AMS.

- Accelerator IP: Pre-built configurations for specific verticals (e.g., Healthcare, Higher Ed) that reduce delivery hours while maintaining fixed-fee pricing.

- Nearshore Leverage: Balancing your expensive onsite architects with high-quality nearshore delivery centers to blend down the cost of delivery while maintaining rate integrity.

The $50M Exit: The “Platform” Premium

When a Workday partner breaches $40M-$50M in revenue with 20%+ EBITDA margins ($8M-$10M EBITDA), the buyer universe changes dramatically. You are no longer a “bolt-on” acquisition; you are a “Platform Asset.”

PE firms pay a premium for Platforms because they can use you to acquire smaller $5M-$10M shops. The valuation multiple expands from the 6x-7x range to 12x-14x EBITDA. This is the “Arbitrage Opportunity”—buying smaller firms at 6x and instantly re-valuing their EBITDA at your 12x multiple.

The 2026 Differentiator: AI & Co-Sell

To command this premium in 2026, you must demonstrate alignment with Workday’s strategic roadmap. This means:

- Agentic AI: Having a dedicated practice for Workday AI and “Illuminate” capabilities.

- Co-Sell Maturity: 90% of top partners now use data-driven co-sell platforms (like Crossbeam) to map accounts with Workday Sales reps. If you are still relying on “coffee and donuts” relationships with AEs, you will lose to data-driven partners.

The journey to $50M is not just about selling more; it’s about architecting a firm that is built to be bought. It requires disciplined specialization, disciplined unit economics, and the courage to invest in overhead before the revenue arrives.