The practical answer

- Short answer

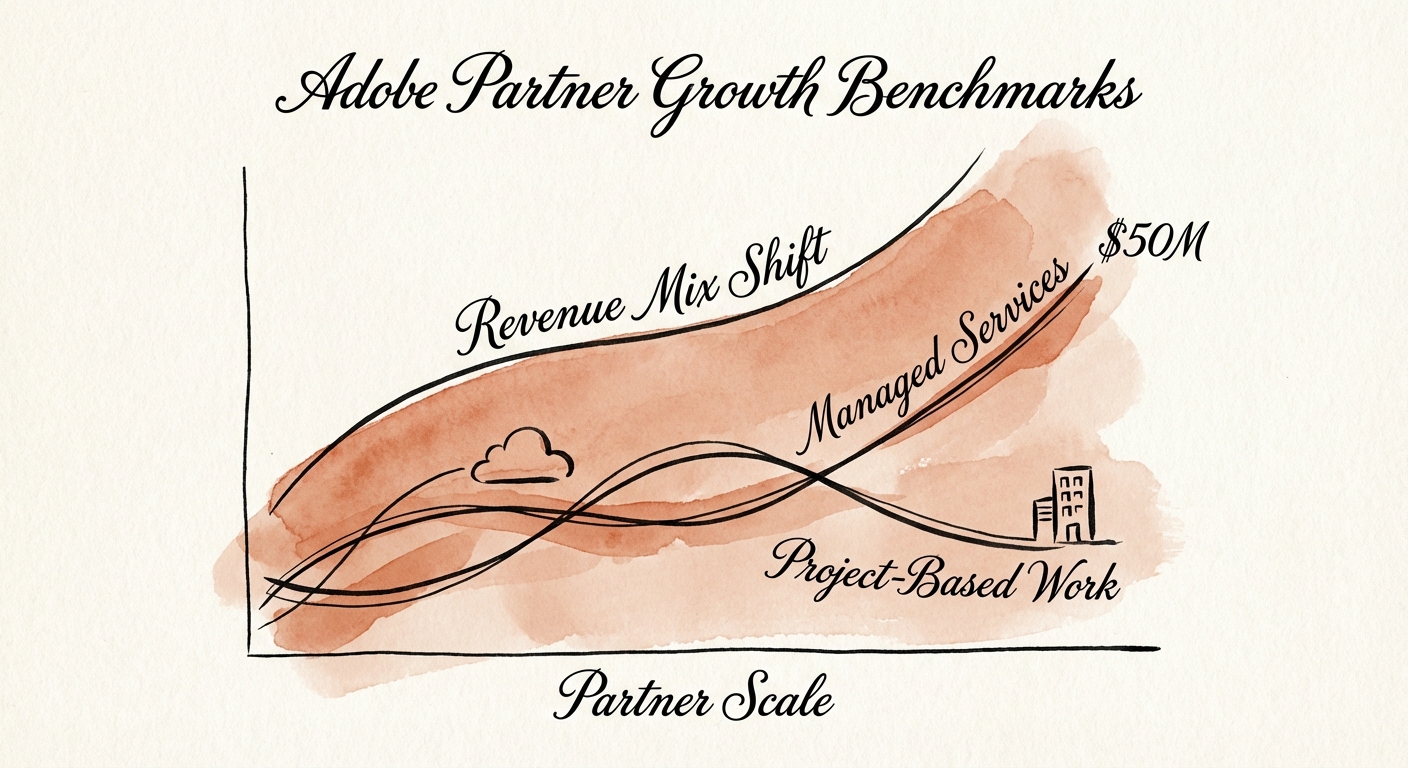

- Why Adobe Experience Cloud partners stall at $10M and how to scale to $50M. Valuation multiples, utilization benchmarks, and the shift to managed services.

- Best fit

- Industry: Professional Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 40% Target percentage of recurring revenue (AMS/IP) needed to secure a premium valuation multiple (10x+ EBITDA) in the Adobe ecosystem.

The $10M Ceiling: The Generalist Trap vs. Specialized Scale

In the Adobe partner ecosystem, $10M in revenue is the most dangerous number. It is the point where founder-led sales fail, where "full-service" value propositions lose their potency, and where the valuation gap begins to widen dramatically. Below $10M, an Adobe partner can survive as a generalist shop—implementing Adobe Commerce (Magento) one month and Adobe Experience Manager (AEM) the next, often relying on the founder's personal network for deal flow.

However, to break through the $10M ceiling and reach Gold or Platinum status, specialization is no longer optional; it is the primary driver of enterprise value. Private equity data from 2024-2025 indicates that Adobe partners with deep, verified Specializations (specifically in high-growth areas like Real-Time CDP and Content Supply Chain) command valuations up to 14x EBITDA, while generalist "body shops" struggle to exit at 6x.

The barrier is often operational. Generalist firms typically run at 65-70% utilization because they cannot efficiently deploy resources across disparate Adobe clouds (Creative, Document, Experience). Specialized firms, by contrast, can maintain 75%+ utilization by focusing on repeatable implementation methodologies (IP) within a single solution area. If you are stuck at Silver status, you are likely trading at a discount because you lack the "Deal Registration" leverage and co-sell motion that comes with Gold-tier specialization.

The partners trading at 14x EBITDA aren't just implementing software; they are selling business outcomes. They have shifted from 'billable hours' to 'strategic outcomes' wrapped in proprietary IP.

The $25M-$50M Valley of Death: Project Volatility vs. AMS Stability

Once an Adobe partner clears the $10M hurdle, the next plateau occurs between $25M and $50M. This is the "Valley of Death" where project-based revenue volatility kills EBITDA margins. At this stage, the sheer size of enterprise implementations—often spanning 12-18 months—creates a "lumpy" revenue recognition curve that terrifies potential acquirers.

To navigate this, the most successful partners aggressively pivot toward Application Management Services (AMS) and proprietary IP. The benchmark for a premium exit is now 40% recurring revenue. This does not mean simply reselling licenses (which adds revenue but little enterprise value); it means wrapping high-margin advisory and optimization services around the core Adobe stack.

For example, instead of just implementing Marketo Engage, top-tier partners sell "Marketing Operations as a Service," embedding themselves into the client's QBR process. This shifts the revenue quality from "one-off project" to "strategic retainer," stabilizing cash flow and increasing the multiple PE firms are willing to pay. If your firm is 80% project revenue at $25M, you are not building a business; you are building a series of deadlines.

The Valuation Delta: Why Digital Transformation Commands a Premium

Not all Adobe revenue is created equal. In the current M&A climate, there is a massive bifurcation in valuations between "Implementation Vendors" and "Digital Transformation Consultancies." Vendors are viewed as commodity labor—replaceable and low-margin. Consultancies are viewed as strategic assets.

The market is currently paying a premium for partners who can execute on the Adobe Experience Platform (AEP) and GenAI narratives. Partners who position themselves as "Content Supply Chain" experts—linking Adobe Creative Cloud workflows with AEM and Workfront—are seeing intense interest because they solve a C-Suite efficiency problem, not just a CTO technical problem.

Conversely, partners focused solely on legacy Adobe Commerce (Magento) maintenance or basic AEM Sites implementation are seeing multiple compression. To maximize your exit readiness, you must audit your revenue mix. Are you maintaining legacy systems, or are you enabling the next generation of customer experiences? The difference is often double the exit multiple.