The practical answer

- Short answer

- The Adobe Partner ecosystem is bifurcating. Why 'Content Supply Chain' specialists command 12x EBITDA multiples while generalist AEM shops stall at 6x. A 2026 exit roadmap.

- Best fit

- Industry: Professional Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 10.2% Adobe's projected FY2026 ARR growth target, setting the baseline for partner growth expectations.

The Great Bifurcation: Agency vs. Deep Tech

For the last decade, the Adobe partner ecosystem was forgiving. If you could implement Adobe Experience Manager (AEM) Sites and maybe do some light front-end development, you could build a $20M business with 20% EBITDA margins. That era ended in late 2024.

As we approach the March 1, 2026 unification of the Adobe Digital Experience Partner Program, the market has rigorously bifurcated. Private equity buyers and strategic acquirers (like Accenture Song, Deloitte Digital, and Publicis Sapient) no longer pay premiums for "capacity." They pay for specialization density.

Our data from Q4 2025 deal flow shows a stark valuation gap:

- Generalist Adobe Partners (5x-7x EBITDA): Firms that offer "full-service" creative and implementation but lack deep technical accreditation in emerging clouds. These firms are viewed as "agencies" with low recurring revenue and high project churn.

- Content Supply Chain Specialists (10x-14x EBITDA): Firms that have pivoted to "Edge Delivery Services," AEM Assets, and Adobe GenStudio. These partners aren't just building websites; they are automating the enterprise content factory. Buyers value this as "Industrialized IP," not just billable hours.

The "Paper Tiger" Trap

Many founders try to bridge this gap by rapidly acquiring certifications before a sale. This is the "Paper Tiger" trap. In 2025, due diligence teams began auditing certification utilization. If you have 50 AEM Architects but they are only utilized on 30% of your projects, your "Specialization" badge is discounted as marketing fluff. Real value lies in the application of that expertise to complex, multi-solution architectures (e.g., integrating Workfront + AEM Assets + Creative Cloud).

The days of trading on 'capacity' are over. In 2026, buyers don't buy headcount; they buy the ability to orchestrate the Content Supply Chain. If you aren't integrating Firefly and Edge Delivery Services, you're just another agency fighting for scraps.

The New Valuation Driver: 'Content Supply Chain'

The single biggest driver of valuation premiums in 2026 is the Content Supply Chain (CSC). Traditional AEM implementations are becoming commoditized. The "Blue Ocean" for exit value is the integration of generative AI (Firefly) into enterprise workflows.

Buyers are specifically hunting for partners who have moved beyond "Lift and Shift" migrations and are deploying:

- Edge Delivery Services: Moving customers to document-based authoring (the "Franklin" project evolution) to drastically cut TCO. Partners mastering this are displacing legacy SIs.

- Adobe Journey Optimizer (AJO): Implementing real-time personalization at scale. This requires deep data engineering capabilities, pushing you out of the "marketing agency" bucket and into the "IT consultancy" valuation bucket.

- GenStudio Integrations: Connecting the creative process (Creative Cloud) with the delivery engine (Experience Cloud).

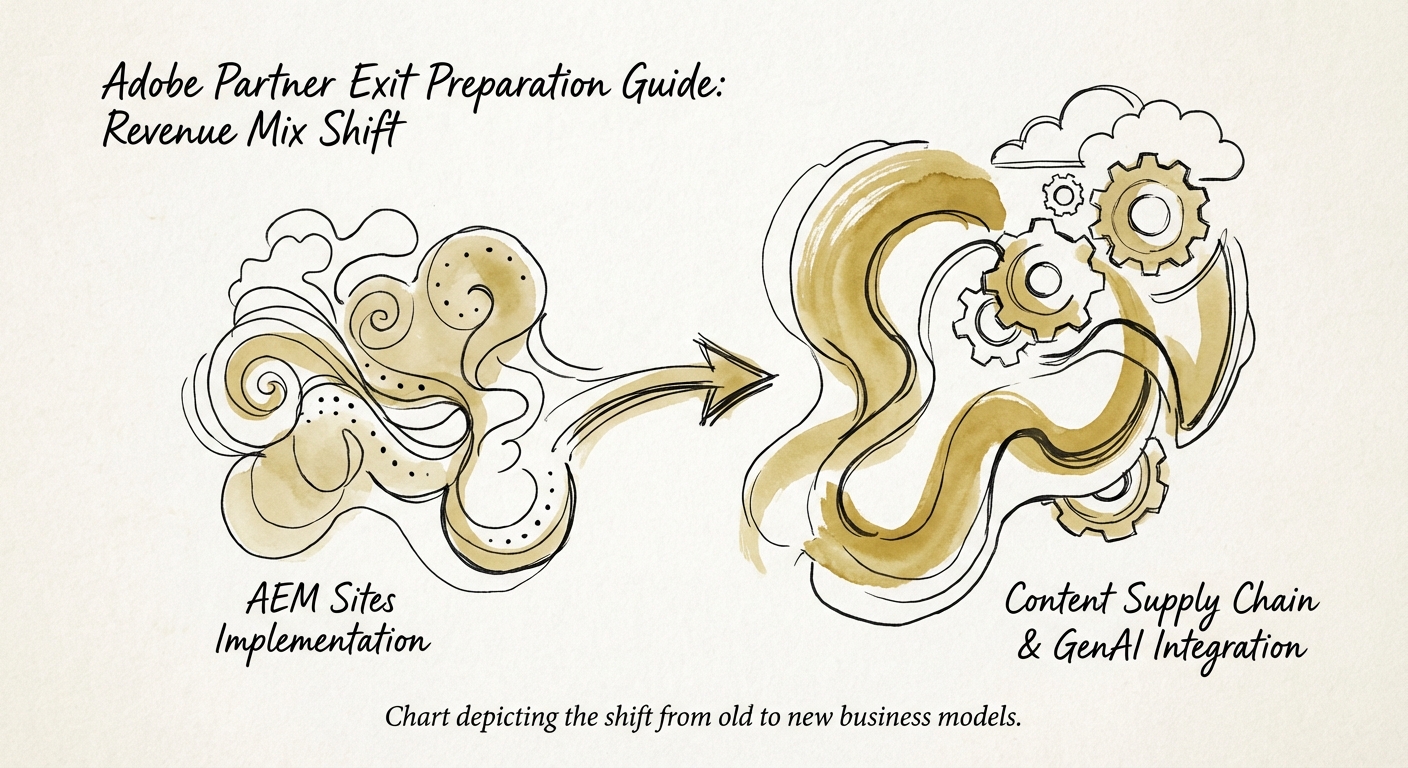

If your firm is still primarily selling "AEM Sites Upgrades," you are fighting a deflationary battle. To prepare for an exit, you must re-engineer your revenue mix. A target mix for a premium exit looks like: 40% Strategy/Architecture (high margin), 40% Implementation (CSC/AJO focus), and 20% Managed Services (Recurring).

The "Specialization" Cliff

Adobe's program requires partners to renew Specializations every two years with customer references. We see deals collapse when a partner loses a key Specialization (like Adobe Commerce or Marketo) during the Letter of Intent (LOI) phase. Actionable Advice: Ensure your Specialization renewal dates do not coincide with your projected transaction close date. A lapsed badge during diligence can trigger a 15% valuation re-trade.

Preparing for the 2026 Program Unification

On March 1, 2026, Adobe merges the Solution and Technology Partner programs. This is a critical inflection point for exit readiness. The new program emphasizes "Total Impact," rewarding partners not just for bookings, but for adoption and integration.

For founders, this means your exit narrative must shift from "We sell licenses" to "We drive consumption." Here is your 3-step exit prep checklist:

- 1. Audit Your "Active" Certifications: Do not just count heads. Map your "Certified Master" and "Certified Expert" staff to your top 10 revenue-generating accounts. If there is a mismatch, fix it. Buyers pay for proven capacity, not theoretical capacity.

- 2. Productize Your "Glue" Code: If you have custom connectors between AEM and common enterprise platforms (Salesforce, SAP, ServiceNow), package them. Even if they aren't full SaaS products, documenting them as "proprietary accelerators" moves you up the IP value chain.

- 3. Diversify Beyond AEM Sites: AEM Sites is the anchor, but it's no longer the growth engine. To hit the 12x multiple, you need to show traction in Adobe Real-Time CDP or Customer Journey Analytics. This proves you own the "Office of the CDO" (Chief Data Officer), not just the CMO.

The window to position yourself as a "Generative Experience Partner" is open now. By late 2026, the market will have chosen its winners. Don't be left holding a legacy "web development" bag when the market has moved to "autonomous content factories."