The practical answer

- Short answer

- Diagnostic for PE Operating Partners: Why Enterprise Oracle Fusion partners often trade at lower multiples than their Mid-Market counterparts due to revenue quality and margin erosion.

- Best fit

- Industry: Technology Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 10-12x EBITDA multiple for IP-led Mid-Market partners, compared to 6-8x for project-heavy Enterprise firms.

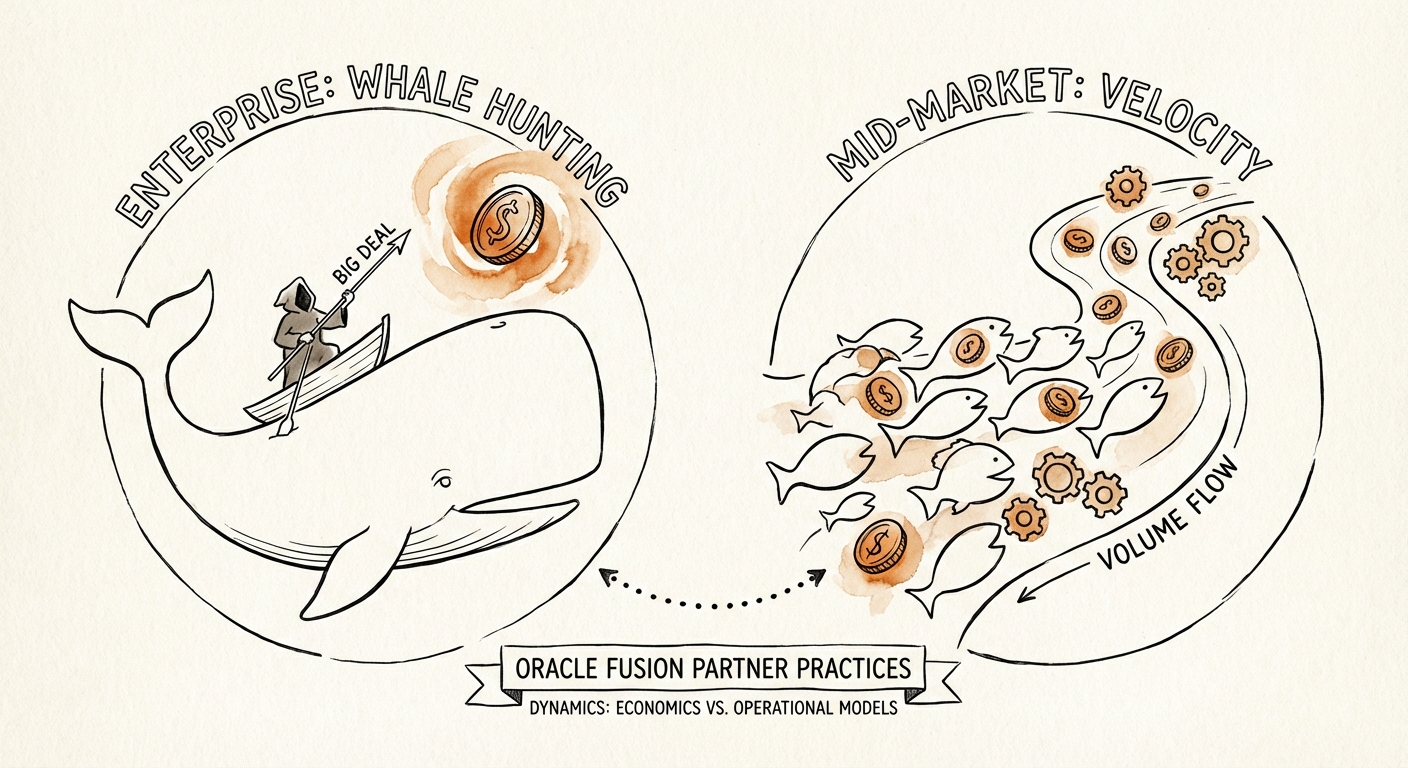

The "Whale Hunting" Trap: Revenue Vanity vs. Margin Reality

In the Oracle Fusion ecosystem, there is a pervasive myth that "Enterprise" logos equal higher enterprise value. For Private Equity Operating Partners, this is often the first red flag we see in a Quality of Earnings (QofE) report. You acquire a partner with $50M in revenue, boasting logos like GE, FedEx, or Pfizer, only to discover that the Quality of Revenue is high-risk.

The Enterprise Oracle Fusion market—spanning ERP, HCM, and SCM—has shifted drastically in 2025. While bill rates at the Enterprise level remain seductive ($225–$350/hr blended), the Cost of Revenue has exploded. Enterprise deals now demand massive pre-sales investment (often 6-9 months), risk-sharing "outcome-based" pricing models, and, most critically, a "subcontractor army" to fulfill the sheer volume of seats required. A firm might win a $5M implementation, but if 60% of the delivery is fulfilled by 1099s or low-margin staffing partners to meet the "bodies in seats" requirement, your Gross Margins plummet from a healthy 50% to a staffing-like 35%.

Contrast this with the Mid-Market (companies with $100M-$1B revenue). Here, the sales cycle is 90-120 days. The implementation scope is standardized—often using "accelerators" or pre-packaged IP rather than custom code. The result? A delivery model that scales without linear headcount growth. In our 2025 analysis of Oracle partner exits, Mid-Market focused firms with high IP adoption traded at 10x-12x EBITDA, while their "Whale Hunting" Enterprise counterparts struggled to clear 6x-8x. The market doesn't pay for revenue; it pays for reproducible margin.

The market doesn't pay for revenue complexity; it pays for margin reproducibility. A $20M Oracle partner with 60% recurring revenue is worth more than a $50M partner hunting whales.

The Managed Services Bridge: Where Valuation is Won or Lost

The single biggest valuation driver in 2026 is the Implementation-to-Managed-Services Attach Rate. In the Enterprise space, this is notoriously difficult. A Fortune 500 CIO typically unbundles services: they hire a Big 4 firm for strategy, a boutique for implementation, and push support to low-cost offshore providers or internal teams. The "attach rate" for high-margin Application Managed Services (AMS) in Enterprise deals hovers around 15-20%.

In the Mid-Market, the dynamics are inverted. The Mid-Market CIO is often resource-constrained and prefers a single accountable partner model. They don't want five vendors; they want one partner to implement Oracle Cloud HCM and run it for the next three years. Consequently, disciplined Mid-Market partners achieve AMS attach rates of 60-75%.

The Multiplier Effect of "Sticky" Revenue

This difference is mathematical, not just theoretical. Consider two firms with $20M revenue:

- Firm A (Enterprise Hunter): $18M Projects (one-off), $2M Recurring. Valuation: ~6x EBITDA.

- Firm B (Mid-Market Farmer): $10M Projects, $10M Recurring (AMS + IP). Valuation: ~10x EBITDA.

Firm B is worth nearly double Firm A, despite having the same top-line revenue. Why? Because Net Revenue Retention (NRR) in Firm B is likely 110%+, while Firm A starts every year at zero. For PE sponsors, the strategic pivot must be to force the "Enterprise" partner to adopt "Mid-Market" discipline: standardized offerings, mandatory AMS bundles, and IP-led delivery.

Operational Diagnostic: Are You a Consultancy or a Staffing Firm?

To determine if your portfolio company is ready for a premium exit, you must audit their operational DNA. Many "Oracle Platinum Partners" are effectively high-end staffing agencies masking as consultancies. Here is the diagnostic framework we use:

1. The Subcontractor Ratio

Check the W2 vs. 1099 ratio on billable delivery. If >20% of revenue is delivered by contractors, you have a Gross Margin leak. Enterprise projects often force this ratio up to 40% during "surge" phases. A premium valuation requires a W2-led delivery model where IP creates the leverage, not bodies.

2. The "Custom Code" Trap

Audit the last 10 SOWs. Are they 100% T&M (Time & Materials) with undefined scope? That’s not a business; that’s a rental service. Premium partners sell Fixed Scope / Fixed Price outcomes based on proprietary accelerators. If your firm is rewriting the same integrations for every client, you have zero IP leverage.

3. The Utilization Lie

Enterprise shops often boast 85% utilization, but this is a vanity metric if the Revenue Per Employee is flat. High utilization on low-rate projects is just "busy work." We look for Effective Bill Rate (EBR) realization. If your standard rate is $250 but your EBR (after discounts and non-billable travel) is $160, you are bleeding value.

The Fix: Shift the GTM motion. Stop chasing low-margin Enterprise RFPs where you are a comparison vendor for Deloitte. Pivot to the upper Mid-Market ($250M-$2B revenue clients) where you can dictate the methodology, bundle the AMS, and command a "Specialist Premium" rather than a "Generalist Discount."