The practical answer

- Short answer

- Azure grew ~33% last year. If your Microsoft practice grew 20%, you lost share. Growth, margin, and valuation benchmarks for partners at $5M, $15M, and $50M.

- Best fit

- Industry: Technology Services. Function: Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- $8.45 The amount of service revenue top partners generate for every $1 of Microsoft license revenue.

You can grow 20% and still be losing

Here is a sentence that ends a lot of comfortable board meetings: in the Microsoft ecosystem, the platform's growth rate is your hurdle rate. Azure ran at roughly 33% year-over-year heading into 2026 (Microsoft FY25 Q2). That is not a stretch goal. That is the current carrying you. If your practice grew 20% last year, you didn't have an off year — you quietly handed share back to the platform you sit on top of.

For most of the last decade, that math was hidden. Cloud adoption was a tide, and you could be a competent generalist — resell some CSP licenses, run a few lift-and-shift migrations, attach a managed-services contract — and post 25% growth almost by accident. Late-2025 partner data closed that loophole (CRN). The ecosystem split into two populations that no longer look like the same business.

On one side: the CSP-resell generalist. Margin built on license rebates and basic IaaS migration, gross margins compressing toward the mid-30s as everyone races the same hourly rate to the floor. On the other: the partner who pulls more than a quarter of revenue from Data and AI work — Fabric builds, Azure OpenAI deployments, Copilot rollouts — and is growing around 46% (IDC). Same logo on the badge. Completely different company.

The reason this matters past pride: the generalist version hits a ceiling, and it's a specific one. Founder-led sales runs out of personal bandwidth, and CSP resell — often under 15% gross margin — simply cannot pay for the senior solution architects you'd need to climb past it. The wall isn't a market problem. It's the unit economics of the revenue you chose.

In the Microsoft ecosystem, the platform's growth rate is your hurdle rate. Azure ran ~33% last year. Grow 20% and you didn't have a good year — you quietly ceded share to the platform you're built on.

Find your stall point on this map

Microsoft partners break at predictable revenue lines, and they break for structural reasons, not effort reasons. Read these as three different companies, because to an acquirer that's exactly what they are.

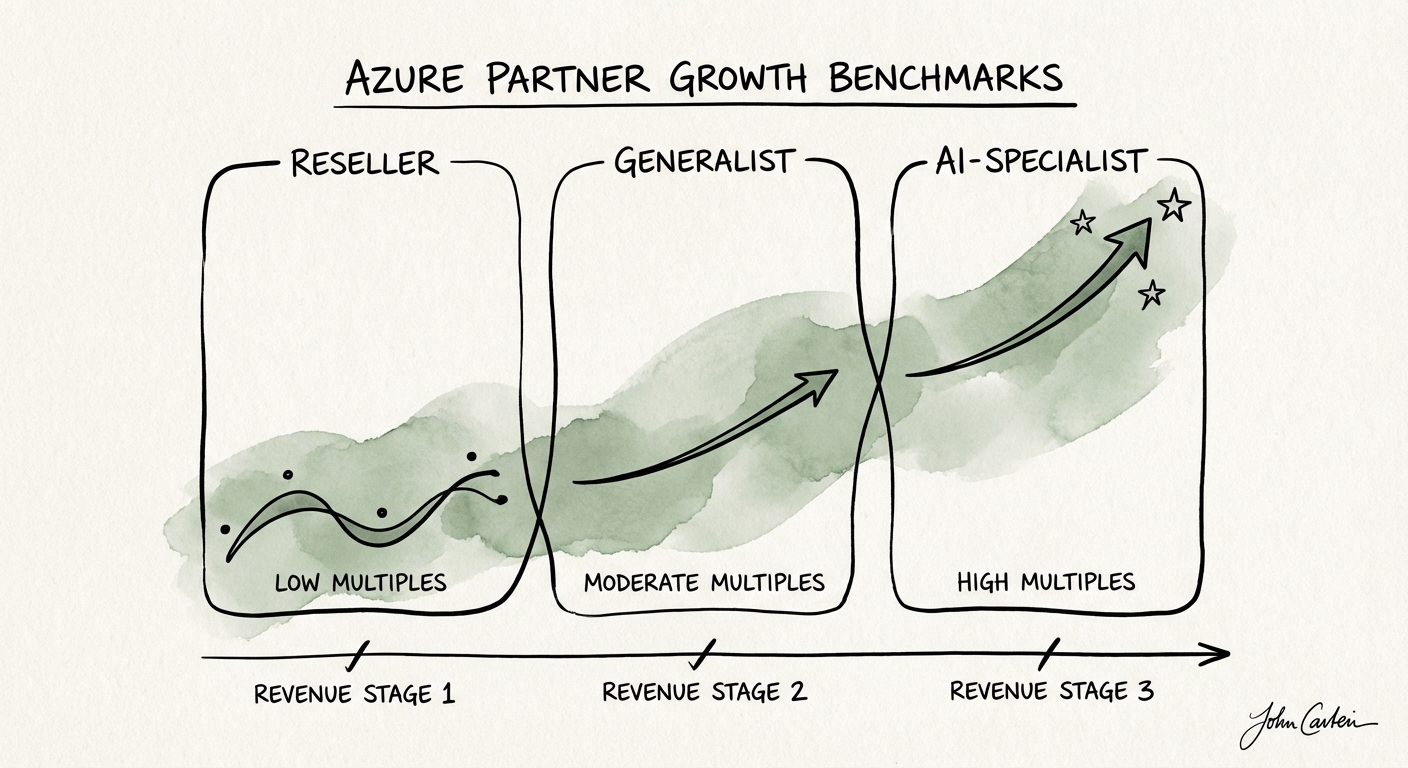

Under $5M — the rebate-chaser

Tell: your "services" line is really drag-along from licensing deals, and your quarter lives or dies on whether the local Microsoft field seller throws you a renewal. Blended gross margin sits under 25%. You will hear the phrase "value-added," but a buyer sees a pass-through entity — revenue that flows through you, not from you. That's why this profile clears roughly 4x to 6x EBITDA. You're priced as a license conduit because that's what the P&L shows.

$5M to $15M — the lift-and-shift plateau

You've built a real delivery bench, but it's pinned to low-value IaaS migration work. The trap shows up in one number: your bill rates ($175–$200/hr on infra) can't fund the $200K+ salaries that senior Azure architects now command, so you can't hire your way out of the commodity tier. You carry a Solutions Partner designation — and so does most of your competitive set, which means it sorts you into a pool rather than out of one. Gross margin lands in the 35–40% band; multiples in the 6x to 8x range. The polite name for the problem is "scaling pains." The accurate name is delivery debt: you trade hours for dollars and build no intellectual property a buyer can underwrite.

$15M to $50M — the Data and AI breakout

This is the company on the other side of the wall, and the tell is a ratio. Top service-led partners generate about $8.45 in services for every $1 of Microsoft license revenue (IDC) — versus the $3–$4 a generalist squeezes out. They lead conversations with Microsoft Fabric and Azure OpenAI, not VM counts. Gross margin runs 45–55%, and multiples step up to roughly 10x–14x EBITDA. The constraint here flips entirely: it's no longer demand or pricing, it's whether you can hire people who are genuinely fluent in Dataverse, the Fabric stack, and production-grade Python. Talent is the only thing throttling the growth.

Notice what changes across the three stages. It isn't how hard the team works — it's whether the revenue is reusable. Every dollar of IP-attached work compounds; every dollar of staff-aug evaporates the moment the engagement ends.

What to do before you go to market

If exit is on the 24-month horizon, understand how the buyer reads you. Private-equity teams have learned to discount CSP revenue on sight — they treat it as low-quality, low-retention, and structurally unprofitable, and they treat undifferentiated "infrastructure support" as a margin sinkhole. The number that earns a double-digit multiple isn't ACR. ACR (Azure Consumed Revenue) is Microsoft's scoreboard for how much cloud you drive into their P&L — it is not the same as profitable, defensible revenue in yours. Stop reporting it as if it were your win. Report IP-attached services revenue instead.

One useful reframe: in this ecosystem, the bar isn't the old Rule of 40. Call it the Rule of 46 — the growth rate the AI-and-Data cohort is actually posting (IDC). It's not a buzzword tax. AI engagements run shorter and at higher margin (often 60%+), and they pull in long-tail Azure consumption that anchors the customer for years after the project closes. That combination — high margin now, sticky compute later — is exactly the cash-flow shape a buyer pays up for.

Three moves a Microsoft-partner CEO can start this quarter:

- Run gross margin by service line, not blended. The blended number hides the disease. If your "Managed Services" line is sitting near 30%, it isn't managed services — it's staff augmentation wearing a recurring-revenue costume. Real managed services clear 50%+. You can't fix a margin you've averaged away.

- Chase a Specialization, not just the designation. The Solutions Partner badge sorts you into the crowd; an advanced Specialization (AI and Machine Learning on Azure, for instance) sorts you out of it. That's increasingly the filter a buyer's diligence team applies before they take the first call.

- Transact in the Azure Marketplace. Partners who sell through the Marketplace pull meaningfully more enterprise leads, and a Marketplace presence plugs you into committed-spend budgets that procurement has already cleared. If you're not transacting there, you're invisible to the exact enterprise buyers you most want.

The arc across every stage is the same: you cannot resell your way to a $50M exit. You engineer your way there — by trading conduit revenue for revenue you own.