The 3-Year "Quick Flip" is Dead. Welcome to the 6-Year Grind.

For two decades, the private equity playbook was predictable: Buy at 10x, apply leverage, cut costs, and sell at 12x within 40 months. That era is over. The financial engineering levers that drove IRR for the last cycle—cheap debt and automatic multiple expansion—are broken.

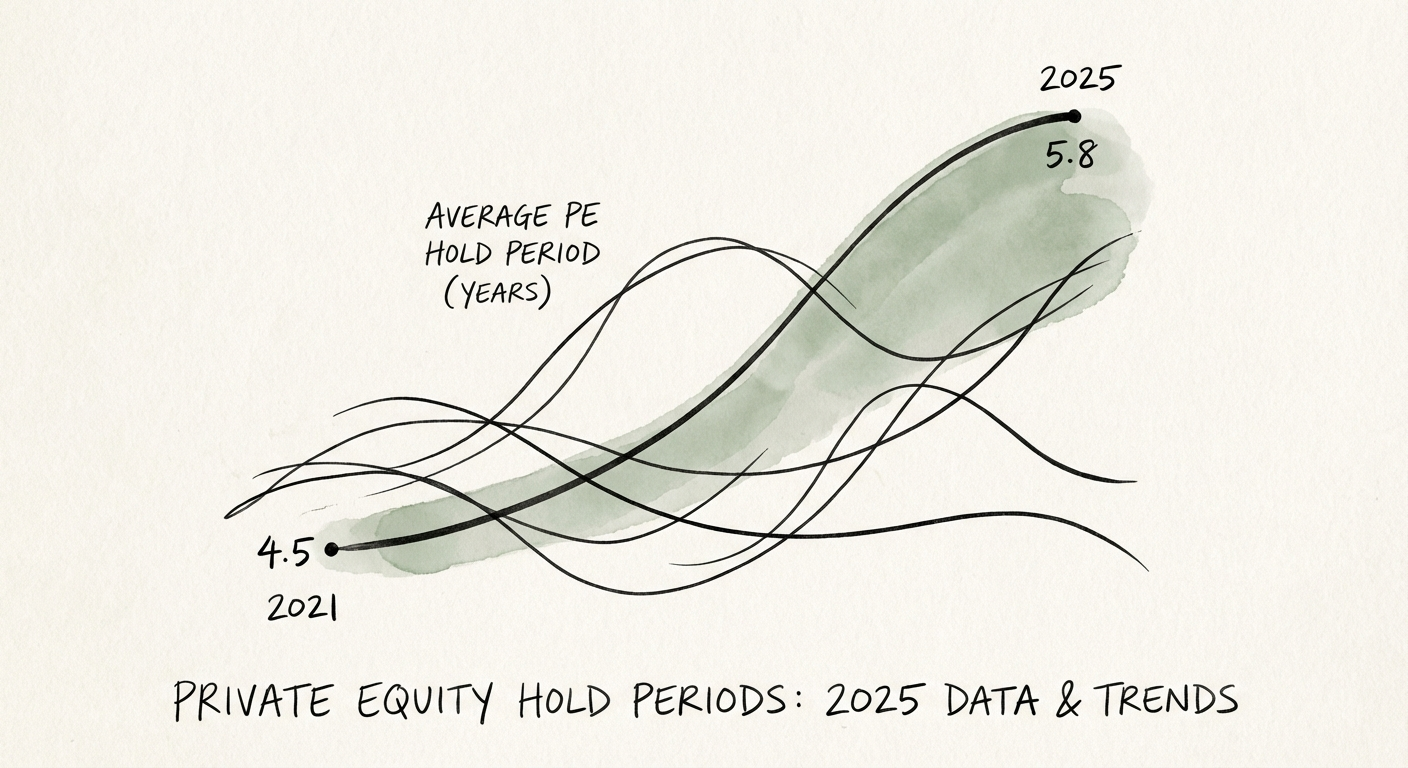

We are now operating in an environment of extended detention. According to 2025 data from PitchBook and S&P Global, the median holding period for US private equity buyouts has settled at 5.8 years, down slightly from the paralysis peak of 7.1 years in 2023, but still historically elevated. More concerning for Operating Partners is the "inventory age": the median age of current portfolio companies sits at 3.4 years, the highest in over a decade.

For PE Operating Partners, this shifts the mandate entirely. You aren't sprinting; you're running a middle-distance race with a sprinting pace. The "time value of money" clock is ticking louder than ever. When you hold an asset for six years instead of four, the IRR drag is massive unless you generate significant organic EBITDA growth. The 2x MOIC (Multiple on Invested Capital) that looked easy in 2021 now requires deep operational engineering to achieve.

The "Inventory" Problem

While exit activity is thawing in 2025, the backlog is immense. PitchBook reports over 11,000 PE-backed companies are currently in U.S. portfolios—inventory that must move. This congestion creates a buyer's market for add-ons but a seller's purgatory for platforms that aren't "Rule of 40" perfect. If your portfolio company has messy financials, undocumented technical debt, or flatlining retention, you aren't exiting in 2025. You are holding the bag until 2026 or 2027.

Industry Benchmarks: Where the Logjam is Worst

The "average" hold period hides significant variance across sectors. The dynamics in Healthcare differ wildly from Enterprise Software.

1. Healthcare: The Long-Haul Platform Build (6.5+ Years)

Healthcare Services (Dental, Vision, Outpatient) are seeing some of the longest hold periods. Why? The "Buy-and-Build" strategy takes time. Integrating 50 dental practices into a coherent platform with shared back-office operations is not a 3-year job. With $115 billion invested in healthcare in 2024, firms are doubling down on consolidation. They are holding assets longer to prove that the "platform" is real and not just a loose collection of clinics.

2. Enterprise Software: The Bifurcated Exit (4.5 vs. 7 Years)

Software is a tale of two cities. High-quality SaaS assets (Rule of 40, "mission critical", <100% NRR) are clearing the market quickly—often in under 5 years—as strategic buyers return. However, "B-Player" software firms—those with high churn or crippling technical debt—are stuck. Operating Partners are forced to hold these assets for 6-7 years to fix the underlying unit economics before a sale is viable.

3. The Rise of Continuation Funds: The "Fake" Exit

A critical trend distorting the data is the explosion of Continuation Vehicles (CVs). Industry estimates suggest CVs will account for 20% of all exits in 2025, with transaction volumes approaching $100 billion. Technically, this counts as an "exit" for the old fund, but for the Operating Partner, the job continues. You are essentially re-underwriting the asset for another 3-5 years. This isn't a liquidation; it's a refinancing of the timeline.

| Metric | 2021 (Peak Frenzy) | 2023 (Peak Paralysis) | 2025 (Current Reality) |

|---|---|---|---|

| Median Hold Period | 4.5 Years | 7.1 Years | 5.8 Years |

| Primary Exit Channel | Sponsor-to-Sponsor | None (Held) | Strategic / Continuation Fund |

| Cost of Debt | 4-5% | 10-12% | 8-9% |

The 2025 Operator's Playbook: What to Do With the Extra 2 Years

If you are holding an asset for 6 years, you cannot rely on market beta. You must generate alpha through operations. Here is the playbook for the "Extended Hold" scenario.

1. From Financial Engineering to EBITDA Engineering

In a 4-year hold, you can slash costs and exit. In a 6-year hold, you must build scalable infrastructure. You cannot cut your way to growth for six years. You need to fix the Revenue Architecture. This means moving from "Founder Heroics" sales to a systematic commercial engine. If your portfolio company still relies on the founder to close the biggest deals, you are not exit-ready.

2. Aggressive Add-on Integration

Use the extended timeline to buy smaller competitors at lower multiples (6-8x) to blend down your entry multiple. But buy with caution: 70% of integration synergies never materialize because of poor operational execution. Don't just stack financials; integrate the tech stacks and sales teams within 12 months, not 36.

3. The "Mid-Hold" Audit

If you are in Year 4 of a 6-year hold, treat today like Day 1. Conduct a full Operational Assessment. Is the management team that got you from $10M to $50M capable of getting you to $100M? Often, the answer is no. Replace the "Wartime" CFO with a "Scaling" CFO. Audit the code base for scalability. Use the extra time to pay down technical debt that would otherwise be a red flag in Diligence.

The Bottom Line: A 5.8-year hold period is a curse for the passive investor but a gift for the active operator. It provides the runway to fix fundamental flaws that a quick flip would have ignored. But you have to use the time, not just endure it.