The practical answer

- Short answer

- Why generalist Workday partners trade at 7x EBITDA while industry specialists command 14x. A 2026 valuation guide for PE Operating Partners.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Average EBITDA multiple for Workday Industry Specialists (Healthcare/Edu) in Q4 2025.

The Great Bifurcation: 7x vs. 14x

In 2023, having a "Workday" badge was enough to secure a 10x EBITDA multiple. The ecosystem was supply-constrained, and anyone with certified bodies could print money. That era is dead.

As we enter 2026, the Workday partner ecosystem has violently bifurcated. We are no longer seeing a bell curve of valuations; we are seeing a distinct split between Generalist Implementers and Vertical Specialists.

Our data from the last 12 months of deal flow shows a stark reality:

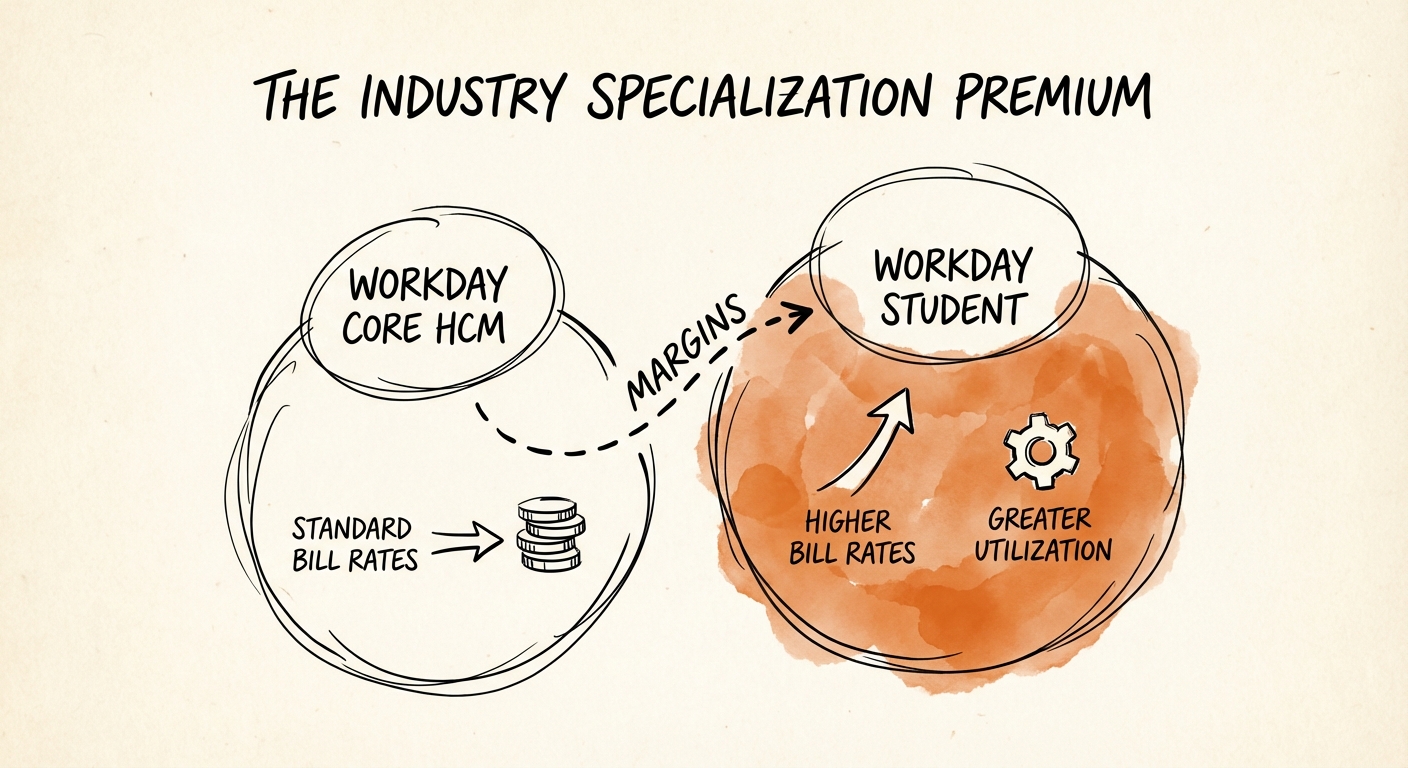

- Generalist Firms (HCM/Financials Core): Trading at 6x–8x EBITDA. These firms are increasingly viewed as "staff augmentation" businesses. They compete on rate cards ($195–$215/hr), suffer from high attrition, and have no defensive moat against the Global Systems Integrators (GSIs).

- Vertical Specialists (Higher Ed, Healthcare, Gov): Trading at 12x–14x EBITDA. These firms don't just implement software; they install business processes specific to an industry. They command bill rates of $285–$325/hr, utilize "Industry Accelerator" badges to get sole-source access from Workday sales reps, and maintain EBITDA margins north of 25%.

For a Private Equity sponsor, the message is clear: If your portfolio company is pitching "we do Workday," you are holding a depreciating asset. If they are pitching "we fix Student Information Systems for R1 Universities," you are holding a premium asset.

You can't be 'Premier' at everything. In 2026, if you don't own a vertical, you don't own a business—you own a staffing agency with a Workday badge.

The "Industry Accelerator" Moat

The driver of this premium isn't just margin profile—it's Cost of Customer Acquisition (CAC) and Pipeline Quality. Workday's 2025/2026 Go-to-Market strategy relies heavily on its "Industry Accelerators"—pre-packaged solutions for sectors like Healthcare, Higher Education, and Public Sector.

When a Workday Account Executive (AE) has a quota to retire in the Healthcare vertical, they do not bring in a generalist partner. They bring in the partner who understands supply chain compliance for hospitals or clinical labor management. Why? Because that partner increases the AE's probability of closing the software deal.

The Operational Delta

This preference creates a virtuous cycle for specialists that shows up in the Quality of Earnings (QofE):

- Sales Efficiency: Specialists often see CAC Payback periods under 8 months, compared to 14+ months for generalists who must hunt their own leads.

- Utilization Floors: Generalists suffer from "bench rot" between projects. Specialists in tight verticals (like Workday Student) often have backlogs of 6-9 months, keeping utilization consistently above 75%.

- Rate Card Elasticity: A generalist fighting for a Core HCM deployment is price-takers against Accenture and Deloitte. A specialist deploying Workday Adaptive Planning for a specific sub-vertical (e.g., Regional Banking) is a price-maker.

We recently advised on a buy-side diligence for a $40M Healthcare-focused Workday partner. Their EBITDA margin was 28%—nearly double the 16% average of the generalist peers we tracked in the same quarter. The difference wasn't overhead; it was the premium bill rates derived from specialization.

The 18-Month Pivot from Generalist to Specialist

If you are holding a generalist Workday asset, you cannot simply "market" your way to a higher multiple. You must engineer a pivot before you go to market.

We recommend a three-step "Vertical Injection" strategy for PE-backed partners:

- Pick One "Power" Vertical: Do not try to be everything. Look at your past 20 deployments. Where did you have the highest margins and the happiest customers? If it was mid-market manufacturing, double down. If it was non-profits, own it.

- Build IP, Don't Just Bill Hours: Develop proprietary configurations or "accelerators" for that vertical. A standard "Higher Ed Deployment Kit" that reduces implementation time by 20% is valuable IP. It converts one-time labor revenue into recurring maintenance streams.

- Re-Train the Channel: Your CEO needs to stop telling Workday AEs "we have capacity." They need to start saying "we close your Manufacturing deals." Map your sales team directly to Workday's vertical sales leadership.

The window to exit a generalist firm is closing. The "lift and shift" cloud migration wave is ending; the next wave is industry-specific optimization. Your exit multiple depends entirely on whether you are positioned as a commodity laborer or a strategic expert.