The practical answer

- Short answer

- Data & AI consultancies are bifurcating. Generalist Databricks partners trade at 8x EBITDA, while GenAI specialists command 14x. Here is the diagnostic.

- Best fit

- Industry: Data & AI Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for GenAI-specialized Databricks partners, compared to 8.8x for generalist IT consultancies.

The Great Bifurcation: 'Pipe Builders' vs. 'Model Makers'

For the last five years, the Databricks partner ecosystem was a reliable, if predictable, volume game. The playbook for Private Equity was simple: acquire a regional System Integrator (SI), stack certifications, push "Lakehouse" migrations, and exit at 8x-10x EBITDA. The value was in the plumbing—moving data from on-premise silos to the cloud.

That thesis is now dead. The acquisition of MosaicML by Databricks for $1.3 billion signaled a violent shift in the value chain. The market no longer pays a premium for moving data; it pays for reasoning with it. Consequently, we are seeing a valuation bifurcation in 2025/2026 that is catching generalist firms off guard.

The Valuation Gap

According to 2025 M&A data, generalist IT service firms are stabilizing at roughly 8.8x to 11.2x EBITDA. However, firms with verifiable "Data Intelligence" and GenAI capabilities—specifically those capable of fine-tuning LLMs and deploying agentic workflows on the Databricks Data Intelligence Platform—are commanding valuations upward of 14x EBITDA.

The driver is the Velocity Partner Program. Databricks has shifted incentives from commitments to consumption. In the AI era, consumption is king. A "lift and shift" migration creates a one-time spike in compute. An operationalized Large Language Model (LLM) or RAG (Retrieval-Augmented Generation) architecture creates a permanent, compounding consumption layer. Acquirers know this. They aren't buying service hours; they are buying the sticky, high-margin consumption revenue that GenAI workloads generate.

The market no longer pays a premium for moving data; it pays for reasoning with it. A firm that builds autonomous agents and custom LLMs is the target.

The Anatomy of a 14x Databricks Partner

What separates a firm trading at 14x from one stuck at 8x? It is not the number of "Elite" badges on the website. It is the composition of the revenue mix and the technical depth of the delivery team.

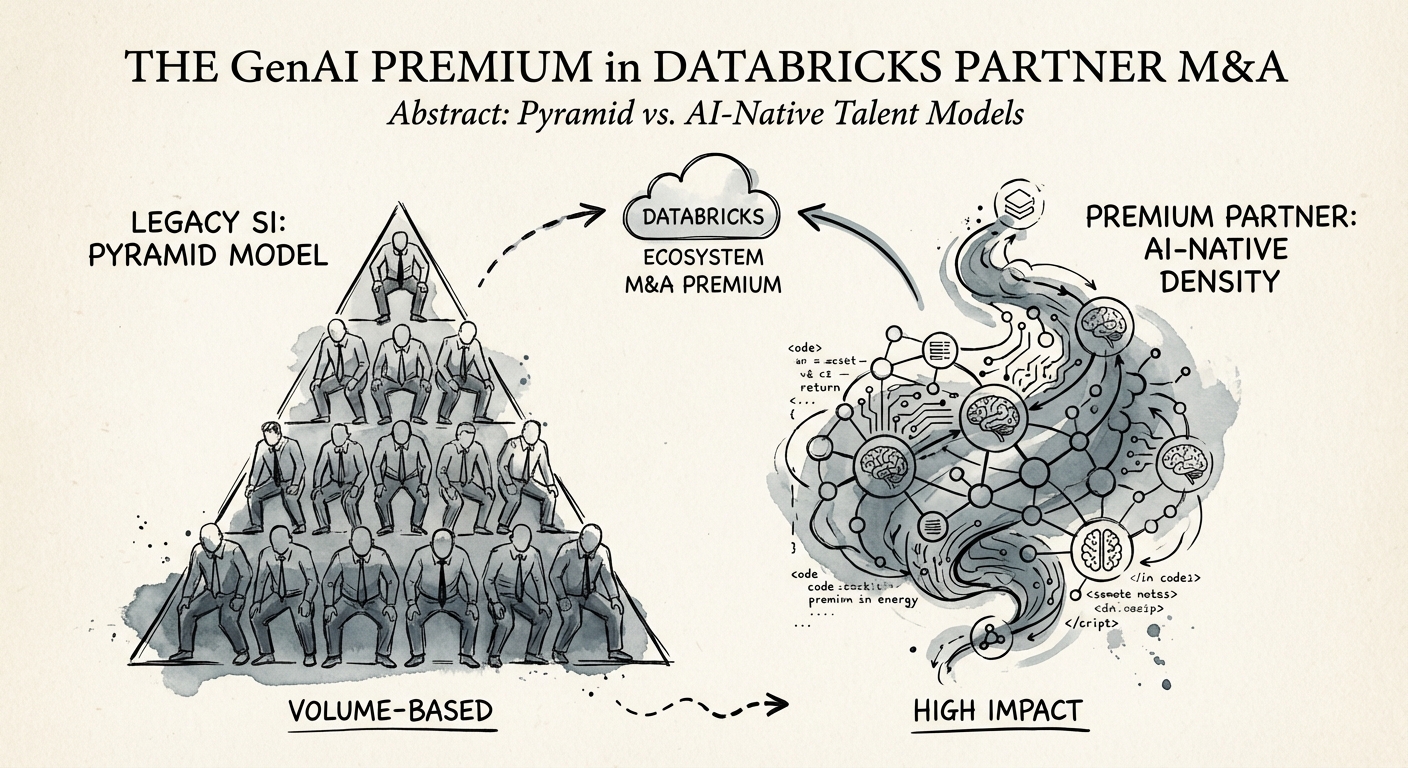

Generalist partners (8x) have a "Pyramid" talent model: a few architects atop a massive base of junior data engineers billing for ETL (Extract, Transform, Load) pipelines. Their revenue is 90% time-and-materials. They compete on rate cards.

Premium partners (14x) operate an "AI-Native" model:

- Talent Density: They employ Machine Learning Engineers (MLEs) capable of using MosaicML to fine-tune open-source models (like Llama 3 or DBRX) on proprietary client data. They don't just build pipelines; they build inference engines.

- Asset-Based Revenue: They deploy proprietary IP—such as "Agent Bricks" or industry-specific RAG accelerators—that reduce time-to-value. This shifts revenue from pure services to higher-margin "solution" licensing or managed services.

- Revenue Quality: Their engagements are tied to production AI, not just Proof of Concepts (PoCs). PoCs are easy to sell but hard to renew. Production AI drives the Databricks consumption meter, aligning the partner perfectly with the vendor's own growth goals (and thus, deal flow).

Warning for PE Sponsors: Do not conflate "Data Science" with "GenAI." A firm that builds propensity models in notebooks is legacy. A firm that builds autonomous agents and custom LLMs is the target. The former is a commodity; the latter is a scarcity.

The Strategic Pivot: Capturing the Premium Before the Window Closes

The window to arbitrage this GenAI premium is narrow, likely closing by late 2027 as GenAI skills commoditize. For PE-backed Databricks partners currently sitting in the "Generalist" bucket, the path to a 14x exit requires an immediate, aggressive pivot.

1. Stop Selling Migrations, Start Selling 'Intelligence'

Rebrand your practice. If your homepage says "Cloud Migration," you are negotiating against global GSIs who will crush you on price. Position around "Enterprise AI Adoption" or "Domain-Specific LLMs." The goal is to be the firm that unlocks the data, not just the one that stores it.

2. Audit Your Utilization and Burn

AI-native firms have different unit economics. They burn more cash on talent (MLEs cost 50% more than Data Engineers) but generate higher revenue per employee. If your Revenue Per Employee is below $200k, you are operating a body shop, not a premium consultancy. You must raise rates and move up-market to justify the talent required for GenAI work.

3. Align with the 'Velocity' Program

Databricks rewards partners who drive consumption. Audit your current client base: how many are actually consuming DBU (Databricks Units) at scale? If you have 50 clients but only 5 are significant consumers, your "customer base" valuation metric is a hallucination. Focus your Customer Success efforts on lighting up AI workloads that drive compute.

The "GenAI Premium" is real, but it is not automatic. It is reserved for partners who have fundamentally re-architected their business model to serve the AI era. If you are still selling Spark pipelines while the market is buying Agentic AI, you are leaving 6 turns of EBITDA on the table.