The practical answer

- Short answer

- Generalist IT shops trade at 8x EBITDA. Specialized SuccessFactors partners trade at 12x+. Here is the operational diagnostic to capture the specialist premium in 2026.

- Best fit

- Industry: Private Equity. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.0x Median EBITDA multiple for specialized IT Consulting in 2025, compared to 11.2x for generalist firms.

The Valuation Gap: Generalists vs. Sharpshooters

In the private equity theater, there is no such thing as a "standard" IT services multiple. There is the Generalist Discount, and there is the Specialist Premium. As of Q1 2026, the data is unforgiving: generalist software development shops are trading at a median of 11.2x EBITDA. Meanwhile, specialized IT consultancies—particularly those with deep moats in ecosystems like SAP—are commanding upwards of 13.0x EBITDA, with premium assets seeing turns as high as 15x.

For a firm with $5M in EBITDA, that "Specialist Premium" isn't a rounding error; it’s a $9M to $15M difference in enterprise value. Why the gap? Because PE buyers like yourself aren't buying headcount; you're buying defensibility.

Generalist firms are commoditized "body shops" fighting a race to the bottom on hourly rates against offshore giants. They are easy to enter, easy to leave, and terrifying to model in a downturn. Specialized SuccessFactors partners, conversely, own a problem that the Fortune 1000 cannot afford to ignore. With SAP's ECC support deadline looming and the massive migration to S/4HANA and cloud HR underway, demand isn't just stable—it's practically mandated by technical obsolescence.

The "Rule of X" in Services

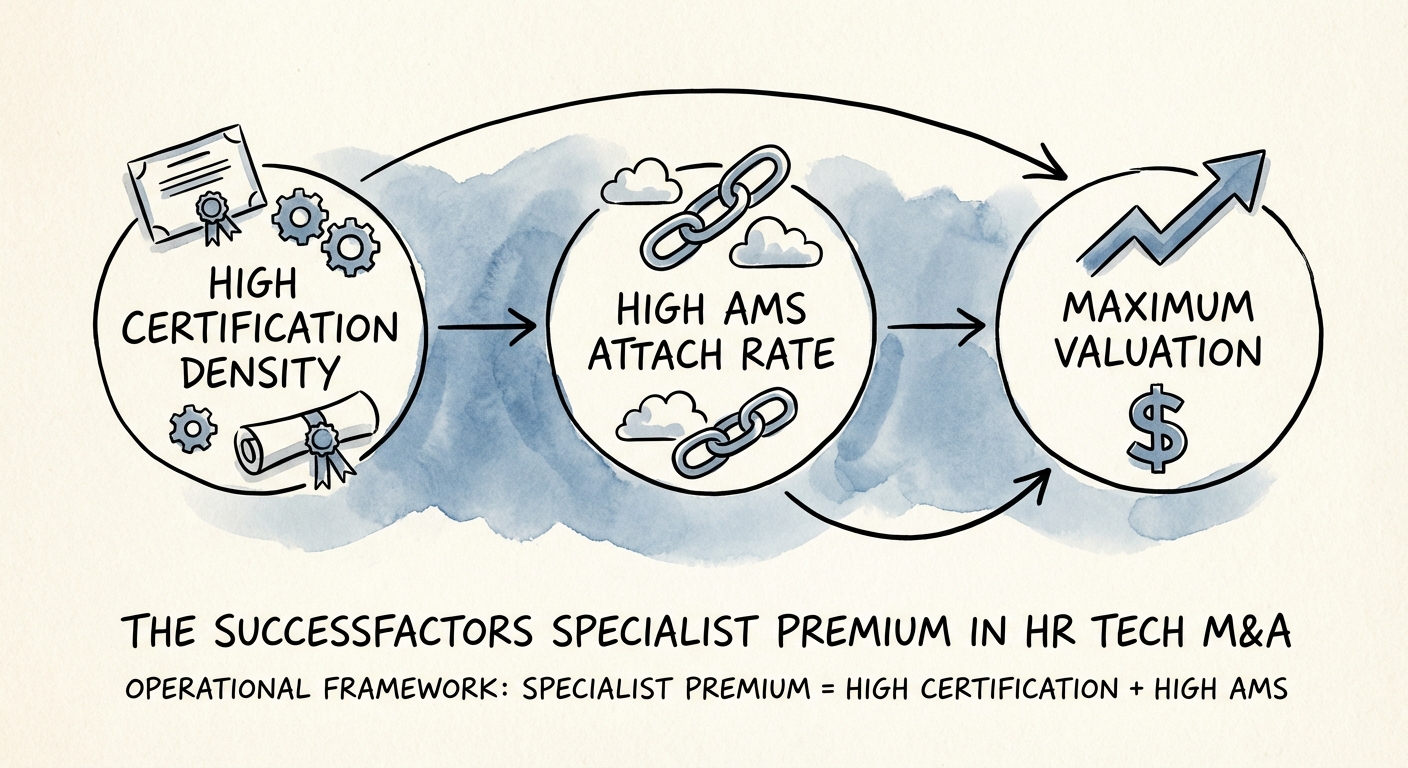

We are seeing term sheets shift from the "Rule of 40" (growth + margin) to what Bessemer and others call the "Rule of X," where the quality of revenue is weighted heavier than the quantity. In the SAP ecosystem, quality is defined by certification density and AMS (Application Management Services) attach rates. A firm with 30% growth but 0% recurring revenue is a project house. A firm with 15% growth but 40% locked-in AMS revenue is a platform.

Private equity buyers aren't buying your headcount; they are buying your defensibility. A $5M EBITDA generalist is a commodity. A $5M EBITDA specialist is a platform.

The SuccessFactors Moat: Why HR Tech is 'Sticky' EBITDA

Why SuccessFactors specifically? Why not general ERP implementation? Because HR data is the "third rail" of enterprise compliance. You can survive a weekend glitch in your procurement software; if payroll fails or compliance data leaks, the CEO gets fired. This creates an inherently stickier relationship than almost any other IT vertical.

But the real multiple driver in 2026 is the Cloud Migration Supercycle. Estimates suggest that less than 40% of SAP's install base has fully completed the migration to S/4HANA and cloud-native HXM (Human Experience Management). This isn't just an implementation queue; it's a decade-long backlog of guaranteed work.

However, the premium only accrues to firms that have moved beyond "staff aug." To capture the 13x multiple, your portfolio company must demonstrate:

- High Certification Density: We look for a ratio of 2.5+ certifications per consultant. If your team is just "familiar" with Employee Central but not certified, you are selling labor, not expertise.

- The AMS Attach Rate: Best-in-class firms attach an AMS contract to 70%+ of their implementation projects. This converts lumpy project revenue into a predictable recurring stream that buyers will capitalize like SaaS.

- IP vs. Hours: The highest valuations go to firms that have productized their service delivery—proprietary accelerators, pre-built integration connectors for payroll, or automated data migration tools.

Operationalizing the Premium: The 2026 Diagnostic

You have a portfolio company in the HR Tech space. How do you know if you're sitting on a 6x asset or a 12x asset? Run this diagnostic immediately.

1. The Revenue Mix Test

If >80% of revenue is "eat what you kill" project work, you are a 6x shop. You need to aggressively pivot to Managed Services. The goal is 30-40% Recurring Revenue by exit. This buffers the P&L against market volatility and allows aggressive leverage utilization by the buyer.

2. The Utilization vs. Rate Matrix

Generalists run high utilization (90%+) at low rates. Specialists run healthy utilization (75-80%) at premium rates. If your utilization is 95%, you aren't efficient; you're underpriced and burning out your assets (people). The target for a premium exit is a Gross Margin of 45-50% on services. Anything less implies you are competing on price, not value.

3. The 'Key Person Dependency' Risk

In niche firms, the biggest risk is the 'Rainmaker Founder' who holds all the client relationships. To get the 13x multiple, you must demonstrate Transferability. Show me a sales pipeline that is generated by a system, not the CEO's rolodex. Show me delivery SOPs (Standard Operating Procedures) that allow a mid-level consultant to deliver senior-level results.

The market is paying a premium for specialized systems. If you can prove your SuccessFactors practice is a machine, not a magic trick, you will command the multiple you deserve.