The practical answer

- Short answer

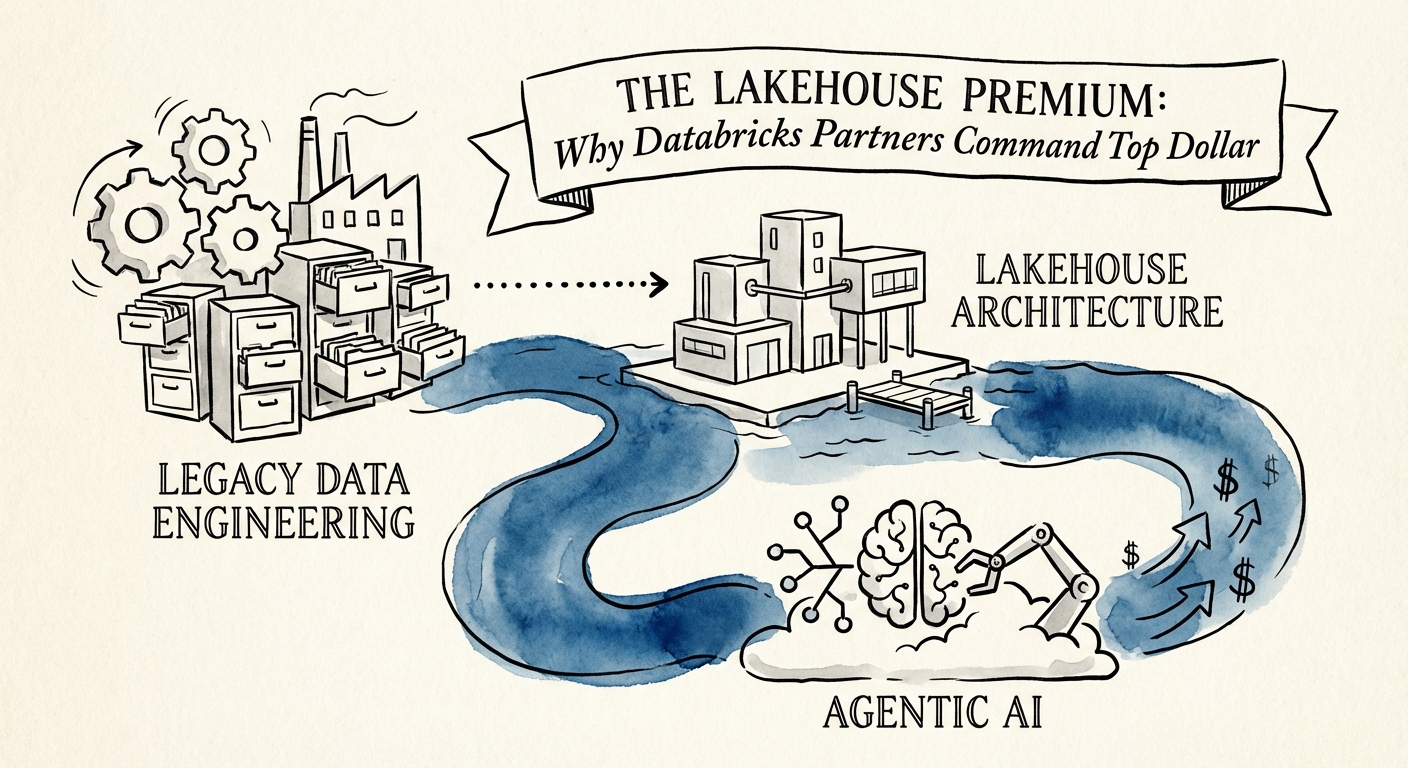

- Why specialized Databricks partners trade at 14.5x EBITDA while generalist cloud firms stall at 8x. A guide for PE sponsors and founders on the Lakehouse Premium.

- Best fit

- Industry: Data & AI. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 55% Databricks Year-Over-Year Revenue Growth (reaching $4.8B ARR in 2026).

The $134B Signal: Why the Market is Bifurcating

In December 2025, Databricks closed its Series L funding round at a $134 billion valuation, reporting $4.8 billion in ARR and a significant 55% year-over-year growth rate. For Private Equity sponsors and search funds, the headline number isn't the valuation—it's the 140% Net Dollar Retention (NDR). This metric confirms that once a customer adopts the Lakehouse architecture, they expand aggressively. This expansion doesn't happen via software alone; it requires a specialized service layer that generalist IT firms cannot provide.

We are witnessing a violent bifurcation in the IT services M&A market. On the left, we have generalist cloud migration shops—firms that "lift and shift" infrastructure to AWS or Azure. These firms are seeing multiples compress to 8x-10x EBITDA as infrastructure becomes commoditized. On the right, we have the "Lakehouse Specialists"—firms with deep expertise in Spark, Unity Catalog, and MosaicML. These assets are trading at a 14.5x EBITDA premium.

Why the gap? Because the "Lakehouse" isn't just a storage architecture; it is the operating system for Enterprise AI. While generalist partners are fighting over rate cards for low-margin infrastructure support, Databricks partners are building the data foundations required for Generative AI. This is not "body shop" revenue; it is strategic transformation revenue, and acquirers like Accenture and specialized PE platforms are paying a premium for it.

The Lakehouse isn't just a storage layer; it's the operating system for Enterprise AI. Partners who master Unity Catalog and MosaicML aren't just service providers—they are the architects of the next decade of corporate intelligence.

The "Agentic" Multiplier: Beyond BI to AI Agents

The primary driver of the Lakehouse Premium in 2026 is the shift from "Business Intelligence" (looking at the past) to "Agentic AI" (automating the future). Databricks' acquisition of MosaicML and the subsequent launch of "Agent Bricks" created a massive skills gap that the ecosystem is scrambling to fill.

Partners who have pivoted their delivery models to support Retrieval-Augmented Generation (RAG) and custom LLM fine-tuning are seeing significantly higher valuations than those stuck in traditional data engineering. Here is the valuation math of the pivot:

- Legacy Data Engineering: Migrating Hadoop to the cloud. Low differentiation. Valuation: 8x EBITDA.

- Lakehouse Implementation: Setting up Delta Lake and Unity Catalog. High demand, medium scarcity. Valuation: 10x-12x EBITDA.

- Generative AI & MosaicML: Building custom agents on proprietary data. Extreme scarcity. Valuation: 14.5x+ EBITDA.

For Portfolio Operating Partners, the play is clear: if you hold a data consultancy, you must move them up this value chain immediately. A firm generating $20M revenue from Spark jobs is a good business; a firm generating $20M revenue from deploying AI agents on MosaicML is a strategic asset. The Vertex AI Premium we see in the GCP ecosystem mirrors this trend—buyers are paying for the "Agentic DNA," not just the engineering headcount.

The Unity Catalog Wedge: Governance as IP

The most overlooked driver of valuation in the Databricks ecosystem is Unity Catalog. To the uninitiated, data governance sounds like a low-value compliance task. To a strategic acquirer, it is the "wedge" that locks in the customer for a decade. Unity Catalog is the gatekeeper for all data and AI assets within the Lakehouse. A partner that owns the Unity Catalog implementation owns the roadmap for every subsequent AI project.

The "Brickbuilder" Exit Strategy

To command the 14.5x multiple, founders must transition from "Staff Augmentation" to "Solution Accelerators"—what Databricks calls "Brickbuilders." PE buyers are allergic to pure services revenue that walks out the door every evening. They want Intellectual Property.

This doesn't mean you need to build a SaaS product. It means packaging your repeated service motions into deployable code accelerators. If you have a financial services practice, package your fraud detection models into a reusable library. If you serve retail, package your recommendation engine. Firms with documented, reusable IP trade at a 2-3 turn premium over pure services firms. As detailed in our Snowflake Partner Valuation Guide, the market rewards "Data Products," not just billable hours.