The practical answer

- Short answer

- Dynamics 365 partner valuations range from 4x to 12x EBITDA. Discover the 3 specific levers that drive premium multiples for PE-backed implementation firms.

- Best fit

- Industry: Tech Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x Target EBITDA multiple for IP-led Dynamics partners

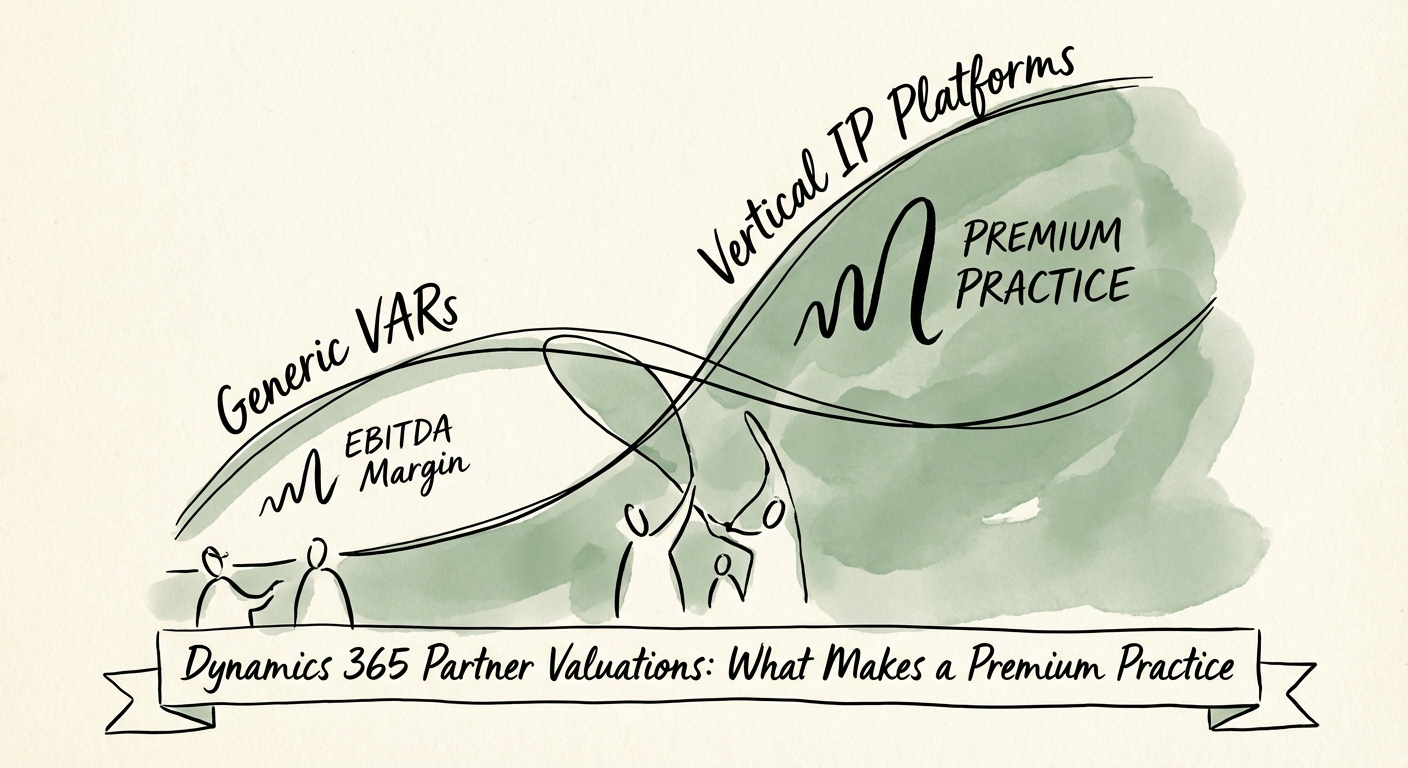

The Tale of Two Multiples: Service Shops vs. Platforms

In the current M&A landscape, the spread between median and top-quartile valuations for Microsoft Dynamics 365 partners has never been wider. We are seeing a bifurcation in the market that is punishing generic implementation firms while rewarding specialized platforms with software-like multiples.

On one side, you have the Generic VAR (Value Added Reseller). This firm trades at 4x–6x EBITDA. They chase every RFP, rely heavily on one-time implementation revenue (60%+ of mix), and their "managed services" are really just ad-hoc support hours disguised as a retainer. Their margins on services hover around 35%, dragged down by the high cost of "hero" talent needed to fix bad deployments.

On the other side is the Vertical IP Platform. This firm trades at 10x–12x EBITDA—sometimes higher if they have cracked the code on proprietary IP. They don't just implement Dynamics; they sell a pre-configured Manufacturing Accelerator or a Healthcare Compliance Layer. Their revenue mix is >40% recurring (high-margin Managed Services + IP), and their gross margins on services exceed 50% because they are deploying standardized code, not custom art.

For Private Equity Operating Partners, the goal is not just to acquire a partner; it is to engineer the transition from the former model to the latter before exit. The market is no longer paying premiums for simple capacity. It is paying for repeatable outcomes.

The market is no longer paying premiums for simple capacity. It is paying for repeatable outcomes wrapped in IP.

The Three Drivers of a Premium Valuation

1. IP Co-Sell and Verticalization

Generalist partners are commodities. The premium multiple

belongs to partners who own IP Co-Sell Ready solutions. This isn't

just a badge; it's a distribution moat. When a partner has a certified IP solution

(e.g., an automated billing engine for Dynamics Finance) listed on the Microsoft

AppSource, they gain access to Microsoft's own sales force.

The

Metric: Premium firms generate >15% of their revenue from proprietary IP

with gross margins >80%. If your portfolio company is purely selling hours, you

are capped at a 6x multiple. See our analysis on IT

Services Valuation Trends for more detail on this split.

2. High-Quality Recurring Revenue (Managed Services > CSP)

Not all recurring revenue is created

equal. Many partners puff up their ARR numbers with Cloud Solution Provider (CSP)

license margins. But with Microsoft tightening margins and incentives, CSP revenue

is low-quality—often trading at lower

multiples than true Managed Services.

The Metric: Buyers

look for a Managed Services to License Ratio of 3:1. For every

dollar of margin you make on reselling the license, you should be making three dollars

on high-margin, sticky managed services contracts (e.g., release management, automated

testing, security monitoring). This proves you own the customer relationship, not

just the billing line item.

3. Delivery Standardization (The "Anti-Hero" Model)

The biggest risk in a Services acquisition is key-person dependency. If your portfolio company requires a $250k/year Solution Architect to be involved in every project to prevent failure, your scalability is broken. Premium valuations are awarded to firms that have "productized" their service delivery—using standard operating procedures (SOPs) and code libraries that allow mid-level resources to deliver senior-level outcomes.

The "Deal Killers" in Dynamics Due Diligence

Even if the top-line growth looks good, we frequently see deals collapse or re-trade during the Quality of Earnings (QofE) phase due to three specific operational risks.

1. Project Concentration Risk

If one massive implementation project accounts for >20% of revenue, you don't have a business; you have a contract. We often see firms ramp up for a massive "whale" client, distorting their utilization and EBITDA for 12 months. When that project goes live (or pauses), the P&L collapses. Buyers will normalize EBITDA by removing these outliers, often resulting in a 30% valuation haircut.

2. The "Customization" Trap (Technical Debt)

In the Dynamics ecosystem, there is a fine line between "tailored" and "unsupportable." Partners that build heavy custom code for clients create environments that break with every Microsoft "One Version" update. During technical due diligence, we look at the code. If we see excessive customization (violating EBITDA quality standards by creating future support liabilities), we deduct the estimated remediation costs from the purchase price.

3. Phantom Utilization

Are your consultants actually billable, or are they "busy"? We often find utilization rates reported at 85%, but effective realization rates at 60% due to write-offs and non-billable rework. A premium practice tracks Effective Rate per Hour rigorously. If your effective rate is dropping while utilization is stable, your team is churning hours to fix their own mistakes.