The practical answer

- Short answer

- NetSuite partners are top PE targets in 2026. Discover why valuations are hitting 12x EBITDA, the specific metrics driving the premium, and the 'Time & Materials' trap to avoid.

- Best fit

- Industry: Technology Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12.8x Median EBITDA multiple paid by Private Equity for high-performing IT Services firms in 2025.

The 'Digital Backbone' Thesis

In 2026, Private Equity firms aren't just buying software companies; they are buying the installers of the software. Specifically, the NetSuite ecosystem has become a primary hunting ground for middle-market sponsors. The math is simple: Oracle NetSuite revenue hit $1.0 billion in Q4 Fiscal 2025, growing at 18% year-over-year. It is the default operating system for the exact mid-market companies ($10M-$200M revenue) that PE firms acquire. By rolling up the partners who control these implementations, sponsors gain a strategic leverage point over the broader mid-market.

For a PE Operating Partner, acquiring a NetSuite solution provider isn't just a services play; it's a platform play. The data supports this aggression: while corporate acquirers are paying a median of 9.9x EBITDA for IT services firms, Private Equity sponsors are paying a premium 12.8x EBITDA. Why the gap? Because smart sponsors see what founder-owners often miss: the ability to convert "one-time implementation" revenue into "recurring digital transformation" revenue.

The Consolidation Driver

We are seeing a massive consolidation wave. A typical PE thesis involves acquiring a "Platform" partner with $20M+ revenue and bolt-on smaller, regional shops ($2M-$5M revenue). The goal is to reduce subsidiary count—often taking a portfolio of 30+ disparate ERP instances and consolidating them into a single, standardized NetSuite environment. Owning the partner that executes this consolidation provides both cost synergy and execution certainty.

You stop being a services firm and start being a platform when you stop selling 'hours' and start selling 'outcomes'. The market pays 4x for hours. It pays 12x for outcomes.

The Valuation Delta: 6x vs. 12x

Not all revenue is created equal. I see founders celebrating $15M in revenue, not realizing that their valuation is capped at 5x-6x EBITDA because 90% of that revenue is "Time & Materials" (T&M) implementation work. The partners commanding 12x+ multiples have fundamentally different revenue architecture.

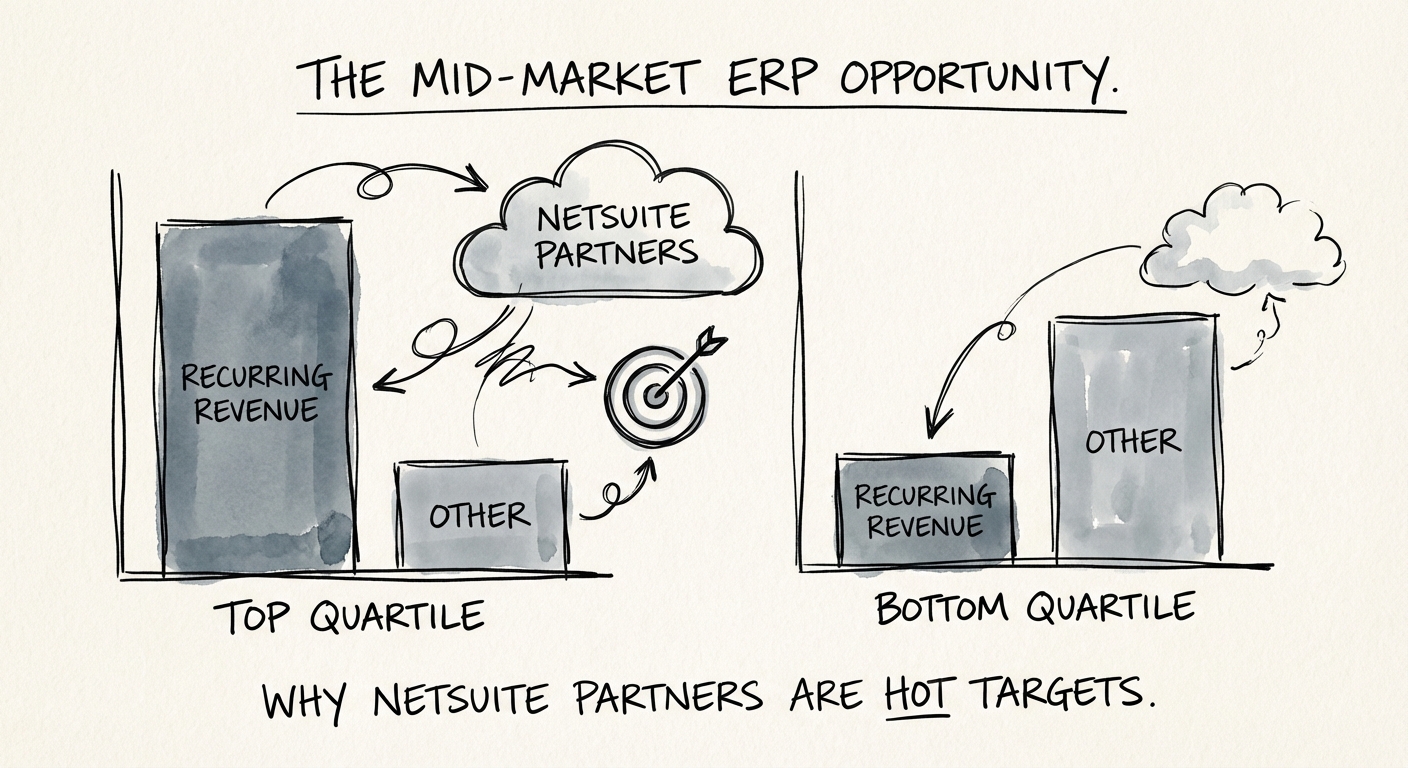

The Metric That Matters: Recurring Revenue Mix

The average IT services firm has a recurring revenue mix of ~15-18%. The top quartile—the ones getting the premium exits—push that number above 30%. They do this by shifting from "hourly support" to "Managed Services Subscriptions" (MSP). Instead of charging $250/hour to fix a broken workflow, they charge a flat $5,000/month for "Optimization & Governance." This shift moves the valuation multiple from a services band (4x-8x) to a SaaS-hybrid band (10x-15x).

Furthermore, valuation is driven by IP ownership. Partners that have built proprietary "SuiteApps" or micro-vertical accelerators (e.g., "NetSuite for Medical Device Manufacturing") break the linear link between headcount and revenue. If your revenue growth requires linearly hiring more consultants, your margins will eventually compress. If you sell IP that sits on top of the ERP, your margins expand.

For a deeper dive on how valuation multiples are calculated in this sector, read our guide on IT Services M&A: Valuation Multiples and Deal Structure Trends 2025.

The 'Generic Partner' Trap

The biggest risk in this ecosystem is the "Generalist Shop." These firms take any client, anywhere, for any project. They have high revenue volatility and low gross margins (often <40% on services). In Due Diligence, these firms get shredded. We typically see a 20-30% valuation haircut applied post-LOI when we discover that the "Customer Success" team is actually just sales reps in disguise, and that customer retention is purely relationship-based (Founder-led) rather than process-based.

The Exit Readiness Checklist

If you are a NetSuite partner looking to exit, or a PE firm looking to acquire one, look for these three "Green Flags":

- Gross Margins > 50%: Indicates high IP mix or efficient, documented delivery processes.

- Revenue Per Billable Head > $250k: Shows strong pricing power and utilization management.

- Client Concentration < 15%: No single client can kill the business.

Without documented processes, you aren't selling a business; you're selling a job. Acquirers pay a massive premium for transferability. See our analysis on The Transferability Premium to understand the math behind this.

Finally, do not ignore the financial hygiene. Revenue recognition in long-term implementation projects is a minefield. Read The Revenue Recognition Trap (applies equally to NetSuite) to ensure your EBITDA is real before you go to market.