The practical answer

- Short answer

- A PE diligence read on Azure partners: why the 70-point Partner Capability Score, ACR growth, and audited Advanced Specializations decide 6x vs. 12x.

- Best fit

- Industry: IT Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x EBITDA multiple for Azure partners with Advanced Specializations (AI, Kubernetes) vs. 6x for generalists.

The deal that died at 68 points

A few years back I watched an Azure practice go to market at a clean 8x trailing EBITDA. Solid bookings, a partner logo on every slide, a founder who could talk cloud architecture for an hour without notes. The QofE team didn't kill it. The Microsoft Partner Center dashboard did. Their Partner Capability Score had drifted to 68 — two points under the line — and nobody on the sell side had clocked what that meant. Below 70, the partner designation lapses, and with it the back-end rebates and co-op incentives that were quietly carrying roughly a fifth of the firm's margin. The "8x business" was an asset with a hole in the floor that nobody had measured.

This is the thing about valuing Azure partners that trips up generalist buyers: the badge on the website is not the asset. Under the Microsoft Cloud Partner Program, a Solutions Partner designation isn't earned once and framed on the wall — it's a rolling algorithmic verdict. The Partner Capability Score tallies up to 100 points across three buckets that map almost perfectly onto what you actually care about as an owner: Performance (net new customer adds — do they still sell?), Skilling (intermediate and advanced certifications — is the bench real?), and Customer Success (usage growth and active deployments — or is the software shelfware?).

Seventy is the cliff. And here's what makes it a financial number, not a marketing one: a partner sitting at 71 with a renewal 30 days out is a fundamentally different risk than one sitting at 85. The first one can lose incentive eligibility in month one of your ownership because a couple of certified engineers quit or a single large customer churned. So the first diligence move isn't a question — it's a screenshot. Pull the Partner Center Insights view, dated inside the last week, and read the trailing score curve. If it's anywhere under 75, you are not buying a platform. You are buying a remediation project, and you should be paying remediation prices.

A partner who passed the 70-point score with rented certifications isn't a platform — it's a payroll liability with a renewal clock, and the clock starts the day you wire the money.

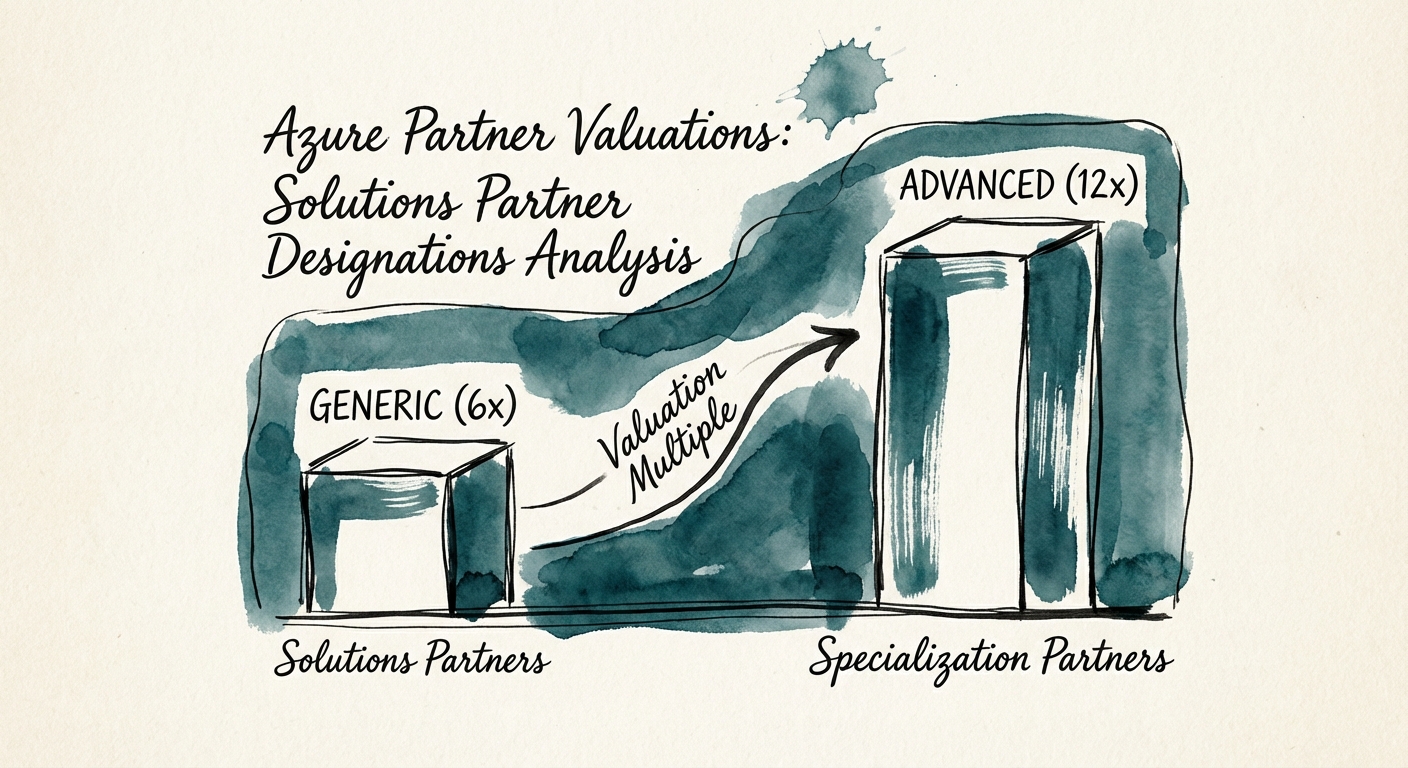

Two firms, same logo, half the multiple

Put two Azure partners side by side. Both display the partner designation. Both do roughly $12M in revenue. One trades around 6x. The other clears 12x. The logo tells you nothing about which is which — but three numbers in Partner Center tell you everything.

The first firm holds a baseline Solutions Partner for Infrastructure designation and lives on project work: lift-and-shift migrations, a VM estate stood up, an invoice cut, on to the next deal. Revenue is lumpy and re-competed constantly. There's nothing wrong with the work, but it's a commodity, and commodities get commodity multiples — call it the high-6x range that the broader Microsoft partner valuation market assigns to undifferentiated IT services.

The second firm carries an Advanced Specialization — and the distinction is not cosmetic. You don't self-attest your way into one. Microsoft puts you through a third-party technical audit, which is exactly why the designation behaves like a moat instead of a sticker. The specializations that move multiples are the ones that imply the partner is wired into the customer's daily operations and can't be ripped out on a renewal:

- Azure Virtual Desktop: once a client's workforce logs in through your environment every morning, switching costs are brutal — that's stickiness you can underwrite.

- Kubernetes on Azure: signals genuine modernization and DevOps depth, not just moving servers. These engagements run for years, not quarters.

- AI and Machine Learning: the current premium driver. Pair an audited AI specialization with proprietary IP and you're underwriting expansion revenue, not project backlog — which is what pushes the top of the range toward 12x.

The trap is treating the AI specialization as a multiplier you can apply on its own. It isn't. An AI badge sitting on top of one-off pilot engagements is still project revenue wearing a more expensive jacket. The multiple lives in the recurring, audited, consumption-tied work underneath it. For how those technical capabilities actually translate to exit value, see our breakdown of The Azure Multiplier.

Four exports that beat any management presentation

Skip the deck. The management presentation is the seller's story; the Partner Center exports are the data the seller can't edit. Here's what I pull, in order, and what each one is actually testing.

1. The Partner Association report — is the bench owned or rented? Plenty of firms pass 70 by stacking certifications held by contractors brought on to clear the threshold. Read tenure. If 40% of certified professionals are contractors or have been on payroll under six months, the "capability" you're buying walks out the door every evening and is under no obligation to come back after close. This is the single biggest post-deal retention risk in the category, and it's invisible on a P&L.

2. Azure Consumption Revenue trend — booked vs. consumed. ACR is the number Microsoft actually rewards, and the gap between it and booked revenue is diagnostic. If bookings are flat but ACR is climbing 30% year over year, the install base is expanding under its own weight — that's the expansion revenue you want to pay for. If revenue grows while ACR stays flat, they're moving low-margin licenses, not driving usage, and the growth story is hollow.

3. The Score Simulator export — how close to the cliff, and how fast is renewal coming? Designations renew annually. A partner at 71 points with renewal inside 30 days is a different underwriting case than one with a comfortable buffer and a year of runway. Model the scenario where their two strongest certified engineers leave: does the score hold, or does it fall through 70 and take the incentives with it?

4. Front-end vs. back-end incentive mix — how fragile is the margin? Request the split. Durable revenue — managed services, consumption-tied recurring work — shouldn't depend on Microsoft's rebate programs to be profitable. If back-end rebates and incentives clear 25% of EBITDA, you're not underwriting a business, you're underwriting a program-eligibility status that can shift with the next channel update. The CFO commentary in Microsoft's recent earnings — pointing at "partner motion" as a swing factor in Azure performance — is a reminder that the incentive structure underneath these firms is set in Redmond, not in the boardroom you're buying into.

Run those four and you'll know within an afternoon whether you're looking at a specialist with a moat or a generalist with a logo. For the broader pattern of what to flag before you sign, read our list of 10 Red Flags in Technology Due Diligence That Kill Deals, and for how the same dynamics play out in an adjacent ecosystem, our analysis of Microsoft Dynamics Partner Valuation Multiples.