The practical answer

- Short answer

- Two $20M IT services firms, same revenue — one sells at 13x, one at 5x. The 2025 data on PE vs. corporate multiples, the earnout trap, and how to engineer the spread.

- Best fit

- Industry: IT Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

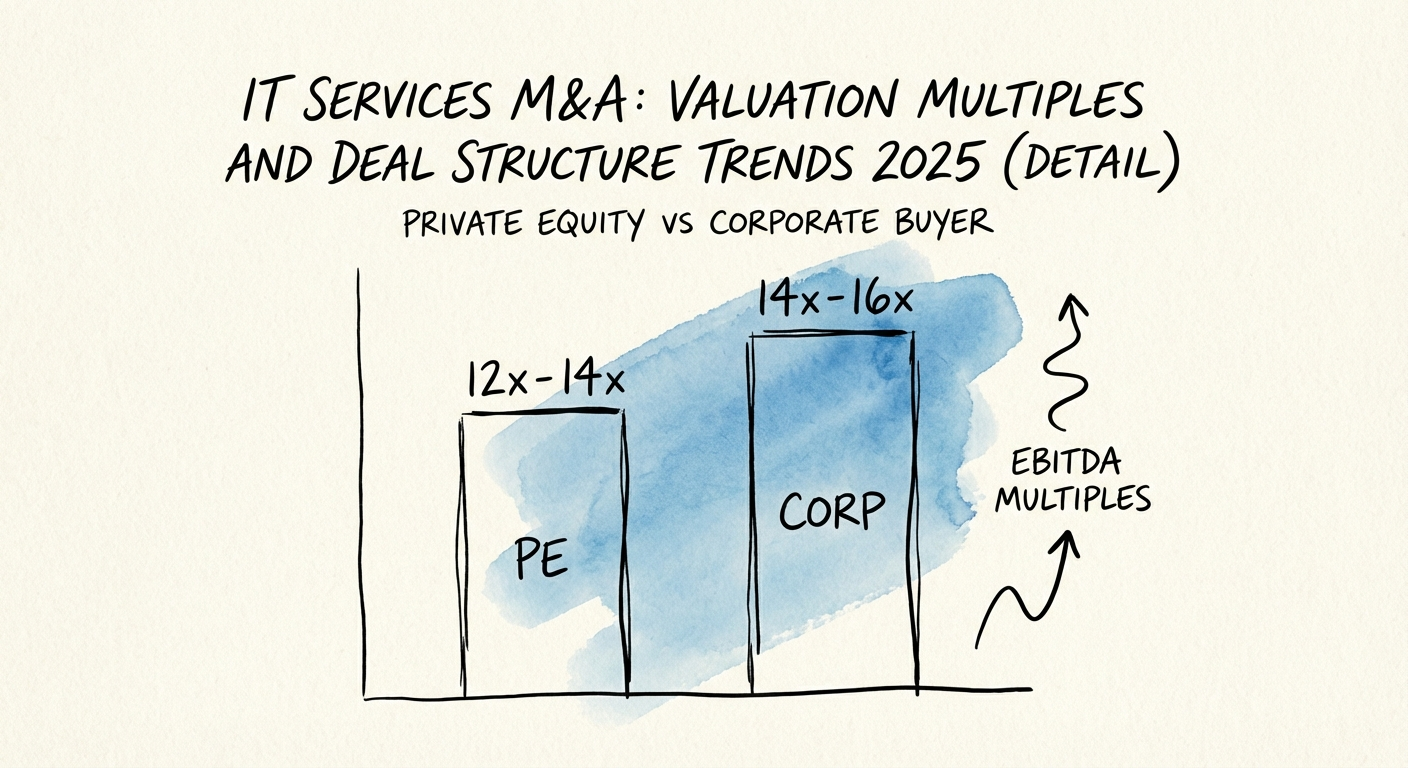

- 10.1x Avg PE Multiple (vs 8.6x Corporate)

Same revenue, same headcount, an 8-turn gap

Picture two IT services firms going to market this year. Both do $20M in revenue. Both run around 15% EBITDA, roughly $3M. Both have a founder who still closes the biggest deals and a handful of senior engineers everyone leans on. On a one-page teaser, they look like the same company.

One signs an LOI at roughly 13x. The other fights to hold 5x — and most of that is back-loaded into an earnout the founder may never fully collect. The difference isn't size, sector, or even profitability. It's what survives the founder walking out the door.

This is the split that defined IT services M&A in 2025. The median EV/EBITDA multiple has settled around 8.8x per Aventis Advisors' Q2 2025 data — a sane number after the 2021 peak. But the median is a fiction nobody actually transacts at. The real market is two markets. IP-led cybersecurity, vertical SaaS, and sticky managed-services books clear at 12x–14x. Generalist staff augmentation, break/fix, and project-shop consultancies get pushed down to 4x–6x, structured so the buyer keeps the risk and you keep the hope. If you run a portfolio company still billing hours without a layer of recurring revenue or proprietary tooling underneath it, you don't own a growth asset. You own a depreciating one — and the clock on it is louder than you think.

Buyers in 2025 aren't paying for revenue. They're paying for what stays after you and your top three engineers walk out the door — and on a staff-aug shop, that's almost nothing.

The two things buyers are actually pricing

The 2025 data breaks the comfortable old story that strategics always pay up. They don't right now. PitchBook and CLFI figures show private equity sponsors outbidding corporate acquirers for platform-grade IT services assets — averaging 10.1x EBITDA against 8.6x for corporates. The reason is structural, not sentimental: PE is sitting on a wall of uncommitted capital and needs platforms it can bolt acquisitions onto, while corporate development teams are buying for cost takeout and won't pay for a story they have to underwrite themselves. If your firm can credibly be a buy-and-build hub, your most aggressive bidder is probably a sponsor, not a competitor.

Then check the structure, because the headline multiple is half the negotiation. The risk has migrated almost entirely onto the seller. SRS Acquiom's 2025 Deal Terms Study finds that 68% of private-target deals now carry multiple earnout metrics — not just a revenue trigger, but stacked tests on logo retention, EBITDA margin, and gross margin held in tandem. The clean old "half cash, half earnout on revenue" handshake is gone. Buyers now gate your payout on the exact operating discipline that founders of services firms tend to ignore until diligence forces the issue, including a defensible Quality of Earnings position. Here's the practical decoder for where a 2025 IT services firm lands:

- IP-led (cyber, data, applied AI): 12x–14x EBITDA, heavy cash at close. You're being bought for the asset, not the people.

- Recurring managed services: 8x–10x EBITDA, standard earnout. Priced on net revenue retention and contract length.

- Staff aug / VARs / project shops: 4x–6x EBITDA, deep earnout plus a seller note. You're financing your own buyer.

Notice the pattern: the further left your revenue sits on the "stays without me" spectrum, the more of the purchase price you actually get to keep at signing.

How to move from the 5x list to the 13x list

You can't financial-engineer a commodity multiple. But you have an 18-to-24-month runway to rebuild the chassis underneath the same revenue, and three moves do most of the work.

Convert the revenue mix before the buyer does the math for you. A dollar of project revenue is worth roughly $0.80–$1.20 in enterprise value. A dollar of contracted recurring services is worth $4–$6. So a $20M firm doing $15M in projects and $5M in managed services is, in a buyer's model, a project shop wearing a managed-services hat. Flipping that ratio is the single highest-leverage thing you can do — and it's slow, which is exactly why you start now. Productize your most repeatable engagement into a fixed monthly subscription. Move clients onto annual contracts with auto-renew. Track the recurring share as a board metric every month, the way you'd track any other value driver.

Make the founder removable. Most of the discount on lower-multiple firms is a key-person tax. Buyers in 2025 run forensic diligence on it: if the founder leaves, does the pipeline leave with them? If your sales engine depends on one person's relationships and instinct, your ceiling is roughly 5x. If it runs on a documented motion anyone can execute, the ceiling lifts toward 10x. Start a deliberate founder extraction program now — name a second person on every key account, write down how you actually win deals, and prove the machine runs for two quarters without you in the room.

Run your own Quality of Earnings 12 months before the LOI. Adjusted EBITDA is the battlefield, and you do not want to discover your number is soft after a buyer has anchored on it. If you present $5M of EBITDA that diligence whittles to $3M over weak capitalization policy or owner add-backs that don't survive scrutiny, you lose far more than the two turns — you lose the buyer's trust in every other number on the page. Commission a sell-side QofE a year out and clean the dirty metrics on your own schedule, not theirs. The window for exiting mediocrity has closed. The window for exiting systematic, transferable infrastructure is wide open. Pick which list you want to be on, and build for it.