The practical answer

- Short answer

- MSP valuation multiples by vertical in 2025: generalists 4.5–6.5x, healthcare 9–12.5x, FinTech 10–13x. Why compliance moats drive the 4.2x spread.

- Best fit

- Industry: Managed Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12.5x Top-quartile EBITDA multiple for Healthcare MSPs with proprietary compliance IP.

The Great Bifurcation: 2025 MSP Valuation Benchmarks

In 2025, the phrase "MSP" has become too broad to be useful for valuation purposes. Private equity buyers have bifurcated the market into two distinct asset classes: Commodity Generalists and Vertical Fortresses. The valuation gap between these two groups has widened to a historic 4.2x spread on EBITDA.

Our analysis of 2025 transaction data reveals that while generalist MSPs are seeing multiples compress due to AI-driven commoditization of Level 1 support, vertical specialists are commanding "SaaS-like" premiums. Buyers are no longer paying for management; they are paying for domain expertise that creates defensive moats around recurring revenue.

2025 EBITDA Multiples by Vertical (>$2M EBITDA)

| MSP Vertical Focus | EBITDA Multiple Range | Key Valuation Drivers |

|---|---|---|

| Generalist / SMB | 4.5x - 6.5x | Low barriers to entry, high churn risk from AI. |

| Healthcare (HCLS) | 9.0x - 12.5x | HIPAA/HITECH defensibility, EHR integration stickiness. |

| FinTech / Financial Services | 10.0x - 13.0x | SEC/FINRA compliance reliance, high cost of switching. |

| Legal / Professional Services | 7.5x - 9.5x | DMS specialization (iManage/NetDocuments), high ARPU. |

| Manufacturing / Industrial | 7.0x - 8.5x | OT/IT convergence expertise, IoT integration. |

The data is clear: Specialization is the new scale. A $3M EBITDA Healthcare MSP is now trading at a higher absolute dollar value than a $5M EBITDA Generalist. The market is discounting "width" and paying a premium for "depth."

The market has stopped paying for 'Managed Services' and started paying for 'Managed Risk.' If you aren't solving a specific regulatory or vertical problem, you are essentially selling a commodity utility, and you will be valued like one.

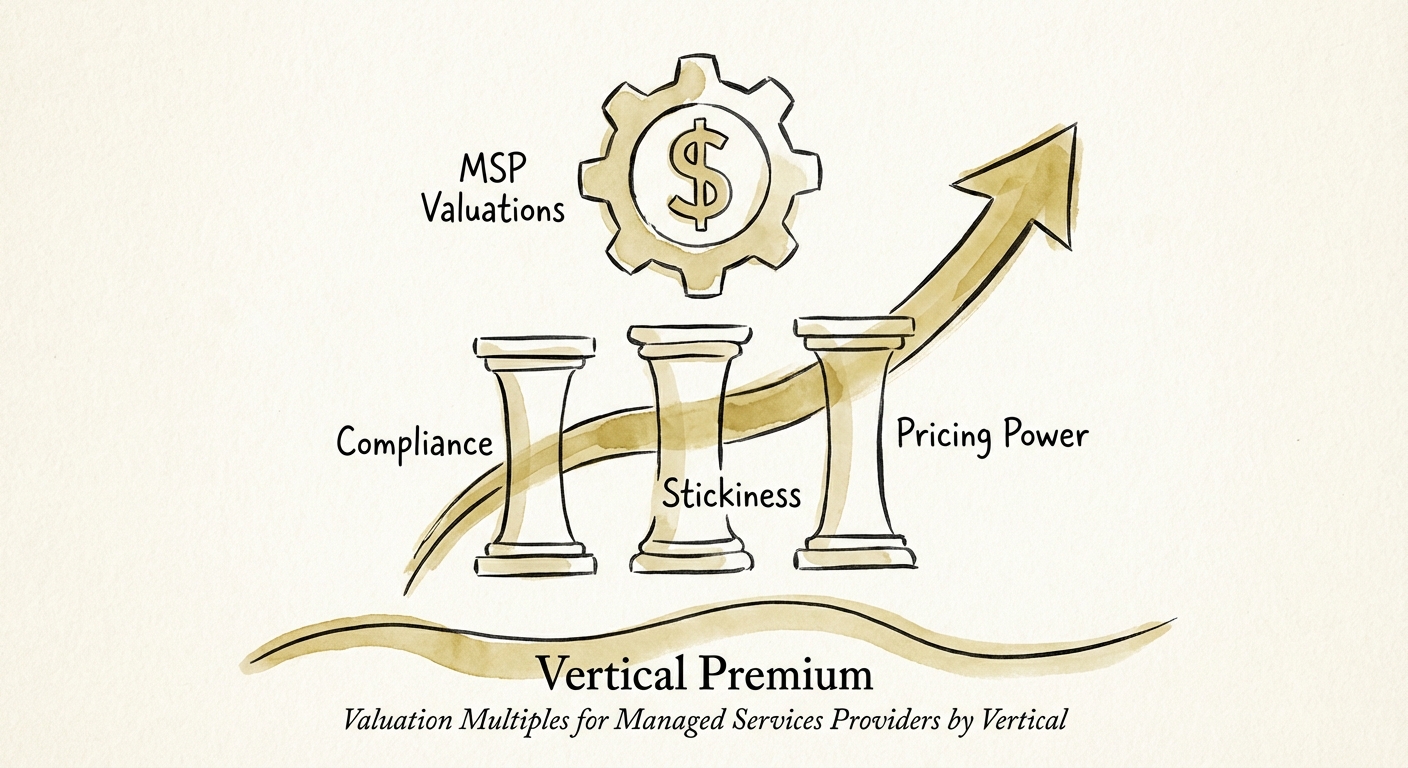

The Drivers of the Vertical Premium

Why does a Healthcare MSP command a 12x multiple while a Generalist stalls at 6x? It is not just about revenue growth; it is about the quality of the revenue and the defensibility of the gross margin.

1. The Compliance Moat (The "Must-Have" Factor)

For a generalist MSP, IT is a utility—a cost center to be minimized. For a FinTech or Healthcare MSP, IT is a regulatory requirement. When you manage the cybersecurity posture for a registered investment advisor (RIA) subject to SEC cybersecurity rules, you are not just fixing printers; you are keeping their license to operate valid. This shifts the relationship from "vendor" to "partner," reducing churn to near-zero levels.

2. Inherited Stickiness

Vertical MSPs inherit the stickiness of the platforms they support. A generalist supporting Microsoft 365 is easily replaceable. A specialist managing the integration between Epic EHR and a localized PACS imaging system is effectively permanent. The technical debt involved in ripping out a specialist provider is too high for most clients to stomach, granting the MSP immense pricing power.

3. The "Subject Matter Expert" Pricing Power

Generalists compete on price per seat (often compressing to $100-$120/user). Vertical specialists compete on outcome and compliance assurance, often commanding $250-$350/user. This structural pricing advantage flows directly to EBITDA, allowing specialists to maintain 25%+ EBITDA margins even while investing heavily in talent.

From Generalist to Specialist: The Pivot Playbook

If you are holding a generalist MSP portfolio company trading at 5x, the path to a 10x exit involves a strategic pivot, not just "more sales." You cannot simply rebrand; you must re-architect the revenue mix.

Step 1: The 80/20 Audit

Analyze your current customer base. You likely have an accidental specialization. If 30% of your revenue comes from regional banks, you are a FinTech MSP in disguise. Isolate these customers, calculate their gross margin relative to the generalist pool, and reorient your GTM strategy to double down on this segment.

Step 2: Productize Compliance

Stop selling "Managed Security." Start selling "SOC 2 Readiness" or "HIPAA Compliance-as-a-Service." By wrapping your services in a compliance framework, you decouple your pricing from the "hours worked" and attach it to the "risk reduced."

Step 3: Acquire for Density

Instead of acquiring another generalist in a new geography (the old playbook), acquire a smaller player with deep expertise in your target vertical. Use M&A to buy the "badge" and the case studies you need to credibly claim specialization. The market rewards this Vertical Density far more than geographic sprawl.

The Bottom Line: In the current market, you cannot afford to be everything to everyone. The "Generalist Discount" is real, and it is growing. Pick a lane, build the moat, and unlock the double-digit multiple.