The practical answer

- Short answer

- New 2026 data: How compliance debt erodes fintech multiples. A diagnostic guide for PE Operating Partners on AML, BaaS, and SOC 2 deal impacts.

- Best fit

- Industry: FinTech. Function: Operations

- Operating path

- Compliance & Security → Turnaround & Restructuring → Turnaround & Restructuring Services

- Key metric

- 19% Average percentage of revenue spent on compliance/risk by regulated fintechs in 2025.

The New "Quality of Compliance" Adjustments

In 2021, you could sell a fintech on growth alone. The "move fast and break things" era allowed founders to treat compliance as a post-Series C problem. In 2026, that mindset is a deal-killer. Buyers have shifted from purely financial Quality of Earnings (QoE) to what I call Quality of Compliance (QoC) audits. If your portfolio company's growth was fueled by ignoring AML thresholds or renting a charter without oversight, that revenue isn't just low-quality—it's a liability.

We are watching the market split in two. According to recent 2025 M&A data, fintechs with "Regulatory Clarity"—defined as clean audits, SOC 2 Type II, and documented banking partner oversight—are trading at a stable 4.2x revenue multiple. Those without? They aren't just trading lower; they are failing to transact. 87% of successful Q4 2025 deals had their compliance infrastructure fully documented and validated before the LOI was signed. The market is no longer pricing in "potential"; it is pricing in "risk reduction."

The Hidden EBITDA Drag

Many Operating Partners look at compliance spend as a line item to minimize. This is a mistake. In 2025, small-to-mid-sized fintechs spent upwards of 0.83% of total assets on AML/KYC remediation. If you haven't made that investment, the buyer will—and they will deduct it from your purchase price at a premium. I recently watched a deal for a payments processor stall because the buyer's diligence team identified \$2M in necessary "remediation CAPEX" to fix a leaky KYC process. That wasn't just a \$2M hit to the closing cash; it compressed the multiple because it cast doubt on the entire customer base's validity.

Your "rapid onboarding" process that allows customers to transact in 30 seconds? If it bypasses standard sanctions checks, it's not a feature. It's an unsalable asset. When we conduct Revenue Quality Assessments, we often find that 15-20% of "active users" in high-growth fintechs are actually bot accounts or money mules that a compliant system would have rejected. That's phantom revenue, and smart buyers are aggressively churning it out of their valuation models.

A disclosed issue with a remediation plan is a negotiation point; a hidden issue discovered by the buyer is a trust-killer.

The Three Horsemen of Deal Destruction

Through our work restructuring stalled fintechs, we've identified three specific compliance failures that are currently triggering the deepest valuation haircuts.

1. The BaaS/Partner "Shadow Risk"

The regulatory crackdown on Banking-as-a-Service (BaaS) in 2024 and 2025 fundamentally changed the operating model. The "rent-a-charter" days are over. Regulators now hold the partner bank responsible for the fintech's compliance. Consequently, banks are offboarding risky fintech programs at a record pace.

If your portfolio company relies on a single banking partner and doesn't own its compliance stack (KYC, AML, transaction monitoring), you have a single point of failure. We've seen valuations slashed by 30% simply because a fintech couldn't prove they had direct oversight of their end-users' activity. Buyers are terrified of acquiring a company that loses its ability to move money 90 days post-close.

2. The AML Data Dump

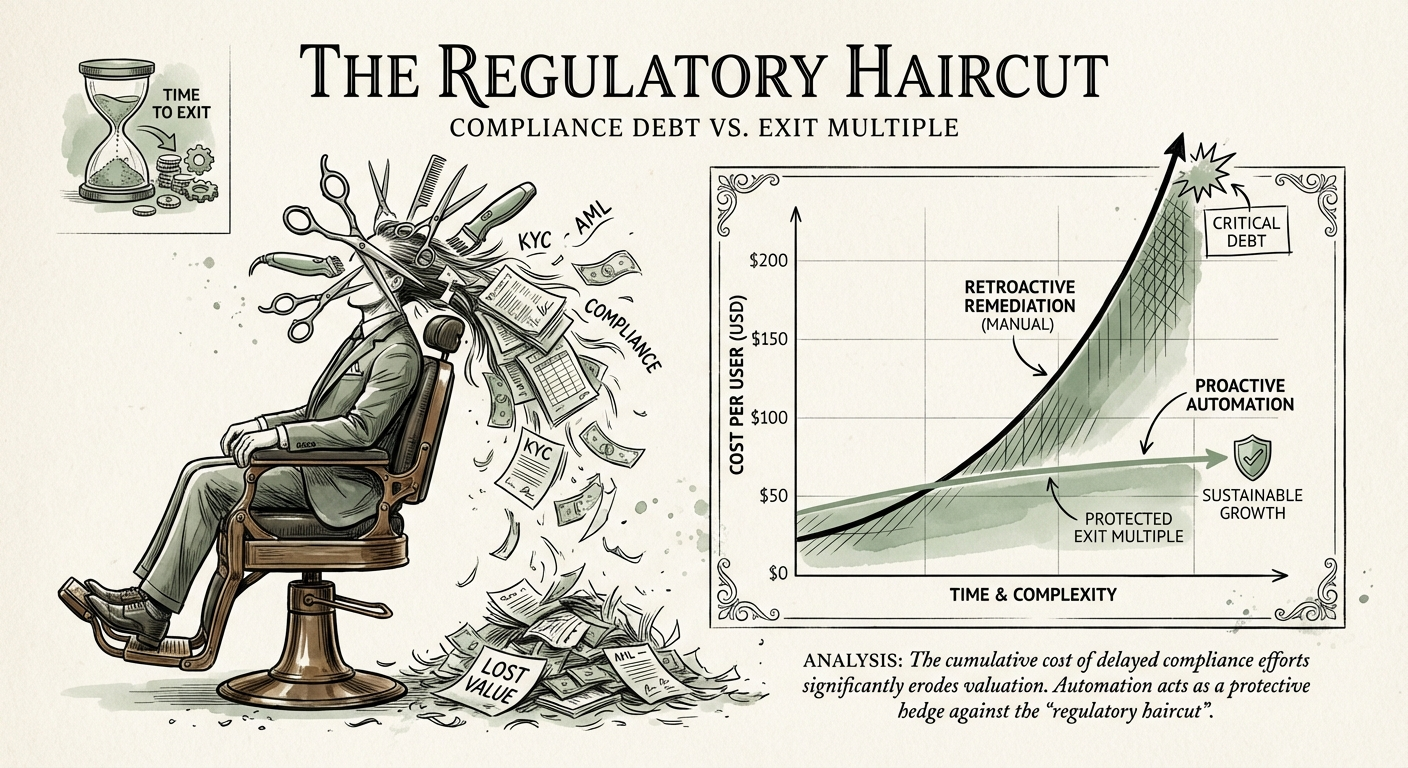

Fines for AML violations in the payments and fintech sector exceeded $160 million in 2025 alone. But the fine isn't the real cost; the remediation is. Bringing a non-compliant user base up to standard (retroactive KYC remediation) typically costs $25-$40 per user in manual review and data appending. For a consumer fintech with 500k users, that's a $12M-$20M liability sitting off-balance-sheet. PE buyers are now calculating this "Compliance Debt" and subtracting it dollar-for-dollar from the enterprise value.

3. The "AI Black Box"

If your portfolio company claims to use AI for credit decisioning or fraud detection, expect a "Model Risk Management" audit. With new frameworks like the EU AI Act and updated CFPB guidance, "black box" algorithms are a liability. Buyers need to know why the model rejected a loan to avoid fair lending violations. If you can't explain the decisioning logic, you can't sell the IP. We recently advised a lender who had to scrap their entire underwriting model—and 6 months of roadmap—because it couldn't pass a basic fairness audit during diligence.

The Remediation Playbook: Protecting the Exit

You cannot fix a broken compliance culture in the 30 days before a sale, but you can stop the bleeding and ring-fence the risk. Here is the operator's approach to cleaning up "Regulatory Debt" before you go to market.

Step 1: The Mock Regulatory Exam

Don't wait for the buyer to find the skeletons. Commission a mock audit that mimics a bank partner's review. Focus on the "flow of funds" and consumer protection. If you find gaps, self-report and remediate before the data room opens. A disclosed issue with a remediation plan is a negotiation point; a hidden issue discovered by the buyer is a trust-killer.

Step 2: Cap the "Heroics"

If your compliance team is working 80-hour weeks to clear false positives, you have a scalability problem. Document the process and invest in automation. Buyers pay for systems, not heroes. If your compliance officer is the only one who knows how to approve a high-risk transaction, that's a key-person dependency that lowers your multiple.

Step 3: Segregate High-Risk Revenue

If 10% of your revenue comes from a grey-market vertical (e.g., crypto rails, adult entertainment, high-risk gaming) that prevents you from getting a tier-1 bank partner, spin it out or shut it down. We've seen firms increase their overall valuation by cutting revenue, simply because the remaining revenue quality was high enough to attract institutional buyers. In fintech, "boring" revenue trades at 5x; "risky" revenue trades at 1x (or 0x).

Ultimately, compliance is no longer a cost center—it's your license to exit. The market has spoken: Growth without governance is worthless. Fix the foundation, and you protect the multiple.