The practical answer

- Short answer

- New 2026 data: Non-compliance costs 2.7x more than proactive governance. Learn how regulatory debt reduces fintech exit multiples and how to fix it.

- Best fit

- Industry: Fintech. Function: Legal & Compliance

- Operating path

- Compliance & Security → Turnaround & Restructuring → Turnaround & Restructuring Services

- Key metric

- 2.71x Cost multiplier of non-compliance vs. proactive governance programs

The "Growth-at-All-Costs" Hangover

You bought the growth story. The pitch deck showed a hockey stick: user acquisition costs (CAC) were low, onboarding was frictionless, and transaction volume was doubling every quarter. But six months into the holding period, you realize why the onboarding was so frictionless. The founder skipped the "heavy" parts of KYC (Know Your Customer) to boost conversion rates. Now, you don't just own a fintech; you own a regulatory latent risk.

For Private Equity sponsors, this is the 2026 reality. The era of "move fast and break things" is over in financial services. Regulators like the CFPB, SEC, and state bodies (NYDFS, California DFPI) are no longer accepting "start-up speed" as an excuse for AML (Anti-Money Laundering) gaps. When you go to sell this asset, the acquirer—likely a strategic bank or a larger, more regulated fintech—won't just look at EBITDA. They will look at your Compliance Debt.

If your portfolio company has weak AML controls, unfiled SARs (Suspicious Activity Reports), or ambiguous state licensing coverage, you aren't getting a 12x revenue multiple. You are getting a 15% valuation haircut, a 20% escrow holdback, or a deal that dies on the vine. We saw this brutally illustrated when the TD Bank/First Horizon deal collapsed due to regulatory delays, erasing billions in value. In the lower middle market, the numbers are smaller, but the ratio of pain is identical.

The market is effectively saying: 'If we have to fix your compliance mess, we are paying distress prices.'

Quantifying the Compliance Discount

Compliance is often viewed by operators as a cost center—a tax on innovation. The data proves otherwise. It is a value protector. According to 2025 benchmarks from FinTech Global, the cost of non-compliance (fines, business disruption, remediation) is now 2.71 times greater than the cost of maintaining a robust compliance program.

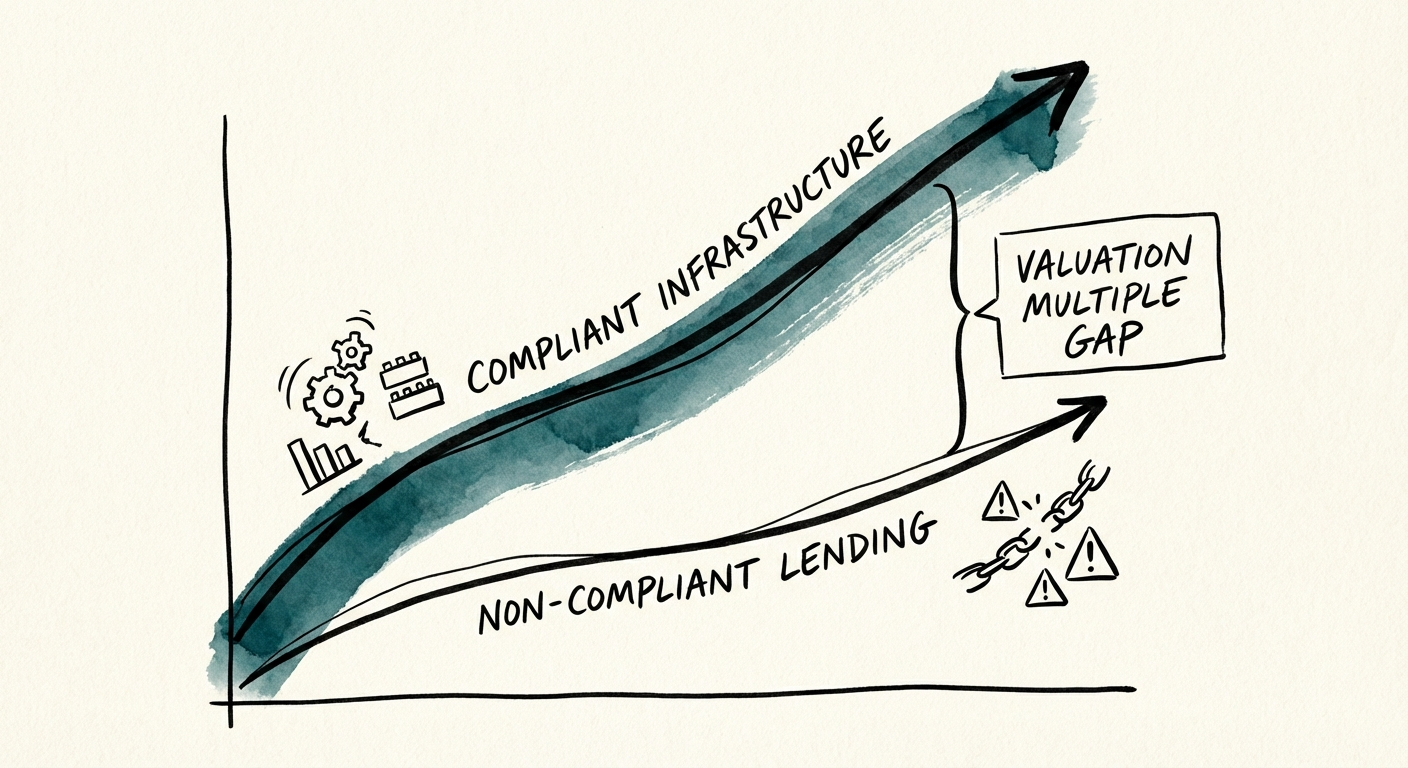

The Valuation Gap: Infrastructure vs. Lending

The market is pricing this risk directly into multiples. Recent Q4 2025 data shows a massive bifurcation in fintech valuations. While infrastructure-heavy, compliance-first platforms are trading at upwards of 17.3x revenue, lending companies with heavier regulatory burdens and perceivable risk are scraping by at 2.5x revenue. The market is effectively saying: "If we have to fix your compliance mess, we are paying distress prices."

- The Fine is Just the Down Payment: In 2024, 60% of fintechs surveyed paid at least $250,000 in fines. But the real cost is the remediation. Fixing a broken AML program requires forensic audits, back-filing years of reports, and often replacing the entire leadership team.

- Deal Timeline Expansion: Bain & Company reports that regulatory scrutiny can now extend the pre-close period from the standard 3 months to up to 2 years. In a high-interest rate environment, that delay kills IRR.

For a PE Operating Partner, this means compliance readiness isn't a legal box to check right before the exit. It is a strategic lever that must be pulled on Day 1 of the hold.

The Remediation Roadmap: Turning Risk into Multiple Expansion

You cannot hide compliance debt in a data room. Strategic buyers will deploy forensic teams to test your transaction monitoring rules and sample your KYC files. If they find the skeletons before you do, they control the negotiation. Here is the operator's playbook to fix it.

1. The "Mock Audit" Stress Test

Do not rely on the company's internal compliance officer, who may be the one who created the debt. Bring in a third-party specialist to conduct a mock regulatory exam. Specifically, test for SAR filing ratios (are you filing too few relative to volume?) and state licensing gaps (are you operating in states where you aren't licensed?). This needs to happen 18 months before you list.

2. Automate to Scale (Headcount is a Trap)

Founders often solve compliance problems by throwing bodies at them. This destroys your unit economics. If your compliance headcount is growing linearly with transaction volume, your tech stack is broken. Replace manual review queues with automated identity verification and transaction monitoring tools. This improves margins and demonstrates scalability to buyers.

3. The "Compliance Asset" Narrative

When you go to market, position your rigorous compliance as a competitive moat. Show the buyer: "We have money transmitter licenses in 50 states. It would take you 3 years to replicate this." That turns a risk factor into a premium. As noted in our guide on Cybersecurity Risks, buyers will pay a premium for "clean" assets because it de-risks their own integration.

The Bottom Line: In 2026, you are either selling a compliant fintech platform or a remediation project. The difference in valuation is roughly 6x. Choose accordingly.