The practical answer

- Short answer

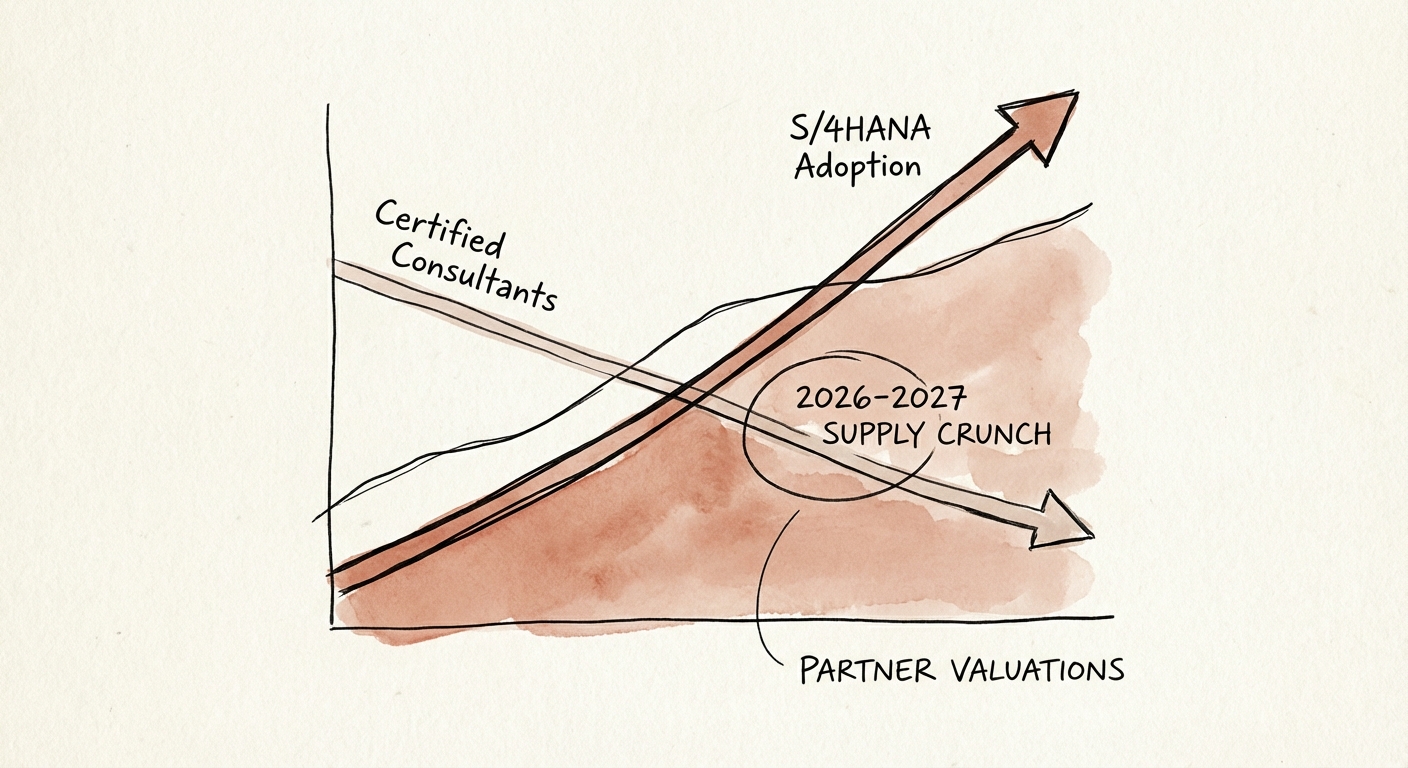

- Two SAP partners, same revenue, double the multiple. The 2027 ECC deadline split the market in two. Here's the diagnostic that decides which side you're on.

- Best fit

- Industry: Technology Services. Function: M&A

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Median EBITDA multiple for Specialized IT Consulting firms in 2025, driven by the S/4HANA scarcity premium.

Two SAP consultancies, one spreadsheet, double the multiple

Put two SAP services firms side by side. Both do roughly $40M in revenue. Both have around 300 consultants. Both are profitable. On paper, in a banker's first-pass model, they look like comps. Then the buyer's diligence team asks one question, and the valuations split clean down the middle: How many of your people can take a live ECC 6.0 client to S/4HANA before maintenance runs out?

Firm A answers with revenue charts and a logo wall. Firm B answers with a number: the count of consultants certified on S/4HANA 2023/2025 releases and on BTP, the bench they can deploy next month, the migration runbook they've productized. Firm A trades around 8x EBITDA. Firm B clears 13.6x. Same revenue. Different question answered.

The line dividing them is a date on the calendar: December 31, 2027, when mainstream maintenance for SAP ECC 6.0 ends. To a CIO that's a compliance deadline. To anyone holding an SAP consultancy in a portfolio, it's the single largest re-rating event the ERP services market will see this decade — and the window to sell into it is already half closed.

Why the gap is structural, not cyclical

Most valuation spreads narrow over time as buyers get smarter. This one is widening, because it sits on a supply-demand fracture. According to Precisely and ASUG, 59% of SAP organizations are now "live or in process" with their S/4HANA migration. Read that the other way: roughly 41% still have to move, and they all have to move through the same narrowing door. Aventis Advisors' IT services data puts generalist IT staffing around 8.8x median EBITDA and specialized cloud/S/4HANA consulting at 13.6x. Strategic acquirers — the Accentures and Deloittes, plus the PE-backed platforms rolling up the mid-market — aren't paying that spread for topline. They're buying the ability to say "yes" to a client that just realized it has eighteen months to migrate and no one on staff who's done it.

A buyer isn't paying 13.6x for your revenue. They're paying it for the number of consultants who can walk into a Fortune 500 panicking about 2027 and say "yes" by Friday. Count those people. That headcount is your multiple.

Your certification density is the number diligence actually models

The S/4HANA skills shortage gets discussed like weather — something that happens to everyone. It isn't. It's the specific lever that lets a disciplined SAP partner push day rates well above a body shop's. Resulting IT has been blunt about the math: there simply are not enough certified S/4HANA resources to migrate every remaining ECC customer before the deadline. Scarcity is your pricing power. But a buyer will only pay for scarcity they can verify, and "we have deep SAP experience" verifies nothing.

So run the one ratio that diligence runs on you. Of your consultants, what percentage hold current S/4HANA 2023/2025 certifications plus BTP credentials — not R/3, not ECC, not "ten years in SAP"? That's your certification density ratio. Below ~30%, you read as a legacy asset: a firm selling maintenance hours into a platform the vendor is actively sunsetting. The R/3 veteran who can't migrate to S/4 carries no premium; that experience is a fax repair certificate in an email world.

The three moves that detach your multiple from headcount

When we look at how IT services M&A is actually getting priced, the firms clearing the high end have done three specific things — and they're sequenced, not simultaneous:

- Re-cert or release the bench, fast. Every legacy ECC consultant is either a retraining candidate or a churn candidate. Pick within the quarter. Carrying un-certifiable headcount drags your density ratio down and your story with it.

- Productize the migration, don't just deliver it. A branded industry accelerator — say, an S/4HANA template for pharma or for discrete manufacturing — plus an automated migration-testing suite, turns a service into an asset. Documented, transferable methodology earns roughly double what an undocumented one does, because it survives the founder and the senior partners walking out.

- Convert projects into AMS contracts. A one-and-done migration is a revenue event. Multi-year Application Management Services on the S/4 stack is a revenue annuity. The same delivery capability, repriced as recurring, lifts both your revenue quality and the multiple a buyer will underwrite against it.

RISE-readiness is the difference between an implementer and a navigator

SAP has stopped being coy about where it's pushing the base: onto the cloud, through RISE with SAP. Partners still defending on-premise maintenance margins are positioned against their own vendor's roadmap, and acquirers can see it. The premium attaches to firms that can sit on the customer side of a RISE conversation — model the commercial tradeoffs, negotiate the contract, and then actually execute the technical migration. There's even reporting that SAP may extend maintenance windows toward 2033 for customers who commit to RISE, which makes the partner who can broker and run that commitment worth far more than one who can only configure modules. An implementer does the build. A navigator owns the customer's entire decision — and gets paid like it.

What to actually do between now and the sale

If you're holding an SAP partner you intend to exit, the timing is the strategy. The peak of the panic-buying curve is 2026 into 2027. Wait until 2028 and you're selling into the post-migration hangover, when the demand that justified your premium has already been consumed. A workable cadence:

- Now through Q2: Run a staff-augmentation-versus-managed-delivery review. Find every low-margin warm-bodies contract and either reprice it onto the S/4 capability or let it churn. Each one you keep dilutes the story diligence will tell about you.

- Mid-year: Formalize the IP. Brand the accelerator, document the testing suite, get the methodology out of senior consultants' heads and into a repeatable, transferable asset.

- Second half: Go to market while the 2027 fear is still a buyer's primary motivation. The forcing function that's about to panic your customers is the same forcing function that re-rates your valuation — but only if you're on the right side of the certification line when the data room opens.