The practical answer

- Short answer

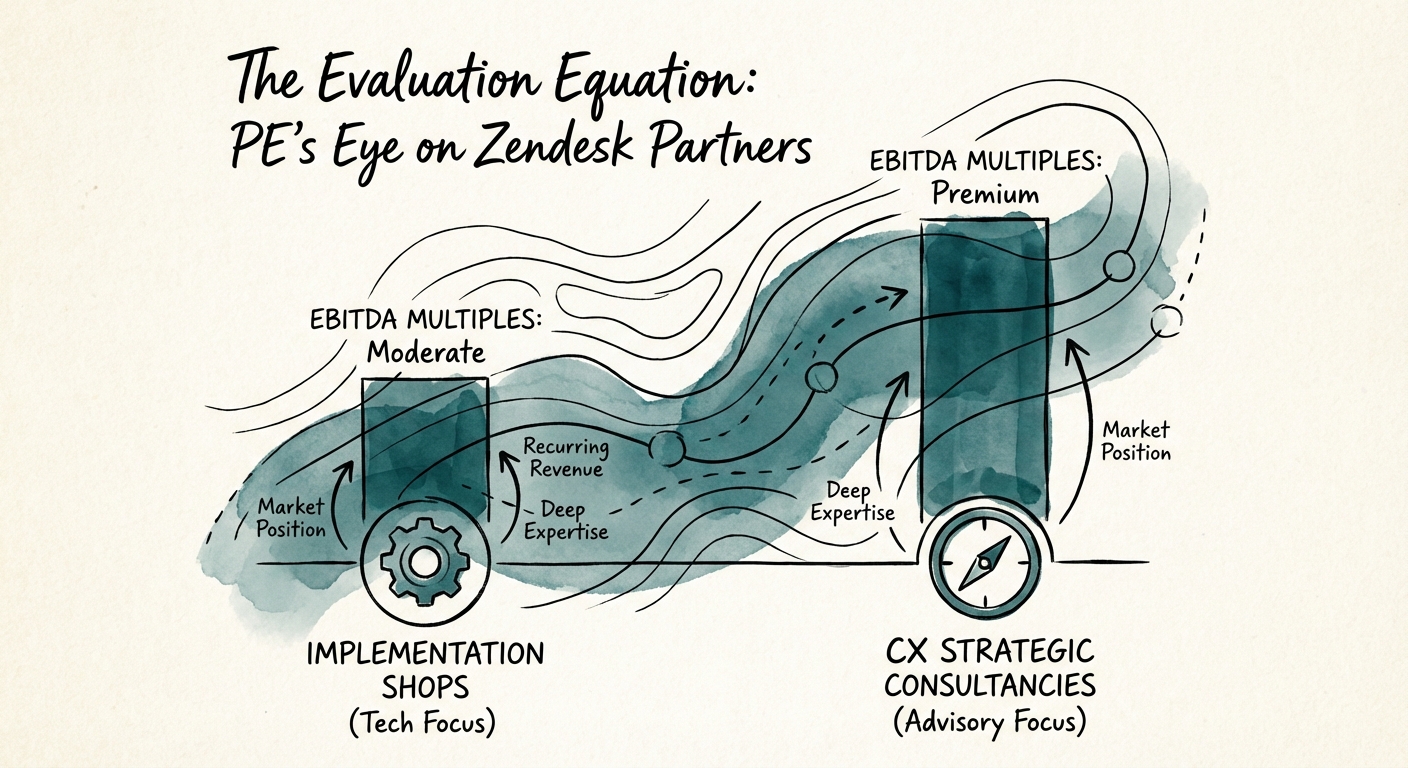

- Private Equity buyers are bifurcating Zendesk partners into 5x 'Ticket Mechanics' and 12x 'CX Architects.' Here is the due diligence framework used to value your firm.

- Best fit

- Industry: Private Equity. Function: Mergers & Acquisitions

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 115% The Net Revenue Retention (NRR) floor required to escape the 'implementation shop' discount.

The Great Bifurcation: Ticket Mechanics vs. CX Architects

In the 2026 private equity landscape, the Zendesk partner ecosystem has undergone a violent bifurcation. For years, the market treated most Zendesk partners as volume-based implementation shops—firms that could spin up a Help Center, configure a few triggers, and hand over the keys. Today, Private Equity buyers distinguish sharply between these "Ticket Mechanics" and true "CX Architects." The valuation gap between them is now a chasm: Mechanics struggle to clear 5x EBITDA, while Architects command 12x to 14x.

The driver of this split is the commoditization of basic configuration. With Zendesk's push into AI and automated agents, the value of setting up basic ticketing workflows has approached zero. PE firms conducting due diligence are no longer looking for partners who can deploy seats; they are looking for partners who can reduce them through intelligent automation while increasing customer lifetime value. If your revenue model depends on the linear scaling of human support agents, your multiple is capped.

Investors are specifically hunting for "Enterprise Complexity"—partners who drag Zendesk upmarket into the Fortune 1000. This requires technical capabilities beyond the standard admin panel: custom apps built on Zendesk Sunshine, deep AWS integrations, and data orchestration that ties support tickets to revenue outcomes in Salesforce or NetSuite. If your engineering team is primarily composed of "admins" rather than developers, you fall into the commodity bucket.

In 2026, nobody buys a Zendesk partner to configure support queues. They buy them to architect the data layer between customer service and revenue operations.

The "Quick Start" Trap and the Churn Problem

The single biggest red flag in Zendesk partner due diligence is an over-reliance on "Quick Start" packages. While these low-cost, fixed-scope implementations are excellent for lead generation, they are poisonous to Enterprise Value if they constitute the majority of revenue. PE firms analyze the "Revenue Quality" of these projects and often find them to be highly transactional with zero retention tail. A firm doing $10M in revenue via 500 Quick Starts is worth significantly less than a firm doing $10M via 50 complex enterprise transformations.

This is where the Net Revenue Retention (NRR) metric becomes the primary filter. In the 2026 market, a Zendesk partner with NRR below 100% is viewed as a staffing agency with a leaky bucket. To command a premium multiple, you must demonstrate NRR above 115%. This indicates that you are not just landing customers, but expanding them—moving them from Support to Sell, adding Sunshine custom objects, and managing their AI strategy.

Furthermore, the "Resale Trap" is particularly acute in this ecosystem. Many partners inflate their top-line revenue with pass-through licensing margins. Experienced buyers will strip this out immediately in a Quality of Earnings (QofE) analysis, isolating the "Value-Added Services" revenue. If your EBITDA margins collapse without the resale cushion, the deal structure will shift from cash-at-close to a heavy earnout.

The AI Readiness "Litmus Test"

The final, and perhaps most critical, component of the 2026 diagnostic is the "AI Readiness" of the partner's revenue stream. Zendesk's aggressive pivot to AI-first service (Zendesk AI) poses an existential threat to partners who bill by the hour for manual ticket resolution or basic admin tasks. PE buyers are modeling a future where 40-60% of Tier 1 support volume disappears.

Consequently, due diligence teams are asking: "Is this firm paid to fix tickets, or to eliminate them?" High-value partners have already pivoted their business models to "Outcome-Based Managed Services." Instead of selling hours, they sell "Deflection Rate Optimization" or "CSAT Improvement Programs." They build proprietary IP around intent modeling and automated workflows.

If a partner lacks a dedicated Data & AI practice, they are viewed as a depreciating asset. The expectation is that their traditional services revenue will shrink by 15% annually as native AI features improve. Conversely, partners with proven capabilities in training custom models and integrating Zendesk AI with backend ERPs are trading at SaaS-like revenue multiples, reflecting their strategic scarcity.