The practical answer

- Short answer

- A diagnostic guide for PE firms evaluating Snowflake partner acquisitions. Analysis of consumption metrics, Native App valuation premiums, and the 2026 due diligence framework.

- Best fit

- Industry: Private Equity. Function: M&A Due Diligence

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

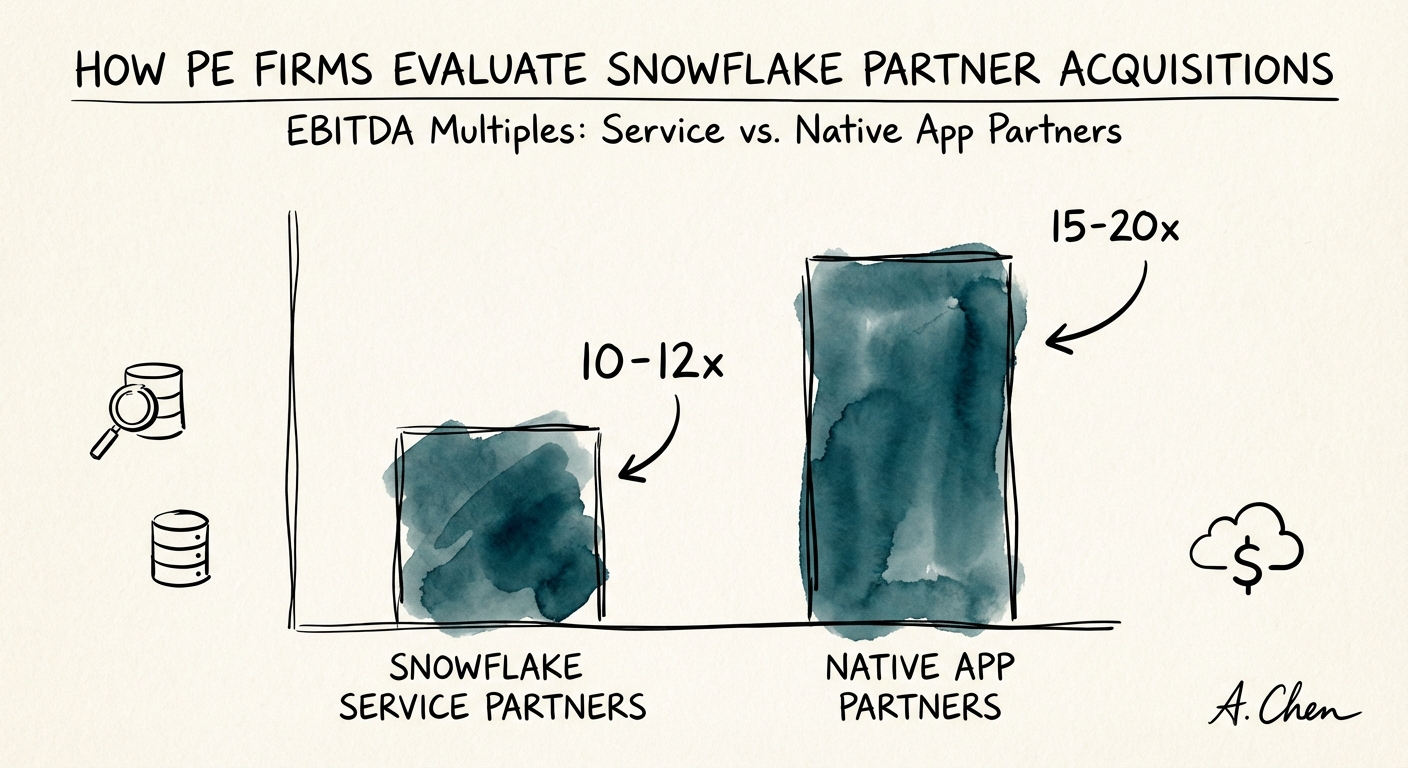

- 6x vs 12x The EBITDA multiple gap between a 'Services' partner and a 'Native App' partner in 2026.

The Consumption Quality of Earnings (QofE)

In 2026, the traditional Quality of Earnings (QofE) report is insufficient for evaluating Snowflake partners. The standard focus on EBITDA adjustments and booked revenue fails to capture the single most important metric in the Data Cloud ecosystem: Consumption.

Unlike traditional SaaS or legacy ERP implementations where "bookings" equal value, Snowflake operates on a consumption model. A partner may book $10M in committed spend (ACV), but if the end client only consumes $2M of credits, that partner has created a "Shelfware Liability."

The "Bookings" Trap

Private Equity firms frequently overvalue partners based on bookings growth (contracted TCV). However, in the Snowflake ecosystem, bookings are merely a leading indicator of potential risk, not realized value. If a partner sells $5M in capacity but their implementation fails to drive the data workloads required to burn those credits, the renewal will collapse. The 2026 due diligence playbook requires a Consumption-to-Booking Ratio (CBR) analysis.

Red Flag: Any partner with a CBR below 0.8 (meaning clients are consuming less than 80% of what they committed) is a churn risk, not a growth asset. Acquiring these firms often leads to a "Renewal Cliff" 12 months post-close.

The New "Recurring" Revenue

True recurring revenue in this ecosystem isn't the managed service contract; it's the Consumption Royalty. Elite partners structure their contracts to share in the consumption upside or wrap "DataOps" managed services around the credit burn. When evaluating a target, strip out one-time implementation fees. Look for Managed Services revenue that correlates with consumption growth. If revenue is flat while client consumption spikes, the partner has failed to capture the value they created.

In the Snowflake ecosystem, bookings are a vanity metric. Consumption is the only truth. If you buy a partner based on committed spend that isn't burning, you are buying a churn event, not an asset.

The Valuation Gap: "Body Shop" vs. "Native App"

The valuation spread in the Snowflake partner ecosystem has bifurcated violently in 2026. On one side are the "Body Shops"—staff augmentation firms trading at 4x-6x EBITDA. On the other are "Data Product" firms leveraging the Snowflake Native App Framework, trading at 8x-12x Revenue.

The Native App Premium

The launch and maturation of the Snowflake Native App Framework changed the math. Partners who build proprietary applications—deployed directly inside the customer's Snowflake instance—are no longer services firms; they are high-margin ISVs. These apps zero out data egress fees and bypass security reviews, creating immense stickiness.

Investors must audit the target's IP portfolio. Does their "accelerator" actually generate license revenue, or is it just marketing slides for a services engagement? A true Native App partner derives >30% of revenue from IP licensing. Anything less is a services firm trying to dress up as a platform.

The "Lift and Shift" Discount

Partners focused on "Lift and Shift" migrations (moving on-prem Teradata/Netezza to Snowflake) are seeing their multiples compress. Automation has commoditized this work. The premium has shifted to Modernization and Domain-Specific Data Estates. A partner moving data is a commodity; a partner building a Healthcare Data Cloud with pre-built regulatory compliance (HIPAA/Hitrust) models commands a scarcity premium.

Financial Benchmarks for Premium Valuation

- Gross Margins: >55% (Blended), >80% (IP Stream)

- Revenue Mix: >40% Managed Services/IP, <60% Professional Services

- Net Revenue Retention (NRR): >120% (driven by consumption expansion)

Vertical Moats: The End of the Generalist

The era of the "Premier Snowflake Partner" badge being a differentiator is over. With thousands of certified partners, the "Generalist Discount" is real. PE firms are actively rolling up niche specialists to form vertical-specific platforms.

The "Industry Cloud" Arbitrage

Snowflake's strategy pivots around Industry Data Clouds (Financial Services, Retail, Healthcare, Media). Partners who align their GTM and IP with these verticals see 30% shorter sales cycles and 2x higher win rates compared to generalists.

Due Diligence Checklist for Vertical Moats:

- Proprietary Data Models: Does the partner own industry-specific data schemas that accelerate time-to-value?

- Snowflake Industry Competency: Have they achieved the specific "Competency" badge for their vertical (e.g., Financial Services Cloud), or are they just generic "Select" partners?

- Client Concentration: A "Healthcare Partner" with 40% of revenue from one hospital system is a concentration risk, not a vertical leader.

The winning PE strategy in 2026 is not buying a "Snowflake Shop." It is buying a "Fintech Data Platform" built on Snowflake. The difference in exit multiple is the difference between selling hours and selling a market position.