The practical answer

- Short answer

- A diagnostic guide for PE firms evaluating Splunk partners. Discover why SecOps specialists trade at 12x while generalists stall at 6x.

- Best fit

- Industry: Private Equity. Function: M&A Due Diligence

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 26% Annual growth rate of Splunk Cloud revenue, a key indicator of a partner's future-proof revenue mix.

The Great Bifurcation: "Log Management" vs. "Security Intelligence"

Following Cisco's $28 billion acquisition of Splunk, the partner ecosystem has bifurcated into two distinct asset classes with radically different valuation profiles. In our analysis of recent deal flow, we see a massive gap between legacy "Log Management" shops and modern "Security Intelligence" platforms.

The Generalist Discount (6x EBITDA): Partners primarily focused on basic log aggregation, compliance reporting, and on-premise Splunk Enterprise maintenance are facing commoditization. These firms often operate on a "body shop" model, billing hourly for SPL (Search Processing Language) query writing. Their revenue is project-heavy, and their customer retention is threatened by lower-cost observability alternatives like Datadog or open-source stacks.

The SecOps Premium (12x+ EBITDA): The premium assets are those entrenched in the Security Operations Center (SOC). These partners don't just "manage logs"; they run Managed Detection and Response (MDR) services on top of Splunk Enterprise Security (ES). They have successfully pivoted to a recurring revenue model where they own the outcome (threat detection), not just the labor. PE buyers are paying 12x-14x for these firms because they bridge the gap between Cisco's network dominance and Splunk's security analytics.

The "Cisco 360" Risk Factor

With the integration of the Splunk Partnerverse into the Cisco 360 Partner Program (launching February 2026), a new due diligence risk has emerged. Partners are now measured by the Partner Value Index (PVI). Legacy Splunk partners who lack Cisco networking certifications may see their margins erode as they lose access to back-end rebates that are now tied to cross-architecture proficiency. In diligence, you must audit the target's readiness for this program merger; a "Splunk Elite" partner today could be demoted to a generic tier tomorrow if they lack the requisite Cisco badging.

In the post-acquisition era, the 'Splunk Elite' badge is just the table stakes. The real valuation driver is the ability to bridge the gap between the Network Operations Center (NOC) and the Security Operations Center (SOC). That is where the 14x multiples live.

Operational Diligence: The "Spaghetti SPL" Trap

In technical due diligence, the single biggest source of value erosion in Splunk consultancies is what we call "Spaghetti SPL." Splunk's flexibility is its Achilles' heel; without rigorous governance, engineers often write complex, undocumented queries that consume excessive compute resources (SVUs/vCPUs) and break whenever the core platform is updated.

When acquiring a Splunk partner, specifically an MSSP, you are buying their intellectual property—their library of detection rules, dashboards, and automation playbooks. If this IP is poorly architected, your post-close R&D costs will balloon as you are forced to refactor the entire service delivery layer.

Key Due Diligence Metrics

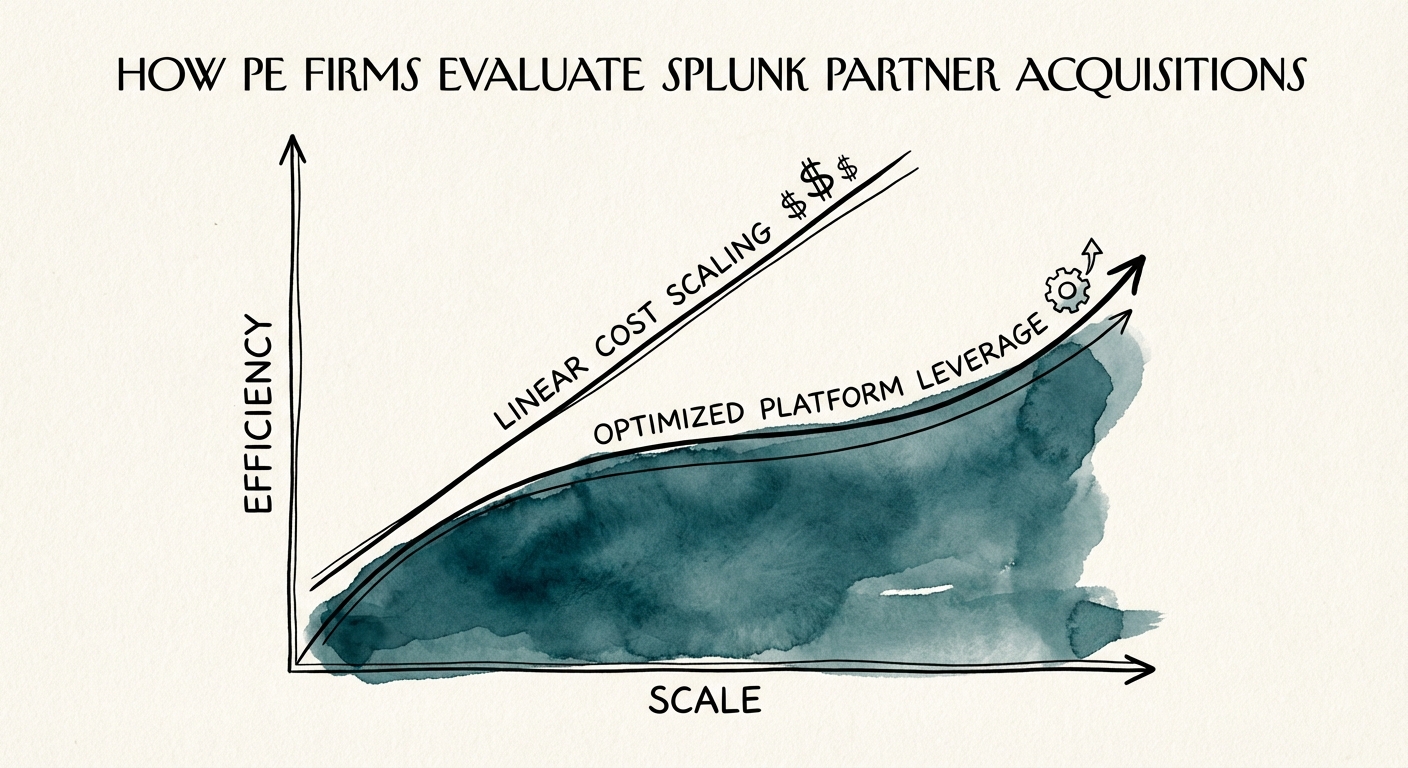

- Compute Efficiency Ratio: analyzing the partner's managed customers. If their "cost of goods sold" (compute/storage) scales linearly with revenue, they haven't built a platform; they've built a resale markup. Top-tier partners demonstrate a 20%+ efficiency gain year-over-year through optimized data ingest pipelines (e.g., using Cribl or Splunk Edge Processor).

- Talent Density & Retention: The cost to replace a Splunk Certified Architect is currently $180k-$220k, with a ramp time of 4-6 months. Analyze the "Key Person Dependency" on the engineering team. If the target's proprietary apps are maintained by a single "hero architect," the deal risk profile increases dramatically.

- Cloud Migration Mix: Partners with >50% of revenue derived from Splunk Cloud migrations or management trade at a premium. Those still heavily reliant on on-premise infrastructure management are acquiring "technical debt revenue" that will churn as customers inevitably move to SaaS.

Valuation Drivers: The Path to 14x

To command the highest multiples in 2026, Splunk partners must demonstrate that they are not just service providers, but strategic enablers of the Cisco Security Cloud. The market is rewarding partners who can execute the "Network + Security" convergence play.

We advise PE sponsors to look for three specific indicators of a platform-grade asset:

- Proprietary IP on Splunkbase: Does the target have certified apps on Splunkbase with significant download numbers? This proves they can build scalable software, not just custom services.

- Vertical Specialization: Generalist partners are struggling. Specialists (e.g., "Splunk for Healthcare" or "Splunk for FedRAMP") are seeing 30% higher retention rates and lower CAC, justifying a higher multiple.

- Managed Services Composition: A target with >45% recurring managed services revenue (vs. project revenue) and <20% customer concentration is the sweet spot. If the "Managed Services" are actually just retainer-based block hours, discount the multiple by 2 turns.

Ultimately, the winners in this ecosystem will be the partners who can translate raw data into business resilience. As you evaluate targets, look past the certifications and look at the workflow. Are they selling hours, or are they selling security outcomes?