The practical answer

- Short answer

- A diagnostic guide for PE Operating Partners on valuing AWS partners. Covers the $7.13 services multiplier, Marketplace premiums, and the specific QofE traps in 2026.

- Best fit

- Industry: Private Equity / Technology Services. Function: M&A Due Diligence

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x EBITDA multiple for AWS Partners with >30% Marketplace transaction volume vs. 6x for traditional SIs.

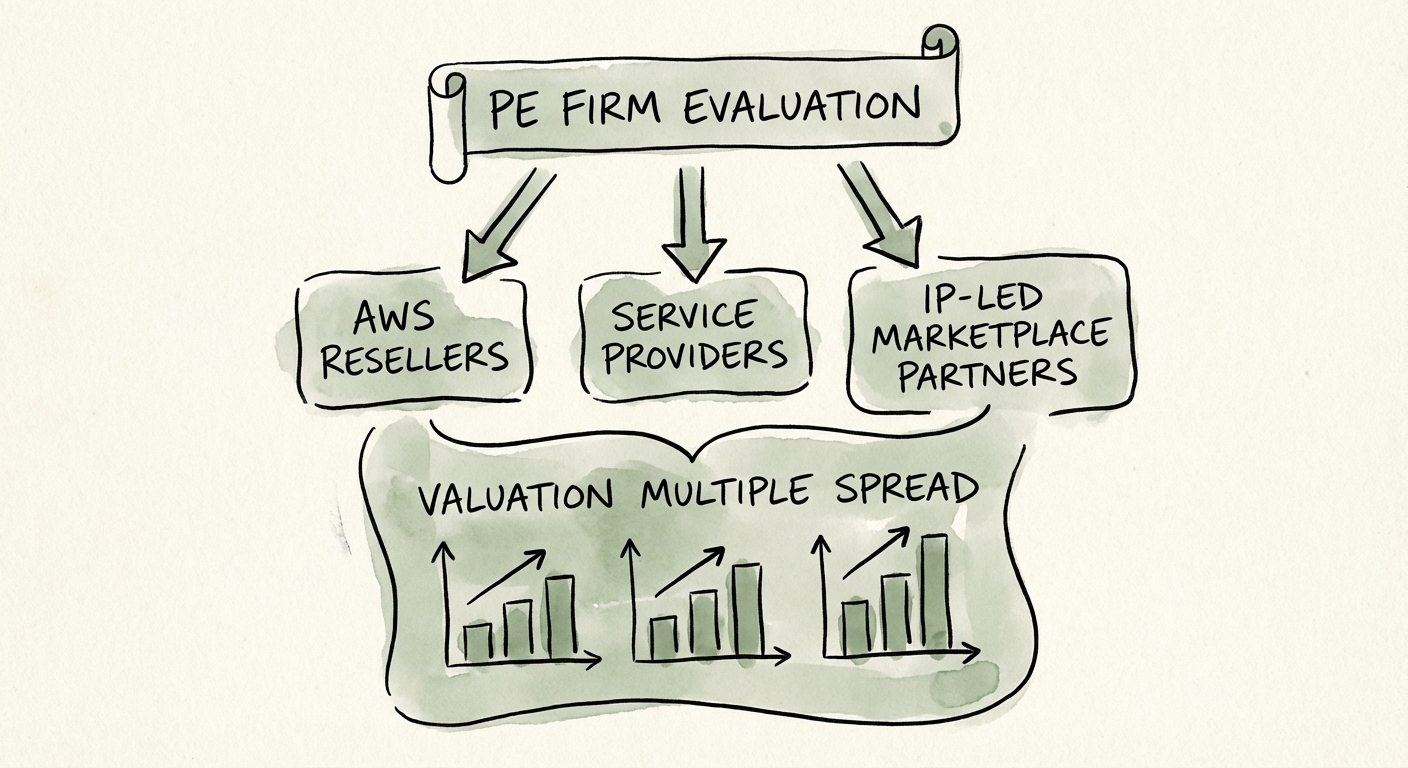

The Valuation Bifurcation: Why 'AWS Partner' Is No Longer an Asset Class

In 2026, the label "AWS Partner" is meaningless in isolation. The market has bifurcated into three distinct asset classes, and PE firms applying a generic "IT Services" multiple (typically 8-10x) are either overpaying for low-margin resell revenue or undervaluing high-leverage IP assets.

1. The Resell & Rebate Trap (3x - 5x EBITDA)

Partners relying on AWS resell margin (the spread between wholesale and retail AWS pricing) and backend rebates/credits are trading at commodity multiples. In 2026, with AWS aggressively pushing direct enterprise agreements and the AWS Marketplace commoditizing procurement, the margin on pure resell has compressed to <8%. If your target's EBITDA relies on "pass-through" revenue to hit the Rule of 40, you are buying a melting ice cube.

2. The 'Body Shop' Service Provider (6x - 9x EBITDA)

These firms sell hours. They may have "Premier" status, but their revenue scales linearly with headcount. They suffer from the classic 68.9% utilization ceiling. While stable, they lack the operating leverage to command premium multiples unless they have deep vertical specialization (e.g., Healthcare Life Sciences, Financial Services) that creates a defensive moat against generalist offshore firms.

3. The IP-Led & Marketplace Native (12x - 16x+ EBITDA)

These are the targets commanding premiums. They don't just bill hours; they deploy proprietary "accelerators" (code libraries, automated migration tools, compliance frameworks) that decouple revenue from headcount. Crucially, they transact heavily on the AWS Marketplace. Data from 2025 shows that partners with >30% of revenue flowing through Marketplace trade at a premium because of significantly lower CAC (procurement cycles shortened by 60%) and higher retention. They aren't selling people; they are selling outcomes.

Stop buying 'Premier' badges. Start buying IP and Marketplace efficiency. A Premier partner with 10% gross margins and linear headcount scaling is not a platform—it's a liability waiting for a wage-inflation shock.

The Revenue Quality (QofE) Landmines in 2026

Standard Quality of Earnings reports often miss the specific liabilities buried in AWS partner financials. Operating Partners must demand a "Cloud Economics" layer in their due diligence.

The EDP Liability Trap

Aggressive partners often sign Enterprise Discount Program (EDP) commitments on behalf of customers to secure better tiering or rebates. If the end-customer churns or fails to consume that committed compute, the partner may be on the hook for the shortfall. I recently saw a $50M acquisition target with a hidden $4M "under-consumption" liability sitting off-balance-sheet. You must audit every EDP contract for recourse clauses.

The 'Pass-Through' Revenue Mirage

Is the target recognizing AWS consumption as Gross Revenue? Under ASC 606, most resell revenue should be recognized Net. Partners who recognize Gross Revenue to inflate their top-line growth (showing 40% YoY growth when Net Revenue is flat) are selling you a hallucination. Recalculate all valuation multiples based on Net Revenue (Gross Profit) to see the real picture.

The 'AI Practice' Vaporware

Every CIM in 2026 claims a "Generative AI Practice." In 90% of cases, this is a technical debt red flag. Diligence must distinguish between:

- POC Revenue: One-off, non-recurring experiments with high churn.

- Production Revenue: Workloads running on Bedrock/SageMaker with consumption scaling.

If the "AI Revenue" is 80% Professional Services for "Strategy Workshops" and 0% Consumption, there is no stickiness. Real AI practices drive compute consumption.

Operational Benchmarks: The 'Paper Tiger' Diagnostic

Do not be seduced by the "Premier Tier" badge. It can be bought with low-margin resell volume and a 'certification farm' hiring strategy.

The Certification vs. Capability Gap

A firm with 500 AWS Certifications but no Competencies is a red flag. Certifications are individual achievements; Competencies (e.g., Migration, DevOps, Data & Analytics) are organizational validations audited by AWS. A target with the Migration Competency or SaaS Competency has undergone a technical audit of their delivery methodology. A target with just "500 Certified Engineers" is likely a staffing agency in disguise.

The Services Multiplier Benchmark

The definitive efficiency metric for 2026 is the Partner Ecosystem Multiplier. According to Canalys and AWS data, high-performing partners generate $7.13 in services/software revenue for every $1 of AWS compute they influence.

If your target is generating only $2.00 in services for every $1 of AWS, they are simply "racking and stacking" infrastructure without capturing the higher-margin application modernization or data strategy work. They are the 'plumbers' of the cloud, while the 'architects' take the margin. Use the $7.13 benchmark to aggressively challenge their revenue mix during management meetings.