The practical answer

- Short answer

- A private equity operating partner's guide to valuing Microsoft Azure partners. Learn the impact of ACR, Advanced Specializations, and managed services mix on exit multiples.

- Best fit

- Industry: Private Equity / Technology Services. Function: M&A / Corporate Development

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 13.6x Average EBITDA multiple for Azure Partners with 'Data & AI' Advanced Specializations in 2025.

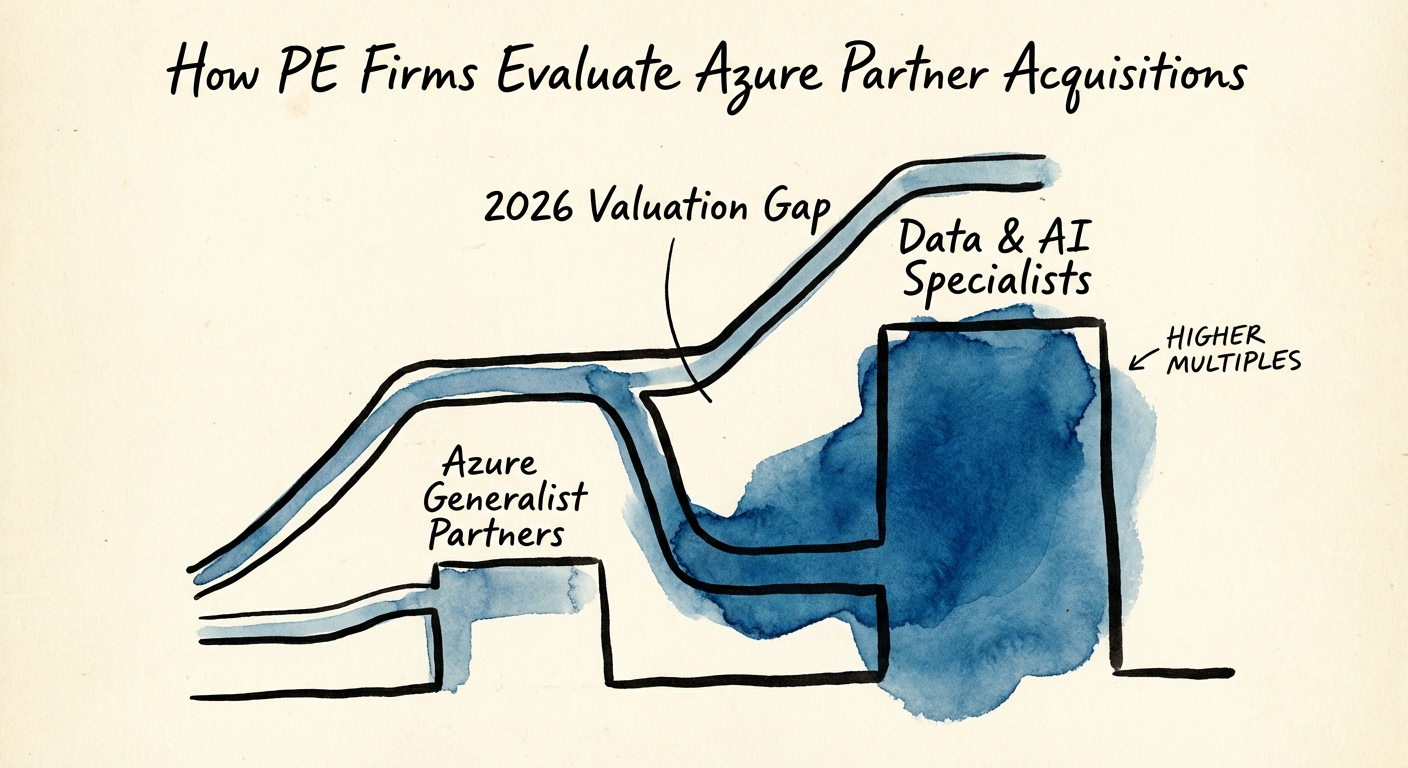

The "Gold Partner" Fallacy is Dead

If you are looking at a CIM (Confidential Information Memorandum) that highlights "Gold Partner" status in 2026, you are looking at a distressed asset. Microsoft killed the Gold/Silver badges years ago, replacing them with the Microsoft AI Cloud Partner Program (MAICPP) designations. Yet, I still see founders—and surprisingly, some brokers—leading with legacy accolades that imply competence but guarantee nothing.

For Private Equity buyers, the valuation game has shifted from capacity (how many certified heads do you have?) to consumption (how much Azure revenue do you actually drive?). The market has bifurcated. On one side, you have the "License Flippers"—low-margin resellers trading at 4x-6x EBITDA. On the other, you have the "Consumption Architects"—firms embedding IP and Managed Services into the Azure fabric—commanding 12x-15x EBITDA.

The difference isn't in the revenue topline. It's in the Quality of Revenue. A $50M revenue shop with $45M in low-margin licensing resale is effectively a $5M business with a massive liability. Conversely, a $15M shop with $10M in high-margin, recurring Managed Azure services is a platform target. In 2026, if you can't distinguish between Partner Admin Link (PAL) attribution and simple resale, you're about to overpay.

In 2026, the market doesn't care about your 'Gold' badge. It cares about your Data Gravity. If you aren't managing the data estate, you're just a glorified landlord collecting rent on someone else's building.

The New Scorecard: ACR is the North Star

Forget bookings. In the Azure ecosystem, Azure Consumed Revenue (ACR) is the only truth. Microsoft incentives, support tiers, and ultimately, your exit multiple, are tied to this metric. But for a PE investor, raw ACR isn't enough. You need to look for ACR Influence.

1. The "PAL" Litmus Test

During diligence, ask for the Partner Admin Link (PAL) report. This tells you which Azure workloads the partner actually manages. If a partner claims to "own" a customer but shows zero PAL attribution, they are merely a paper vendor. They have no operational hook into the client's infrastructure, meaning their revenue is highly churn-prone.

2. The Specialization Premium

Generalist "Infrastructure" partners are a dime a dozen. The alpha is in Advanced Specializations. In our 2025-2026 benchmarks, partners with "Analytics on Microsoft Azure" or "AI Platform" specializations traded at a 35% premium compared to infrastructure-only peers. Why? Because migration is a one-time project; data estate management is a forever revenue stream.

3. The "Pass-Through" Trap

Be wary of "Cloud Resale" appearing as recurring revenue. In your Quality of Earnings (QofE), strip out the low-margin license revenue to see the naked EBITDA of the services business. I've seen "$20M ARR" companies that were actually $18M of 3% margin resale and $2M of actual services. That's not a SaaS multiple; that's a grocery store margin.

Valuation Matrix: What Are You Actually Buying?

When we advise PE sponsors on roll-ups, we categorize Azure targets into three buckets. Your post-close value creation plan depends entirely on which bucket you've acquired.

Bucket A: The Reseller (Valuation: 0.5x - 0.8x Revenue)

High revenue, low gross margin (10-15%). Their value is customer access, not technology.

The Play: Acquire for the customer list, then deploy a "Hunt and Harvest" strategy to cross-sell high-margin managed services (Security, Data/AI).

Bucket B: The Project Shop (Valuation: 6x - 8x EBITDA)

High gross margin (40-50%), but lumpy revenue. They live and die by the utilization rate.

The Play: Force a transition to Managed Services. Convert "Project Revenue" into "subscribe-to-outcome" models. If they haven't made this pivot by $10M revenue, they likely never will without external pressure.

Bucket C: The Platform Specialist (Valuation: 12x - 15x EBITDA)

The Holy Grail. High managed services mix (>40%), high retention (NDR > 110%), and deep vertical IP (e.g., "Azure Data Lake for Healthcare").

The Play: This is your platform. Pour gas on Sales & Marketing. The constraints here are usually talent acquisition and GTM scaling, not product/market fit.

The Bottom Line: In 2026, you aren't buying "IT Services." You are buying Data Gravity. The partners who have successfully moved from "lifting and shifting" VMs to "modernizing data estates" are the ones who will survive the AI consolidation wave.