The practical answer

- Short answer

- Healthcare and Life Sciences Snowflake partners can defend a premium when they prove interoperability, compliance, repeatable IP, and vertical delivery depth.

- Best fit

- Industry: Healthcare IT & Data Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- HCLS Healthcare and Life Sciences specialization should show up in revenue, delivery, hiring, and playbooks.

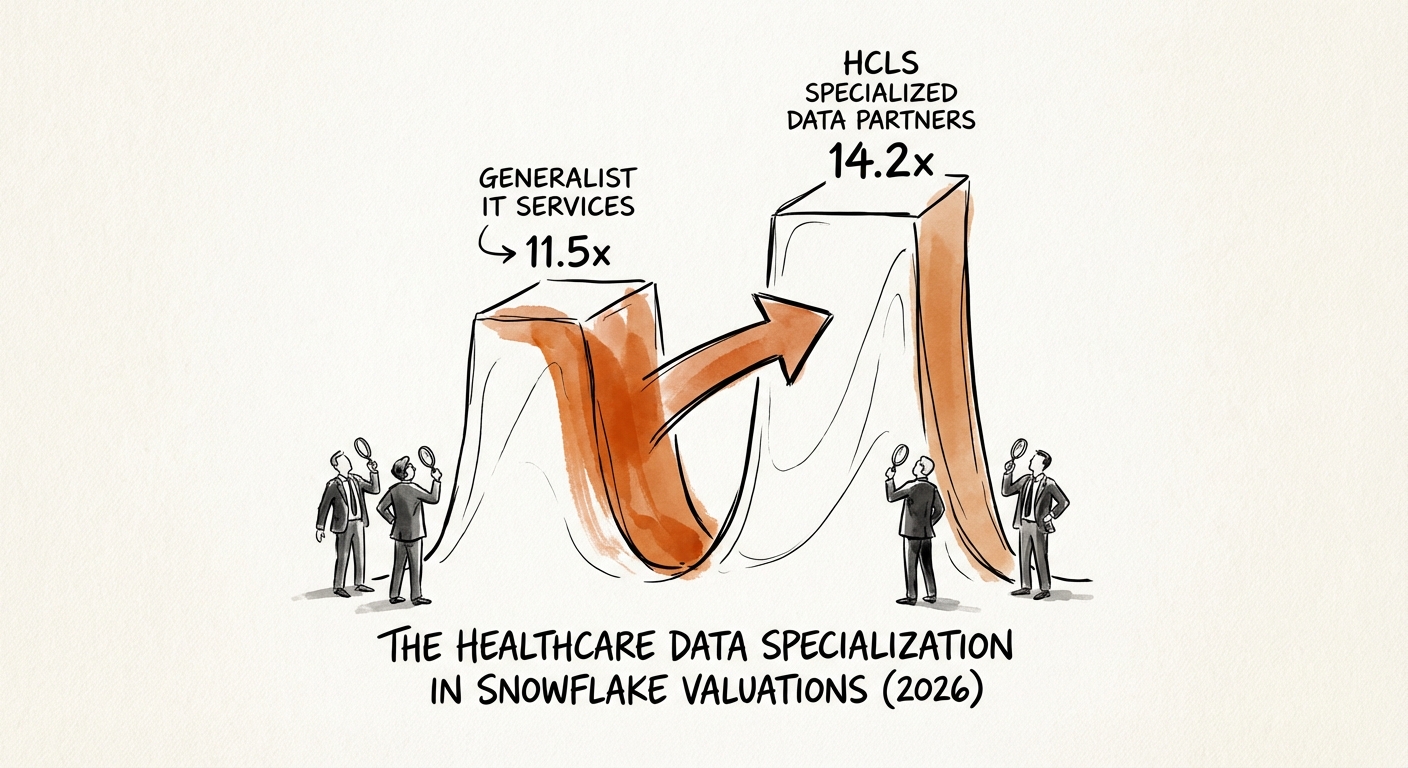

The Generalist Discount vs. the Vertical Premium

The market for Snowflake services partners has bifurcated. Generalist firms that primarily move data warehouses into the Data Cloud are easier to compare on capacity, rate card, and certification count. Healthcare and Life Sciences partners with deep workflow, compliance, and interoperability expertise can tell a more defensible story.

The difference is not just industry logos. Migrating a pharmaceutical company's clinical trial data involves GxP considerations, HIPAA-sensitive workflows, FHIR and HL7 interoperability, consent, security, and auditability. Buyers pay more attention to partners that have already solved those high-friction problems with repeatable accelerators.

In healthcare data, compliance is table stakes. The premium comes from turning regulatory complexity into repeatable delivery IP.

The Clinical Data Multiplier: Beyond Ingestion

The premium for healthcare data partners is driven by the complexity of use cases enabled, not the volume of data stored. The most valuable partners move beyond simple analytics into clinical data repositories, patient 360 views, quality reporting, interoperability, and governed AI workflows.

The 3 Pillars of HCLS Valuation

- Interoperability acceleration: Repeatable patterns for ingesting and normalizing HL7 and FHIR data streams.

- Regulatory governance as code: Automated row-level security, masking, access review, and auditability mapped to healthcare requirements.

- High-value use cases: Work tied to clinical operations, value-based care analytics, trial acceleration, or supply-chain reliability carries a stronger story than generic reporting.

The HCLS Diagnostic: Specialist or Generalist?

Many partners claim healthcare specialization because they have a hospital logo on the slide deck. In diligence, buyers look for evidence that healthcare is embedded in delivery, hiring, playbooks, and revenue mix.

1. Revenue Concentration

Healthcare and Life Sciences should be a meaningful share of revenue, not an opportunistic vertical.

2. Accelerator Ratio

Buyers want to see proprietary assets: clinical data models, integration templates, governance policies, and implementation accelerators that shorten time-to-value.

3. Certification and Domain Mix

A Snowflake architect who understands claims, clinical encounters, and interoperability standards is more valuable in this sector than a generalist cloud engineer. The path to a stronger exit involves focus, documentation, and repeatable healthcare-specific IP.