The practical answer

- Short answer

- Why UiPath partners with Process Mining capabilities trade at 14x EBITDA while pure RPA shops stall at 6x. A diagnostic for founders and their PE backers.

- Best fit

- Industry: Intelligent Automation / RPA. Function: M&A & Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

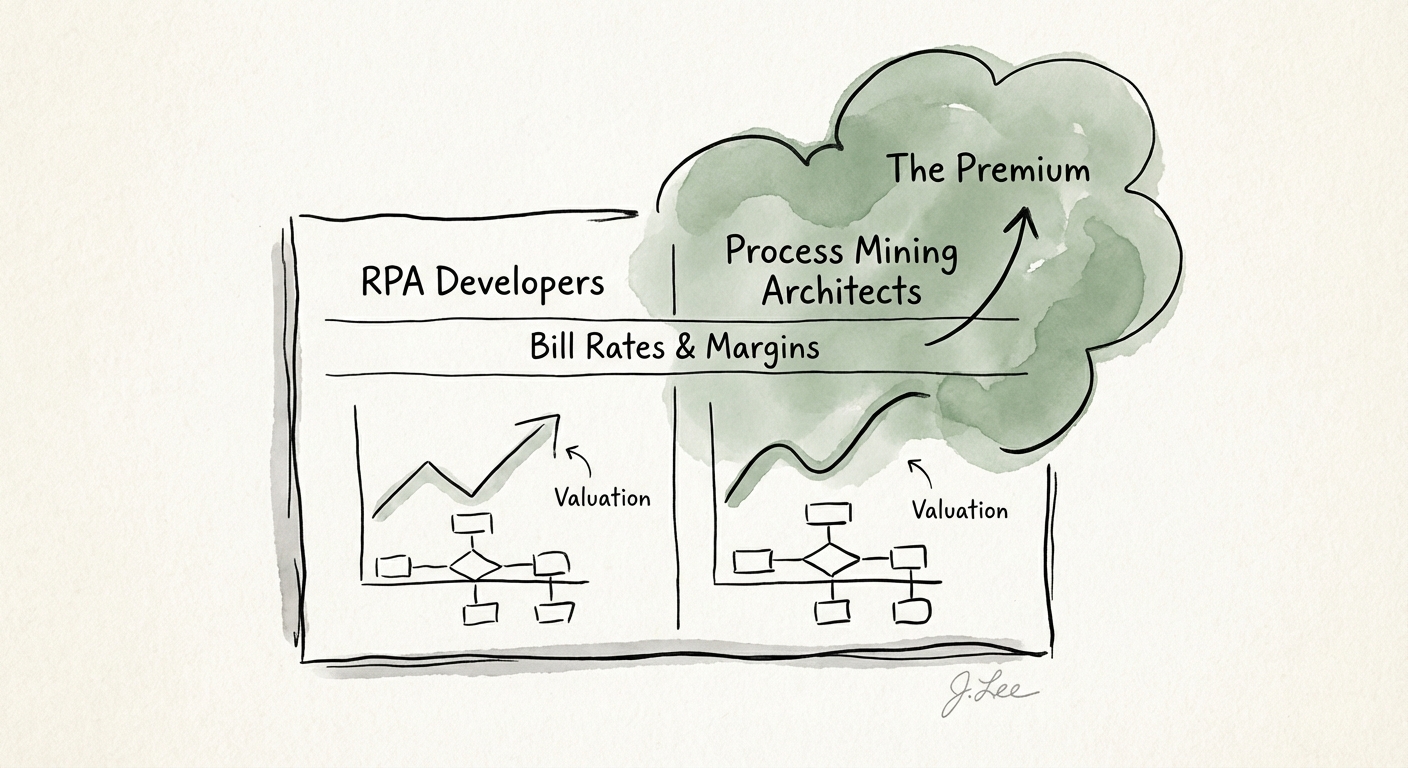

- 133% Higher bill rate for Process Mining Architects vs. RPA Developers.

The 'Bot Shop' Discount vs. The Intelligence Premium

In the early days of the RPA gold rush (circa 2018-2020), private equity firms were buying anything that could spell "UiPath." If you had a bench of certified developers and a few logos, you could command a double-digit multiple. Those days are over. The market has bifurcated into two distinct asset classes: the "Bot Shops" and the "Process Intelligence" firms.

The "Bot Shop" model—pure-play RPA implementation—is now facing severe commoditization. Rate cards for basic RPA developers have compressed by 30% since 2022 as offshore centers flood the market. More critically, these firms suffer from the "fragility problem": bots break when underlying applications change, leading to high maintenance costs and frustrated clients. In the eyes of an acquirer, this looks like low-margin technical debt, trading at 6x-8x EBITDA.

Contrast this with the "Process Intelligence" partner. These firms use Process Mining (UiPath Process Mining, Celonis, etc.) not just as a tool, but as their primary engagement model. They don't start by asking "what do you want to automate?" They start by connecting to ERP event logs to mathematically prove where value is leaking. This "MRI before surgery" approach shifts the vendor relationship from a tactical IT vendor to a strategic C-Suite advisor. Consequently, these firms are seeing valuations of 12x-14x EBITDA.

Why The Valuation Gap Exists

- Entry Point Authority: Bot Shops enter through the IT Director. Process Mining partners enter through the CFO or COO, controlling the strategic roadmap.

- Revenue Quality: Process Mining engagements often trigger a 5x multiplier in downstream implementation revenue, but with higher-margin architectural oversight rather than commodity coding.

- Stickiness: Once a client installs continuous process monitoring, ripping out the partner becomes operationally risky, creating "quasi-SaaS" retention metrics.

Process Mining is not just a tool; it is the difference between a vendor who takes automation orders and an advisor who proves where operational value is leaking. In valuation markets, that diagnostic authority commands a premium.

The Economics of 'Discovery-Led' Growth

The financial profile of a Process Mining-led partner looks fundamentally different in the Data Room. The most obvious difference is in the Bill Rate Differential. While a Senior RPA Developer might bill at $125-$150/hour, a Process Mining Architect—who combines data science, SQL proficiency, and business process re-engineering—commands $250-$350/hour. This isn't just a margin play; it's a talent moat. It is exponentially harder to replicate a team of data-savvy process architects than a bench of script writers.

Furthermore, Process Mining solves the "Pipeline Problem" that kills so many RPA exits. Pure RPA shops often hit a wall after automating the "low-hanging fruit" (invoice processing, password resets). Growth stalls, and so does the multiple. Process Mining provides a scientific, continuous pipeline of automation opportunities, objectively ranked by ROI. Acquirers pay a premium for this visibility.

The 'Pull-Through' Multiplier

Our research into recent M&A transactions in the automation space suggests a clear correlation between discovery capabilities and deal size:

- Traditional RPA Deal: $1 of Assessment leads to $2-$3 of Implementation.

- Process Mining Deal: $1 of Process Mining leads to $5-$7 of Intelligent Automation, Infrastructure, and Change Management.

By controlling the diagnosis, the partner controls the treatment plan. This effectively locks out competitors and increases the Lifetime Value (LTV) of the customer, a metric that PE sponsors scrutinize heavily during due diligence.

Strategic Pivot: Moving Upstream Before the Exit

For UiPath partners looking to exit in the next 18-24 months, the message is clear: You cannot simply be a pair of hands. You must own the diagnostic agenda. Pivoting to a Process Mining-led model is the most effective way to expand EBITDA margins and justify a premium multiple.

The 'Process Center of Excellence' (CoE) Mandate

To capture this premium, partners must build a dedicated Process CoE. This is not just buying a Celonis or UiPath Process Mining license. It requires:

- Data Engineering DNA: Hiring talent that understands ETL (Extract, Transform, Load) and event log structures (SAP, Oracle, Salesforce), not just UiPath Studio.

- Consultative Sales Motion: Training sales teams to sell "transparency" and "efficiency," not just "bots." The buyer is business, not IT.

- Continuous Monitoring Offers: shifting from one-off "projects" to annual subscriptions for process health monitoring, smoothing out lumpy professional services revenue.

Investors are paying for the certainty of future cash flows. A partner that can mathematically prove the next 12 months of automation backlog via process data is infinitely more valuable than one relying on the intuition of department heads. As noted in broader ecosystem risk analyses, diversification through intellectual property and strategic advisory is the only hedge against vendor commoditization.