The practical answer

- Short answer

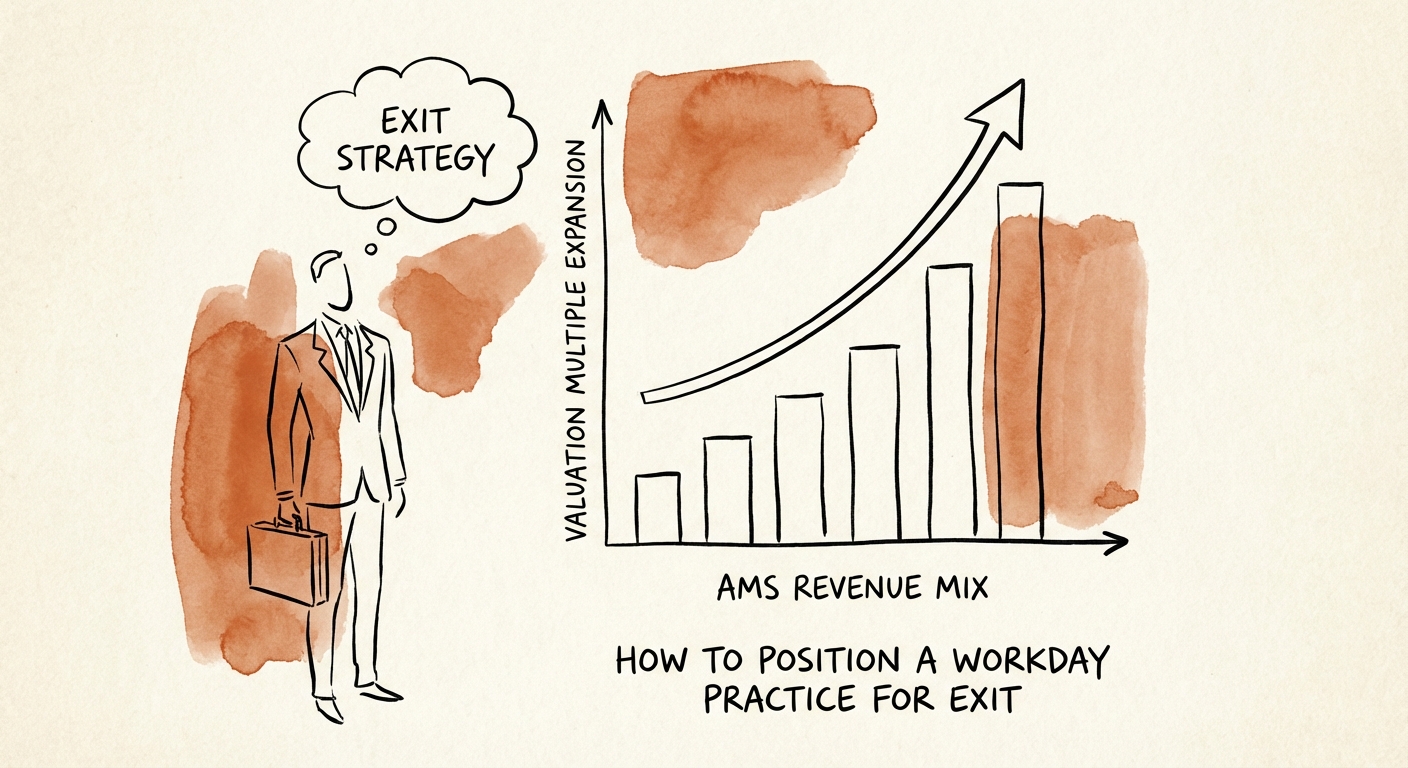

- Workday partners trade at a 40% premium, but only if they escape the 'body shop' trap. Here is the diagnostic guide for positioning your firm for a strategic exit.

- Best fit

- Industry: IT Services. Function: M&A Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 14x Potential EBITDA multiple for specialized Workday Financials practices

The 'Velvet Rope' Economy: Why Workday Partners Are Different

In the world of IT services M&A, not all revenue is created equal. A dollar of revenue in the Salesforce ecosystem—where there are thousands of partners fighting for scraps—is worth fundamentally less than a dollar of revenue in the Workday ecosystem. We call this the "Velvet Rope" premium.

Workday strictly controls its partner ecosystem. You cannot just "spin up" a Workday practice overnight; you have to be invited. This scarcity creates a defensive moat that private equity buyers are willing to pay a premium for. While generalist IT services firms struggle to command 6x-8x EBITDA multiples, specialized Workday partners often see offers in the 10x-14x range. But there is a catch.

That premium is not guaranteed. We see founders assuming that simply having the Workday badge entitles them to a double-digit multiple. It doesn't. In 2025, buyers have become disciplined about bifurcating the market into two buckets: the "Strategic Partners" who own the office of the CFO/CHRO, and the "Body Shops" who are just renting out certified hands. If you are in the latter category, your exit valuation will be cut in half, regardless of the logo on your website.

A Workday badge gets you in the room. It does not guarantee you a seat at the table. The difference between a 6x and a 12x exit is whether you are selling 'hours' or 'outcomes'.

The Valuation Diagnostic: Are You a Partner or a Body Shop?

To position your firm for a premium exit, you must rigorously audit your revenue quality. Private equity investors are looking for three specific signals that separate high-value targets from commodity staffing firms.

1. The AMS Multiplier (Recurring vs. Project)

The biggest valuation killer we see is a 90/10 revenue split favoring implementation. If your business model relies entirely on "Go-Lives," you are on a hamster wheel. You start every year at zero. Buyers pay for predictability. The most valuable Workday practices have aggressively pivoted to Application Management Services (AMS). This isn't just help-desk support; it's "Phase X" continuous optimization. A firm with 40% of revenue coming from multi-year AMS contracts will trade at a significantly higher multiple than a firm with 10% AMS, even if the latter has higher top-line growth.

2. Specialization Beyond HCM

Human Capital Management (HCM) is table stakes. It’s a crowded hallway. The real valuation drivers in 2026 are Financials (FINS), Adaptive Planning, and specialized modules like Prism or Student. If your team is 90% HCM generalists, you are competing on rate. If you have a deep bench of FINS architects who can speak accounting to a CFO, you have pricing power and scarcity value. Buyers know that an HCM consultant takes 6 months to replace, but a FINS architect takes 18 months. That "replacement cost" is a key component of your enterprise value.

3. The "Product Lead" Metric

Stop counting "certifications." Buyers know that a "Pro" certification can be earned relatively quickly. In due diligence, we look for "Product Leads"—the senior architects who are authorized to lead deployments. A firm with 100 certified consultants but only 5 Product Leads is a staffing agency. A firm with 50 consultants and 15 Product Leads is a consulting firm. The ratio matters.

Founder Extraction: The Final Gate

For founders, this is the hardest pill to swallow. You cannot sell a firm where you are the Chief Revenue Officer, the Lead Architect, and the escalation point for every major account. In the Workday ecosystem, where relationships with Workday Channel Managers are currency, founder dependency is particularly high-risk.

If Workday sales reps only trust you, you don't have a sales channel; you have a Rolodex. To exit, you must transfer that trust to a sales leader or a practice director. We advise clients to institute a "No-Fly Zone" for the founder 12 months before a sale. If you are still flying to on-site orals to close the deal, you aren't ready to sell. The buyer needs to see that the "machine" works without your heroics.

The goal is to present a clean, transferable asset: a firm with 30%+ recurring revenue, deep specialization in high-demand modules, and a sales engine that doesn't require the founder's charisma to close deals. That is how you turn a services firm into a strategic platform.