The practical answer

- Short answer

- Generalist SAP partners face rate compression. Discover why specializing in Industry Cloud on BTP drives 2x win rates and premium exit valuations.

- Best fit

- Industry: Enterprise Software / IT Services. Function: Go-to-Market / Strategy

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 8x Lower Customer Acquisition Cost (CAC) for Vertical vs. Horizontal Partners

The 'Rate Card' Race to the Bottom

If you run an SAP consultancy generating between $10M and $50M in revenue, you are likely feeling the walls close in. The 'lift and shift' migration work to S/4HANA, once promised as the gold rush of the decade, has become a commoditized battlefield. Global System Integrators (GSIs) are bidding these projects at margins you cannot sustain, effectively turning the migration business into a staffing game.

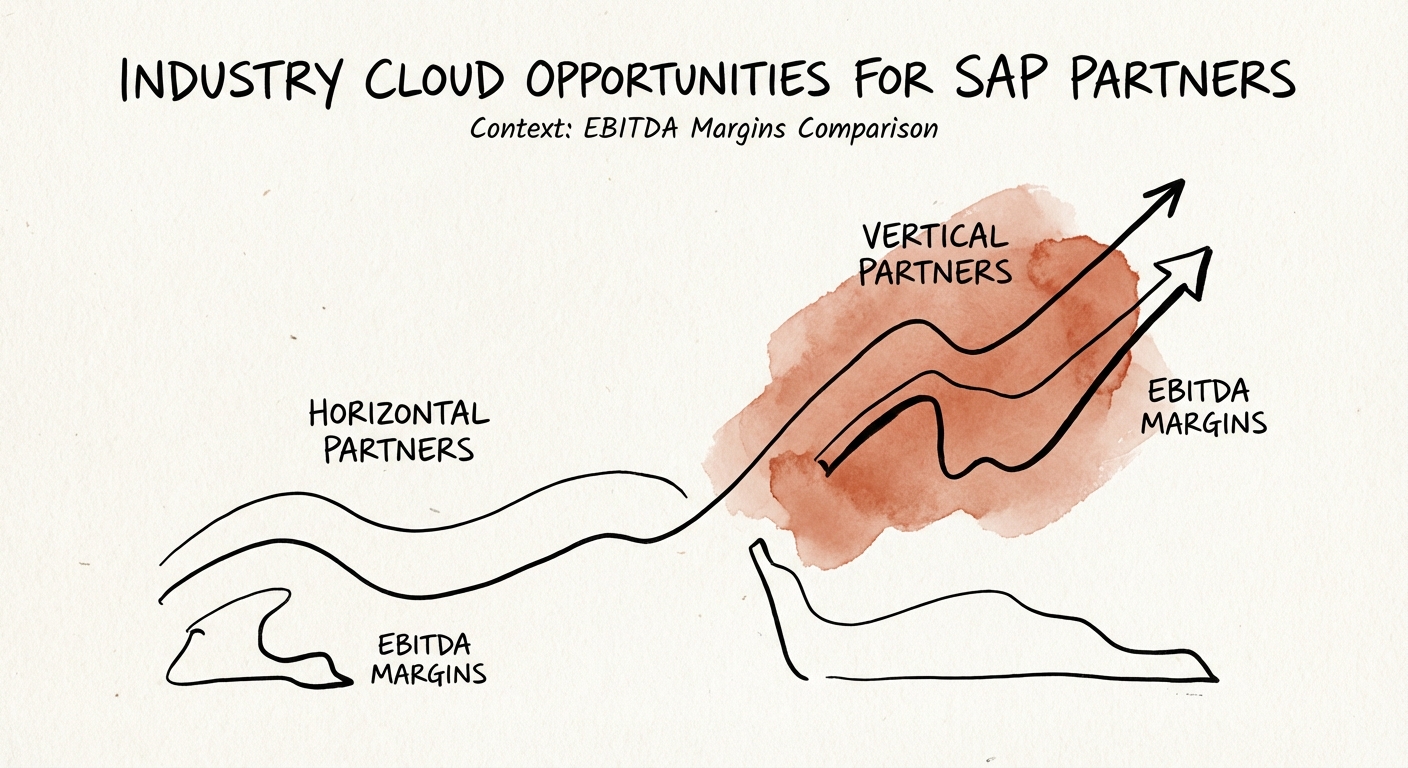

The data is brutal. While SAP’s cloud backlog grew 28% in 2025, the partners winning the high-margin work weren’t the ones selling generic 'implementation capacity.' They were the ones selling Industry Cloud IP. Generalist firms are trading at 5x-7x EBITDA, functionally valued as staffing agencies. Specialized partners—those leveraging the Business Technology Platform (BTP) to own a vertical niche like 'Life Sciences Clinical Trials' or 'Retail Inventory Orchestration'—are seeing valuations north of 12x.

Why? Because private equity buyers don’t buy hours. They buy retention and recurring revenue. Vertical specialization reduces Customer Acquisition Cost (CAC) by up to 8x compared to horizontal plays. If your GTM strategy is still 'We implement S/4HANA,' you have already lost the valuation war.

Private Equity doesn't buy 'general purpose' capacity anymore. They buy specific answers to expensive problems. If you're the 'SAP for Chemicals' expert, you name your price. If you're just an 'SAP Partner,' you take the market rate.

The Vertical Multiplier: BTP as Your Moat

The 'Clean Core' strategy isn’t just technical guidance from Walldorf; it is a business model mandate. By keeping the S/4HANA core clean and pushing customizations to the SAP Business Technology Platform (BTP), you aren’t just writing code—you are building an asset. This is where the Industry Cloud opportunity fundamentally changes your P&L.

According to recent ecosystem data, partners who lead with Industry Cloud solutions close 50% to 150% more deals in their first year compared to those selling generic ERP extensions. More importantly, these deals are sticky. Vertical-specific IP drives Net Revenue Retention (NRR) to 110-120%, whereas horizontal services struggle to break 105%. This is the difference between a 'vendor' and a 'partner.'

Consider the margin impact. Specialized vertical software players operate at a median 15% EBITDA margin, nearly triple the 6% median of horizontal generalists. When you productize your domain expertise on BTP, you decouple revenue from headcount. You stop selling time and start selling capability. In a market where 27% of companies have completed their S/4HANA migration, the remaining 73% aren’t looking for more bodies; they are looking for specific, industry-proven outcomes that de-risk their transformation.

Execution: From 'Body Shop' to 'Boutique Powerhouse'

Pivoting to an Industry Cloud model requires a disciplined audit of your current revenue mix. You cannot be 'SAP for Everyone' anymore. You must identify the one vertical where your delivery teams have tribal knowledge that exceeds the documentation.

1. Productize the 'Last Mile'

Identify the 20% of customization requests you receive repeatedly in your target vertical. Build that functionality as a standard application on BTP. If you serve Pharma, build the connector for FDA compliance reporting. If you serve Manufacturing, build the shop-floor IoT integration. This IP becomes your wedge in the door.

2. Align with the SAP Store

Get your solution listed and certified. This isn't just about distribution; it's about validation. When an SAP Account Executive sees your solution on the store, you become a co-sell partner rather than a competitive threat. Deal sizes for partners with Industry Cloud solutions are 3% to 46% larger because they pull through additional licenses.

3. Rewrite the Valuation Story

When you speak to potential acquirers, stop talking about 'billable utilization' and start talking about 'IP attachment rates.' Show them that 40% of your services revenue is attached to proprietary BTP solutions. That metric alone can move your multiple from a 6x to a 10x. You are no longer a service provider; you are a platform-enabled specialist.