The practical answer

- Short answer

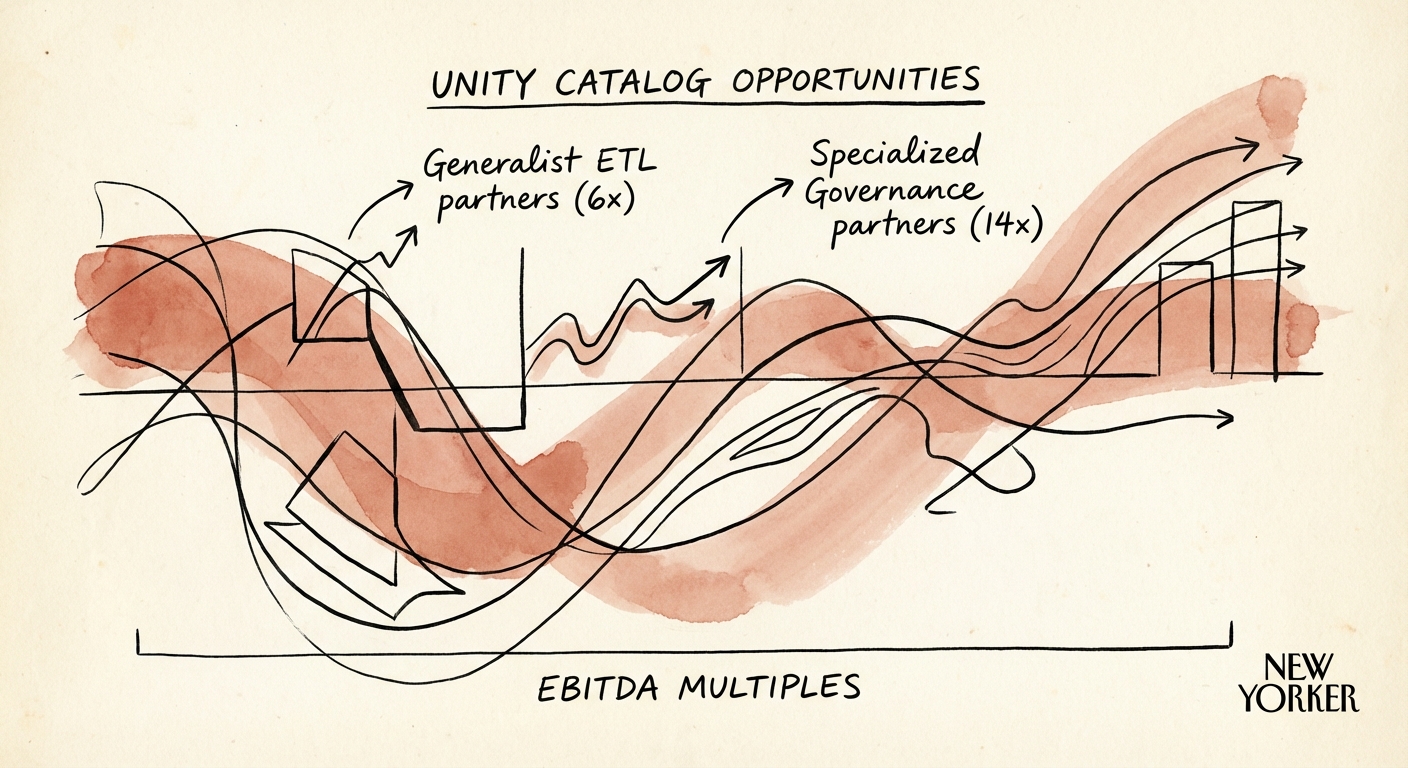

- Why Databricks partners specializing in Unity Catalog migration and governance command 14x multiples. A diagnostic for shifting from ETL body shops to AI strategy firms.

- Best fit

- Industry: Technology Services. Function: Alliances & Partnerships

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 14x EBITDA multiple for Databricks partners with specialized 'AI Governance' practices.

The "Hive" Cliff: Why Generalist ETL Shops Are Dying

In January 2026, the Databricks ecosystem looks nothing like it did in 2023. With the Series L valuation hitting $134 billion, Databricks has solidified its position not just as a data warehouse, but as the operating system for Enterprise AI. Yet, a dangerous bifurcation has emerged in the partner channel.

On one side are the "Body Shop" Generalists. These firms are still selling "lift and shift" migrations, moving Spark jobs from on-prem Hadoop to the cloud, often relying on the legacy Hive Metastore (HMS). Their revenue is tied to headcount, and their valuation is anchored to low-margin staffing models, typically trading at 4x-6x EBITDA. They view Unity Catalog as a technical upgrade—a "nice to have" that they implement only when forced.

On the other side are the Governance Specialists. These firms understood early that Unity Catalog wasn't just a permissions layer; it was the control plane for the entire AI lifecycle. By deprecating HMS strategies and leading with Unity Catalog, they unlock the ability to govern Volumes (unstructured data), Models, and Agents. Because they solve the #1 blocker to AI adoption—governance—they are commanding 12x-14x EBITDA multiples.

The market reality is harsh: If your practice is still maintaining Hive Metastore architectures, you aren't building an asset; you're servicing technical debt. Technical debt remediation is a low-margin game. The premium lies in enablement.

In 2026, AI governance isn't a compliance box to check—it's the product. Partners who treat Unity Catalog as the foundation of an 'AI Operating System' are seeing valuation multiples double those of traditional data engineering firms.

The "Volumes" Multiplier: Governing the Unstructured 90%

The defining shift of 2025 was the explosion of unstructured data usage in RAG (Retrieval-Augmented Generation) workflows. According to IDC, over 90% of enterprise data is unstructured, yet traditional partners only know how to govern the structured 10% (SQL tables).

This is where the Unity Catalog Premium materializes. Specialized partners are packaging "AI Readiness" not as a data engineering task, but as a strategic governance initiative. They use Unity Catalog to secure the PDF documents, call logs, and images that feed Agentic AI models. This capability creates a defensive moat that generalist partners cannot cross.

The Margin Gap

Consider the unit economics of two hypothetical Databricks partners:

- Partner A (The Generalist): Focuses on pipeline migration. Charges time-and-materials. Competes with offshore vendors. Gross Margin: 35%.

- Partner B (The Specialist): Focuses on "Data Products" and Governance. Deploys pre-configured Unity Catalog templates for PII masking, lineage, and "Volumes" security. Charges fixed-fee for strategy + recurring managed services for policy enforcement. Gross Margin: 55%+.

Private Equity buyers in 2026 are aggressively acquiring Partner B because they provide the infrastructure for Data & AI specialization. They are paying for the intellectual property of the governance framework, not the hours of the engineers.

The Execution Playbook: From Project to Platform

To capture the 14x multiple, partners must pivot their GTM motion from "implementation" to "governance assessment." This starts with a hard truth: Governance is the new perimeter.

Your sales conversation must shift from "We can migrate your data" to "We can secure your AI." Here is the diagnostic framework for 2026:

- Audit the Estate: Identify all workspaces still reliant on Hive Metastore. Position these not as "legacy" but as "AI-incompatible."

- Sell the "Volumes" Vision: Demonstrate how Unity Catalog is the only way to safely expose unstructured data to LLMs (like Mosaic AI). If they can't govern the file, they can't use the model.

- Package the Policy: Stop writing custom SQL grants for every client. Build a library of industry-specific governance templates (e.g., "HIPAA-Ready Unity Catalog Bronze Layer"). This moves you toward the software-like margins that drive elite valuations.

In 2026, you cannot be a "Databricks Partner" in name only. You are either a Governance Architect enabling the AI era, or you are a legacy vendor managing a dying metastore.