The practical answer

- Short answer

- For every $1 of Google Cloud consumption, partners can generate $7.05 in services revenue. Here is the diagnostic on escaping pilot purgatory and capturing the GenAI premium.

- Best fit

- Industry: Cloud Services / Technology. Function: Revenue Operations / Strategy

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 500% YoY growth in GenAI transaction volume on Google Cloud Marketplace

The 'Lift and Shift' Party Is Over (And the Hangover Is Expensive)

For the last five years, the Google Cloud Partner playbook was simple: migrate workloads, collect the resale margin, and maybe attach some low-level infrastructure managed services. If you were efficiently managed, you traded at 6x EBITDA. If you were growing fast, maybe 8x.

That era ended in Q4 2025.

The market has bifurcated. Infrastructure migration has become a race to the bottom, commoditized by automation and hyperscaler efficiency. Meanwhile, a new class of partner is trading at 12x-15x EBITDA. They aren't selling migrations; they are selling production AI.

According to a 2025 study by Canalys, for every $1 of Google Cloud technology sold, partners can now generate up to $7.05 in downstream services revenue. But here is the catch: you don't get that multiplier for moving a SQL database to BigQuery. You get it for building Agentic AI workflows that replace manual human labor.

If your 2026 forecast relies on "cloud modernization" retainers, you are holding a depreciating asset. The "multiplier" has moved up the stack. The money isn't in the cloud anymore; it's in the intelligence running on top of it.

The money isn't in the cloud anymore; it's in the intelligence running on top of it. If you're still selling 'migration,' you're selling a commodity.

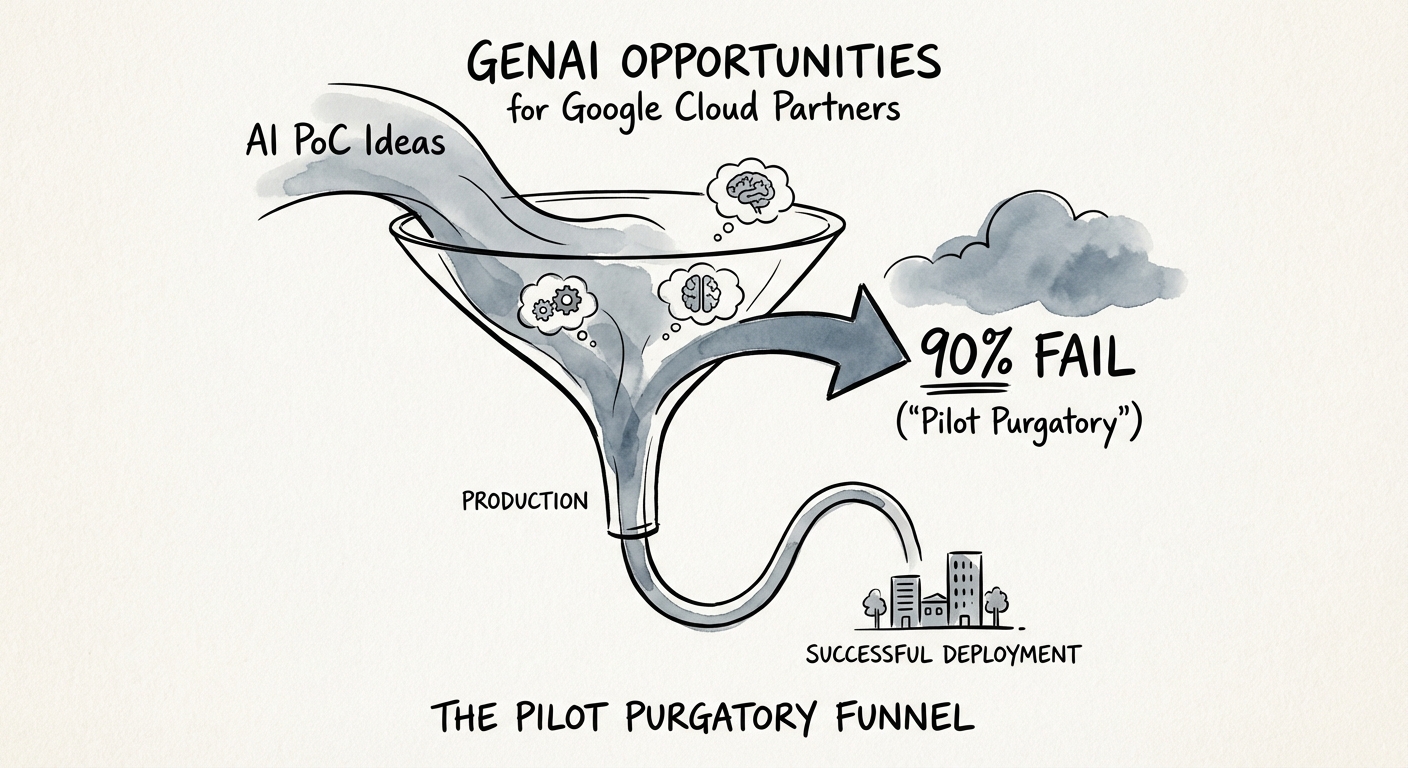

The 'Pilot Purgatory' Trap: Why Your Revenue Is Lumpy

You celebrated that $50,000 GenAI Proof of Concept (PoC) win last quarter. You shouldn't have.

The data on AI adoption is brutal for services firms that lack engineering rigor. Gartner reports that 30% of GenAI projects will be abandoned after PoC by the end of 2025. Other sources, like MLQ.ai, put the failure rate even higher, suggesting only 5% of custom enterprise AI tools reach production.

This creates a specific financial pathology I see in stalled Series B consultancies: The Science Fair Revenue Model.

Your team is busy. Utilization looks high (maybe too high, pushing 85%). But your revenue is non-recurring project churn. You are constantly hunting for the next "experiment" because the last three didn't convert to a $500k ARR managed service contract.

The Conversion Metric You Must Track

Stop measuring "AI Pipeline." It is a vanity metric. Start measuring PoC-to-Production Conversion Rate.

- Danger Zone: <10% (You are an R&D lab for your clients, funded by your own eroding margins).

- Stable: 20-30% (You have decent delivery, but poor qualification).

- Elite: >50% (You are selling outcomes, not technology).

Google Cloud's GenAI transaction volume grew 500% year-over-year. The demand is real. If you aren't capturing it, the problem isn't the market—it's your offer. You are likely selling "AI Strategy" (which is optional) instead of "Agentic Workflows" (which are operational necessities).

From 'Body Shop' to 'IP Factory': The Valuation Shift

Why do some Google Cloud partners trade at 4x revenue while others struggle to get 1x? It comes down to one question from the Private Equity buyer: "If your top 5 engineers leave, does the revenue stop?"

In the GenAI era, "Time and Materials" is a valuation killer. To capture the $7.05 multiplier, you must productize your service delivery. This doesn't mean you need to become a SaaS company. It means building IP Assets on top of Vertex AI that accelerate deployment.

Examples of High-Valuation Service IP:

- Industry-Specific Models: "We don't just 'do GenAI.' We have a pre-trained document processing agent for CPG Logistics that works on Day 1."

- Proprietary Evaluation Frameworks: "We use our own 'Trust & Safety' test suite to guarantee the model doesn't hallucinate compliance violations."

- Managed AI Ops: "We charge a flat monthly fee to monitor model drift and retrain agents, ensuring performance doesn't degrade."

This shifts your revenue quality from "one-off project" to "recurring technical retainer." In 2026 valuations, recurring services revenue commands a 2x premium over project revenue. If you want the exit, stop building science projects and start building production lines.