The practical answer

- Short answer

- Diagnostic guide for Oracle Partners: Why legacy 'Lift and Shift' models are killing valuation multiples and how to pivot to OCI consumption economics.

- Best fit

- Industry: Professional Services. Function: Revenue Operations

- Operating path

- GTM Execution → Commercial Performance → Performance Improvement

- Key metric

- 68% OCI Revenue Growth (Q2 FY2026) – The market opportunity is infrastructure, not just ERP.

The 'Lift and Shift' Commodity Trap

If your 2025 strategy relies on migrating on-premise Oracle EBS environments to OCI using a standard "lift and shift" methodology, you are building a commodity business. The market has spoken, and the numbers are brutal. While Oracle Cloud Infrastructure (OCI) revenue surged 68% in Q2 FY2026, the partners simply moving workloads are seeing margin compression, not expansion.

Why? Because "Lift and Shift" has become a race to the bottom. Automation tools have lowered the barrier to entry, and customers are no longer willing to pay premium hourly rates for basic infrastructure moves. Worse, the failure rate for these migrations remains stubbornly high—75% of cloud migrations stall or fail to deliver projected ROI, often because they simply replicate on-premise inefficiencies in a cloud environment.

For the founder, this manifests as a "Services Cycle." You close a migration deal, burn out your best engineers fighting legacy technical debt, and barely break even on the project margin, hoping to make it up on managed services. But if your managed service is just "keeping the lights on," you are vulnerable to the next lower-cost provider. To break this cycle, you must stop selling migration and start selling modernization.

You think moving your clients to OCI is a technical project. It's not. It's a P&L restructuring. If you don't own the consumption model, you're just a low-margin services provider with better certifications.

The New Economics: Consumption is King

Oracle’s 2025 partner incentive structure has shifted decisively. The money is no longer in the license transaction; it is in the consumption. With the "Enhanced Program Cloud Incentives" effective February 2025, Oracle is rewarding partners who drive sustained OCI usage, not just one-time setups. This aligns with the broader market shift where 82% of customers cite "managing cloud spend" as their top challenge.

This is your pivot point. Instead of being a "Migration Partner," you must become a "FinOps and Optimization Partner." The value proposition changes from "We move you to the cloud" to "We guarantee your unit economics in the cloud."

The "Fix and Optimize" Playbook

Successful partners are productizing their IP. They aren't just billing hours; they are deploying proprietary scripts to automate database patching, using AI to predict capacity needs, and offering "Zero-Downtime" guarantees backed by financial penalties. This shift allows you to move from low-margin project revenue (30-40% Gross Margin) to high-margin recurring revenue (60-70% Gross Margin). See our analysis on why cloud migration estimates are wrong by 3x to understand the scale of the problem you are solving.

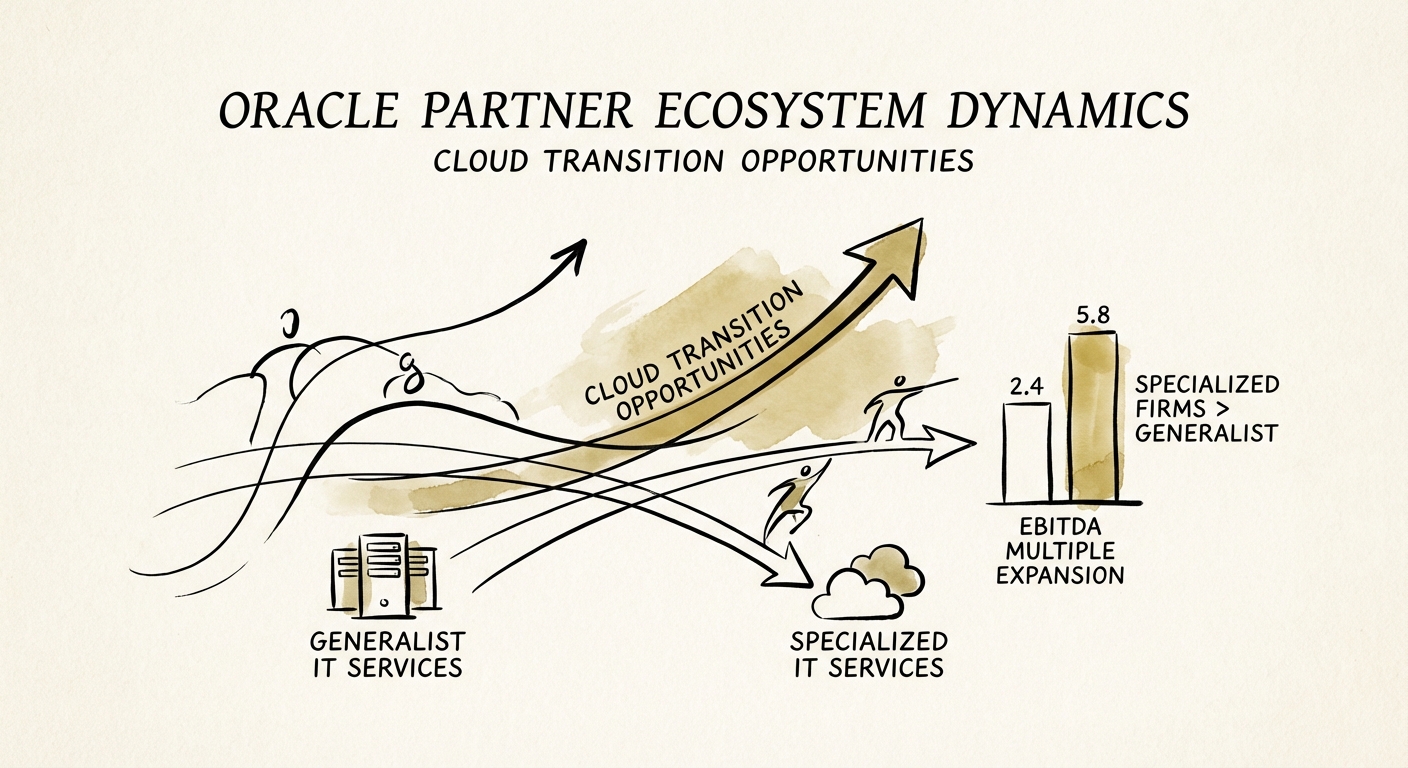

Valuation Reality: The 4x vs. 12x Spread

As an operator who has sat on both sides of the deal table, I can tell you that Private Equity buyers scrutinize Oracle partners differently in 2026. They don't care about your "Gold Partner" status; they care about your revenue quality.

A traditional Oracle service provider—heavy on one-time implementation revenue, low on recurring IP—trades at 4x to 6x EBITDA. You are viewed as a staffing firm with a logo. Contrast that with a "Cloud Platform Partner"—one that owns proprietary accelerators, has high NRR (Net Revenue Retention), and deep expertise in high-growth areas like OCI AI infrastructure. These firms are trading at 10x to 12x EBITDA, and in some cases, are valued on revenue multiples.

To bridge this gap, you must document your processes and turn tribal knowledge into turnkey IP. Read our guide on IT Services M&A trends to see exactly how buyers are pricing these assets. If you are still relying on "heroics" to deliver projects, you are capped at the lower multiple. Systematize your delivery, focus on consumption economics, and position yourself as a strategic enabler of Oracle's AI growth, not just a mover of servers.