The practical answer

- Short answer

- Generalist AWS partners trade at 6x EBITDA. Specialists trade at 12x. Here is the 18-month diagnostic roadmap to bridge the valuation gap before you sell.

- Best fit

- Industry: Cloud Consulting & Managed Services. Function: Corporate Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 11.4x Median EBITDA multiple for Managed Services Providers (MSPs) in H2 2025, recovering to pre-pandemic highs.

The "Generalist" Discount: Why Your Gold Status Isn't Enough

In 2022, you could sell a generic AWS Premier Partner shop for 10x EBITDA just by showing up with a few hundred certifications and a pulse. Those days are gone. The 2026 M&A market has bifurcated into two distinct realities: the Commodity Generalist and the Specialized Asset.

We are seeing generalist "Lift and Shift" migration shops trading at 5x to 7x EBITDA. Why? Because basic infrastructure migration is now a race to the bottom. Automation has compressed billable hours, and the "easy" workloads have already moved. If your revenue model relies on headcount-based staff augmentation or one-off migration projects, Private Equity buyers view you as a low-margin staffing agency, not a technology platform.

Contrast this with the Specialized Asset. AWS Partners focusing on high-complexity verticals—specifically Data & Analytics (Snowflake/Databricks ecosystems), Security-as-a-Service, and Agentic AI—are commanding 11x to 14x EBITDA multiples. The market data is merciless: buyers are paying a premium for outcomes and IP, not just billable hours. If 80% of your revenue is project-based "time and materials," you are leaving roughly half your potential exit value on the table.

Strategic buyers are willing to pay a 50% premium on EBITDA, but only if you fill a specific, high-complexity gap like Agentic AI or Data Security. General capacity is worth 6x. Niche capability is worth 12x.

The 3 Levers of Valuation Expansion

To move from the "Body Shop" discount to the "Platform" premium, you must fundamentally restructure your revenue architecture. We call this the "Exit Engineering" phase, and it typically requires 18 months of disciplined execution.

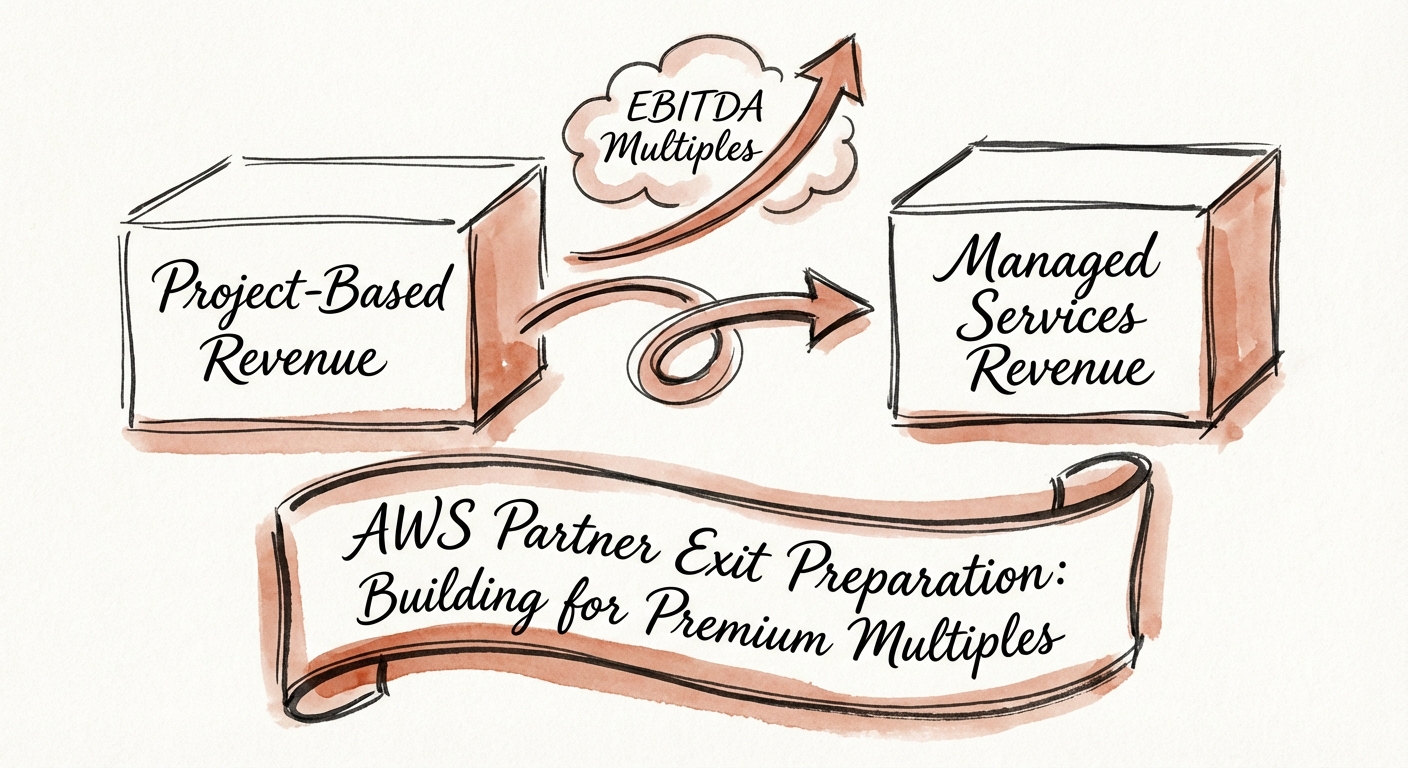

1. Revenue Mix: The 40% Recurring Threshold

Buyers scrutinize the quality of your revenue. Revenue quality audits in 2025 reveal that firms with >40% recurring revenue (Managed Services or IP-based subscription) trade at a 3-turn premium over pure professional services firms. You must pivot from "Project Recovery" to "Platform Management." Stop selling 3-month migrations; start selling 36-month "Modernization & Optimization" contracts. The data shows long-term contracts can increase valuation by 10-20%.

2. The Specialization Wedge

General "DevOps" is no longer a differentiator. The 2026 premium lies in Agentic AI and Security-as-a-Service. Partners who can demonstrate repeatable frameworks for deploying AI agents or securing multi-cloud environments are seeing managed services valuation margins of 60%+, compared to the 35% typical of general consulting. You need to pick a lane—Industry Cloud, FinOps, or SecOps—and own it completely.

3. Intellectual Property as a Multiple Multiplier

Do you have a "Way of Working" that is documented and software-enabled? Or does your value walk out the door every evening? Partners who package their methodology into "Accelerators" or proprietary tooling (even simple code-gen scripts) reduce key-person dependency. This is the difference between buying a business and buying a job for the founder.

The 18-Month Execution Roadmap

You cannot fix your multiple in the 60 days before signing an LOI. This is a surgical process that starts now.

- Months 1-6: Revenue Hygiene. Audit your existing contracts. Identify "bad revenue"—low-margin, high-friction clients—and fire them. Aggressively convert project customers to managed services, even if it means trading short-term cash for long-term contract value (ACV).

- Months 7-12: The IP Sprint. Document your "Tribal Knowledge." If your best architect is the only one who can deploy your solution, you have a scalability risk that changes deals. Build the standard operating procedures (SOPs) and internal tooling that allow junior engineers to deliver senior-level results.

- Months 13-18: The Financial Narrative. Clean up your books. Separate "One-time Implementation" revenue from "Recurring Managed Services" on the P&L. Ensure your Gross Margins on Managed Services are hitting the 50%+ benchmark. Buyers need to see the trend line moving up before they engage.

The goal is not just to sell. It is to sell for a multiple that rewards you for the decade of blood, sweat, and tears you poured into this business. Don't settle for the generalist discount.