The practical answer

- Short answer

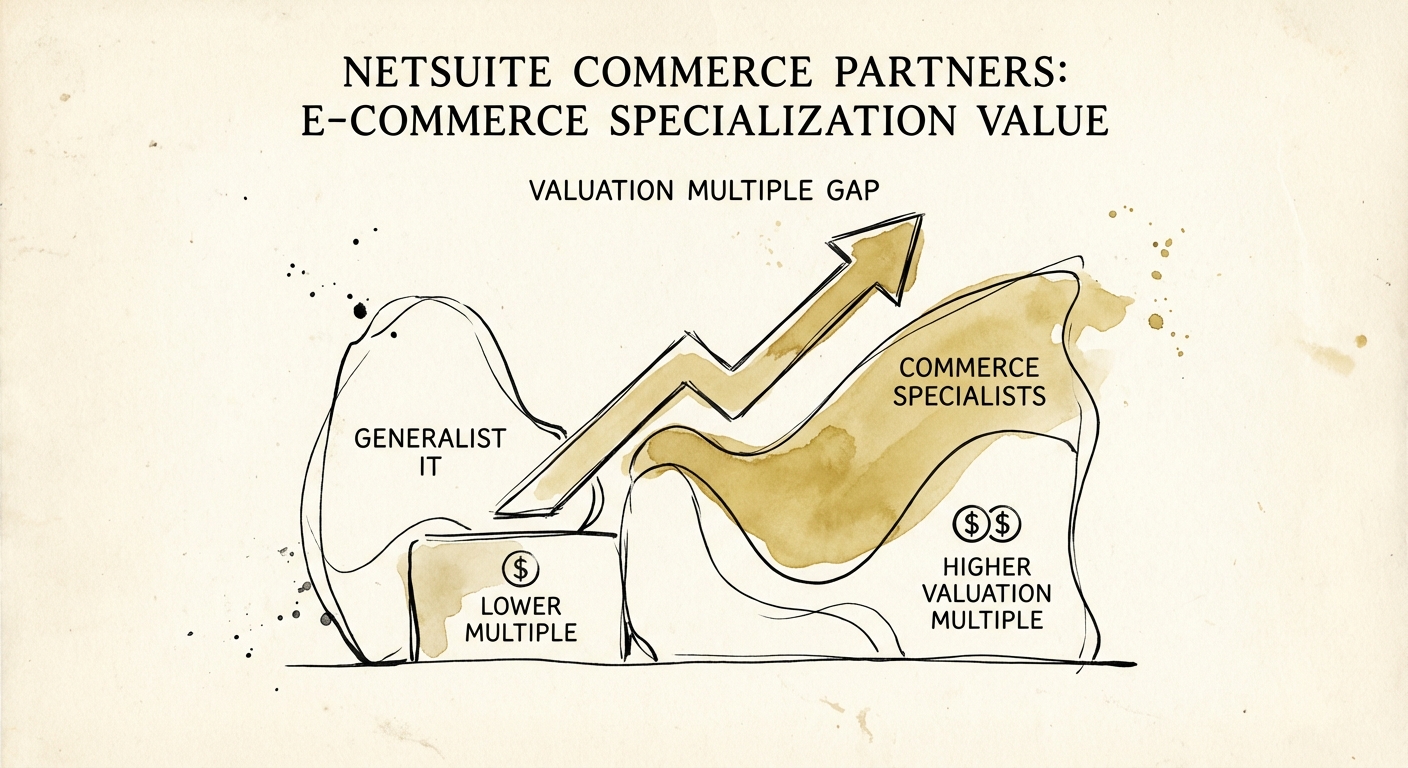

- Generalist NetSuite partners trade at 5x EBITDA. Commerce specialists trade at 10x. Here is the diagnostic framework to bridge the gap before you exit.

- Best fit

- Industry: IT Services / E-commerce. Function: M&A / Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 10x EBITDA multiple potential for specialized Commerce MSPs vs. 5x for Generalist ERP shops.

The 'Jack of All Trades' Discount

If you are running a NetSuite partner firm doing $10M–$20M in revenue, you are likely hearing two very different stories about your valuation. The M&A brokers promised you 10x EBITDA. The Letters of Intent (LOIs) landing on your desk are closer to 5x. Why the disconnect?

The market has bifurcated. In 2025, private equity buyers have stopped paying premiums for "capacity." They are no longer buying hours; they are buying platforms. A generalist NetSuite shop that implements ERP for anyone—from non-profits to manufacturers—is viewed as a low-margin staffing agency. You are trading on the Project Services curve, where multiples are compressed (typically 1.6x – 2.2x Revenue or 6x – 8x EBITDA).

Contrast this with the Specialized Commerce Partner. These firms focus specifically on SuiteCommerce Advanced (SCA) or complex B2B e-commerce integrations. Because e-commerce is revenue-generating mission-critical infrastructure (not just back-office record-keeping), the retainer models are stickier. The result? These firms are evaluated closer to Managed Services Providers (MSPs), where valuations consistently hit 8x – 12x EBITDA. If you look like a generalist, you get the generalist discount. If you look like a specialized platform, you get the premium.

You don't get a premium for knowing NetSuite. You get a premium for knowing why a distributor's checkout flow is failing at 2 AM on a Saturday.

The Vertical Velocity Trap

Many founders believe that narrowing their focus limits their Total Addressable Market (TAM). In the NetSuite ecosystem, the opposite is true. The broader your service offering, the lower your win rate and the lower your bill rates.

Data from 2025 indicates that specialized partners convert referrals at a 3.4x higher rate than generalists. Why? Because the complexity of B2B commerce has exploded. A distributor selling automotive parts needs specific functionality—core exchange management, fitment data integration, real-time inventory lookups—that a generic "NetSuite Expert" will fail to deliver.

When you specialize—for example, "The Premier NetSuite Commerce Partner for Automotive Aftermarket"—two things happen to your financials:

- CAC Plummets: You stop competing for "ERP implementation" keywords and start owning niche conversations.

- Gross Margins Expand: You can reuse IP (accelerators, connectors, themes) across clients, breaking the linear link between revenue and headcount.

See The Valuation Gap: Why MSPs Trade at 10x While Consultancies Struggle at 5x for a deeper dive into how this margin profile impacts your multiple.

Structuring for the Exit: The 'Commerce' Moat

To capture the specialization premium, you must restructure your revenue mix before you go to market. The single biggest value driver for a Commerce partner is the ratio of Managed Services (recurring) to Implementation (one-off) revenue.

E-commerce sites are living organisms. They break, they need updates, they need CRO (Conversion Rate Optimization). Unlike a static ERP implementation that might need a tune-up once a year, a high-volume B2B portal requires constant attention. PE buyers love this because it looks like SaaS revenue.

The Diagnostic Checklist

If you want the 10x multiple, your P&L needs to show:

- >40% Recurring Revenue: Monthly retainers for support, optimization, and managed hosting.

- Vertical IP: documented accelerators that reduce deployment time (see The Transferability Premium).

- Customer Concentration <15%: No single client should own your destiny.

For a detailed breakdown of how buyers view your numbers, read The Services Valuation Matrix. Stop selling hours. Start selling the specialized outcome of digital revenue reliability.