The practical answer

- Short answer

- Why ISVs ignoring the Azure Marketplace are losing 30% of deal value. The 2026 guide to MACC, co-sell incentives, and valuation multiples.

- Best fit

- Industry: B2B SaaS / ISV. Function: Revenue Architecture

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 32% Projected share of ISV revenue transacted via Marketplaces in 2025 (up from 20%).

The 'Direct Sales' Era Is Over (And MACC Killed It)

If you are still forcing enterprise buyers to open a new PO for your software, you are actively sabotaging your win rate. The old playbook—hire expensive AEs, bang on doors, and fight for net-new budget—is dying. The new playbook is budget redirection.

Here is the reality: Your target enterprise customers are sitting on $460 billion in committed cloud spend (MACC). This isn't 'maybe' money. It is 'use it or lose it' money. When a CIO has $5M remaining on their Azure commit and 60 days to burn it, they aren't looking for a new vendor to run a six-month procurement gauntlet. They are looking for a solution they can buy with a click to satisfy their contract.

We are seeing ISVs with 'Co-sell Ready' status and transactable Marketplace listings close deals 40% faster than their direct-sales counterparts. Why? Because you aren't asking for new money. You are solving a procurement problem. You are helping them burn down a commitment they are legally obligated to pay anyway. If you aren't listed, you aren't just losing the deal; you aren't even in the room.

You aren't selling software anymore. You're selling a way for the CIO to hit their burn-down target. If you aren't transactable, you're invisible.

The 3% Tax That Buys You a Trillion-Dollar Sales Force

Founders used to complain about the 20% marketplace transaction fee. That excuse died years ago when Microsoft slashed the fee to 3%. Now, the math is undeniable. You are paying a 3% 'tax' to access the world's largest enterprise sales force.

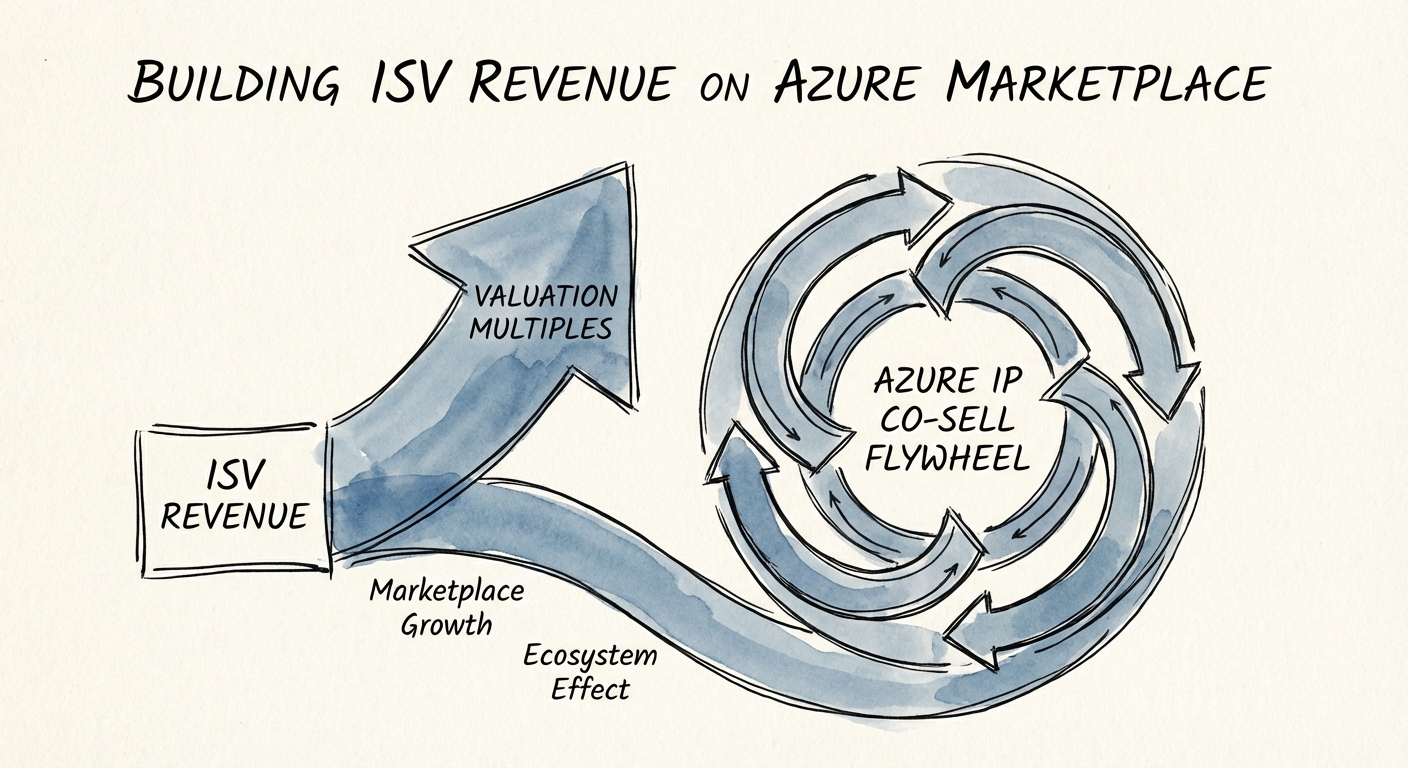

Here is how the 'Co-sell Flywheel' actually works in the trenches:

- Quota Retirement: Microsoft reps retire their quota when they sell your software. When you are 'Azure IP Co-sell Eligible,' you become a tool for them to hit their number.

- The Incentive Game: Microsoft pays its reps to sell specific solutions. If you align your architecture (specifically leveraging Azure services) with their incentives, you get walked into accounts you couldn't penetrate in a decade of cold calling.

- CAC Compression: We see Marketplace-native ISVs running with a Customer Acquisition Cost (CAC) 30-50% lower than direct peers. When a Microsoft PDM (Partner Development Manager) brings you a deal, your marketing spend is zero.

Stop viewing the Marketplace as a 'listing.' It is a distribution channel that scales faster than your internal hiring plan ever could.

Valuation Impact: The 'Marketplace Premium'

When Private Equity firms look at your CIM (Confidential Information Memorandum), they aren't just looking at ARR. They are looking at Revenue Quality. Marketplace revenue is superior to direct revenue for three specific reasons that drive multiple expansion:

1. Frictionless Renewals

Procurement friction is the silent killer of NRR (Net Revenue Retention). Marketplace renewals are often auto-approved because they fall under the umbrella of the larger cloud contract. We consistently see Marketplace-heavy ISVs maintain NRR 10-15 points higher than direct-sales peers.

2. The 'Vendor Consolidation' Moat

In a downturn, CFOs cut vendors. They rarely cut the cloud provider. By embedding your billing into the Azure invoice, you become 'infrastructure' rather than 'discretionary software.' You survive the cut.

3. Scalability Without Headcount

Growing to $50M ARR usually requires an army of sales reps. Marketplace-led growth allows you to scale revenue without linearly scaling SG&A. This efficiency explodes your Rule of 40 score, which is the primary lever for valuation multiples in 2026. A $20M ISV growing at 40% with 20% margins (via Marketplace efficiency) trades at a significantly higher multiple than a $20M ISV growing at 40% with 0% margins (via direct sales bloat).