The practical answer

- Short answer

- Why ISVs on Google Cloud Marketplace trade at higher multiples. 2026 benchmarks on sales cycle acceleration, win rates, and the $460B committed spend opportunity.

- Best fit

- Industry: B2B SaaS / ISV. Function: Revenue Architecture

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

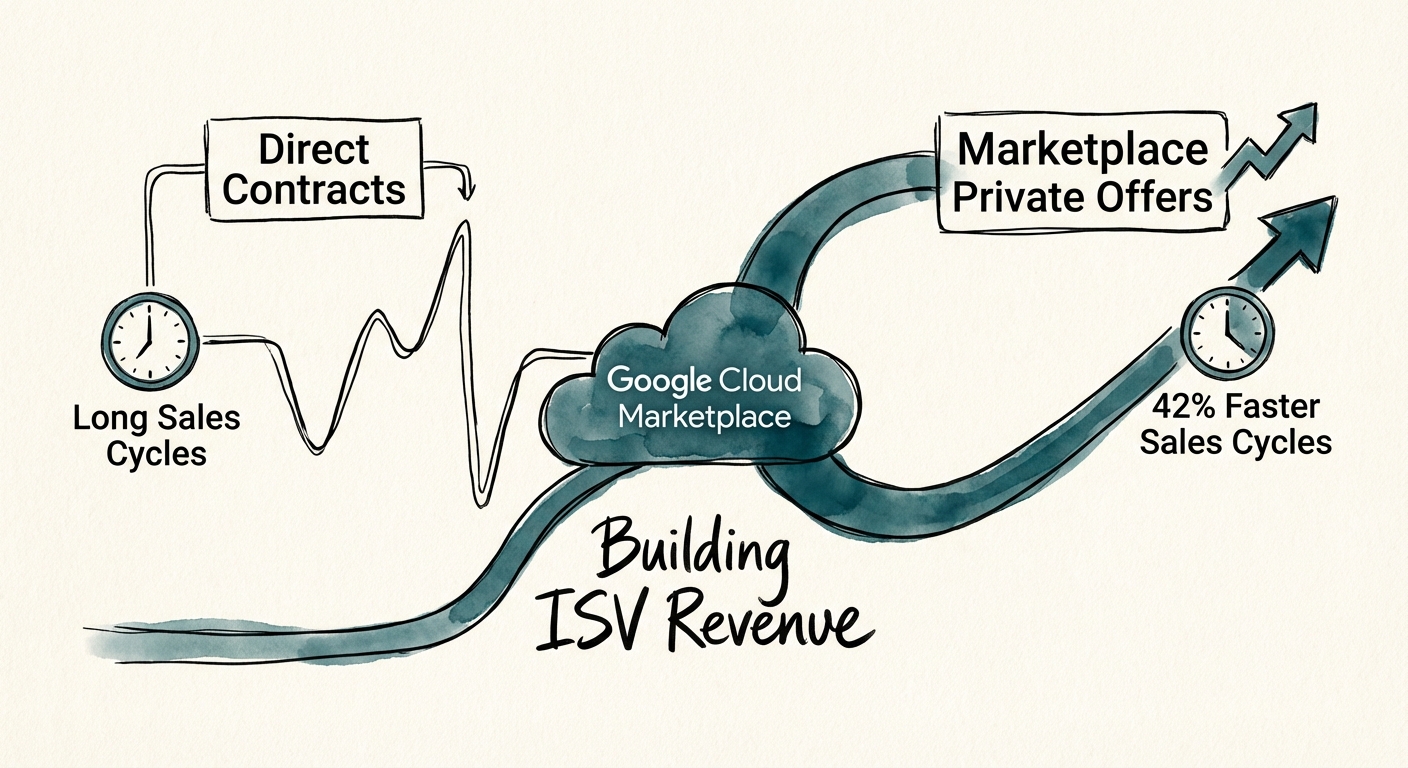

- 42% Reduction in sales cycle length for deals transacted via Google Cloud Marketplace vs. Direct.

The Valuation Delta: Why Marketplace Revenue is 'High Quality'

In the private equity data rooms I sit in, not all ARR is created equal. There is 'Hard ARR'—revenue you have to claw from a CFO's cold hands every renewal cycle—and there is 'Programmatic ARR'—revenue that flows through established budget pipes. Google Cloud Marketplace revenue is the latter, and in 2026, it commands a valuation premium that most founders are completely missing.

The math is brutal for direct sellers. We are seeing a bifurcation in SaaS valuations. The 'Generic SaaS' bucket trades at roughly 4x-6x revenue. But ISVs with significant Marketplace transaction volume—specifically those leveraging the co-sell motion—are seeing term sheets in the 8x-10x range. Why? Because the unit economics are fundamentally superior. CAC Payback on Marketplace deals is often 30-40% faster because you aren't fighting for new budget; you are reallocating committed budget.

According to 2025 data from Google Cloud and Omdia, Marketplace transactions accelerate deal cycles by 42% compared to direct paper. When a PE buyer models your future growth, they aren't just looking at your historical growth rate; they are looking at your friction coefficient. A sales process that requires a new vendor setup, legal redlines, and net-new budget approval is high-friction. A Marketplace Private Offer that burns down an existing Google Cloud commitment is low-friction. In the current M&A climate, you are paid a premium for that lack of friction.

You can fight for net-new budget, or you can help a CIO burn down a $10M Google commitment they're terrified of wasting. One of these paths leads to a 4-month sales cycle; the other closes in 30 days.

The $460B 'Use It or Lose It' Crisis Budget

The single biggest missed opportunity for B2B ISVs today is ignoring the 'Cloud Commit' distinct asset class. By 2025, global cloud commitments (EDP/commit contracts) exceeded $460 billion. This is money that enterprise CIOs have already promised to spend with Google, AWS, or Microsoft. If they don't use it, they lose it.

For a founder, this changes the sales pitch from "Please find $150k for my software" to "Let me help you save the $150k you're about to forfeit to Google." It is a balance sheet conversation, not a budget conversation. And with the 2025 updates to Google's partner program, the incentives are now aggressively aligned to favor you. Google now allows for 100% commit drawdown on Channel Private Offers (capped at 25% of the total commit), meaning you can leverage your channel partners to unlock this spend without taking the direct contracting hit.

We recently advised a Series C DevOps company that shifted its entire enterprise closing motion to Google Cloud Marketplace. The result wasn't just faster deals; it was higher win rates. Win rates via co-sell engagements jumped by 35%. Why? Because the Google Cloud rep is incentivized to help you close. When you transact on Marketplace, you are retiring their quota too. You effectively expand your sales team from 10 reps to 10,000 reps, all hunting for the same budget unlock.

The M&A Reality: Buyers Want 'Ecosystem Flywheels'

When we prepare a company for exit, we look for 'Marketplace Density.' A firm with 0% Marketplace revenue looks like a traditional sales org—expensive, linear, and prone to attrition. A firm with 20-30% Marketplace revenue looks like a platform play. The 2025 Tackle.io State of Cloud Marketplaces Report indicates that Marketplace revenue is expected to jump from 20% to 32% of total revenue for best-in-class ISVs in the next 12 months.

This is what strategic acquirers call the 'Multiplier Effect.' Data shows that for every $1 of Google Cloud consumption, partners generate roughly $7.05 in their own revenue. If you can prove to a buyer that you are part of that $7.05 ecosystem, your valuation is no longer capped by your own sales capacity. You are valued on the growth of the underlying cloud platform.

The Diagnostic Test for Your Board:

1. What percentage of our pipeline is tagged for Marketplace transaction?

2. Are we active in the Google Cloud Partner Advantage program to receive co-sell incentives (reduced listing fees of 1.5% for renewals)?

3. Is our sales comp plan neutral (or accelerated) for Marketplace deals to prevent rep resistance?

If the answer to any of these is 'No' or 'I don't know,' you are leaving multiple turns of EBITDA valuation on the table. In 2026, the Marketplace isn't a channel; it's your new CFO.