The practical answer

- Short answer

- Why Veeva Vault ISVs trade at 8x-12x revenue while services firms stall at 10x EBITDA. A strategic guide for founders on the Salesforce-to-Vault migration opportunity.

- Best fit

- Industry: Life Sciences Technology. Function: Product Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12x Revenue Multiple for 'Agentic' Vault ISVs

The Valuation Play: Services vs. IP on the Vault

For the last decade, the "Veeva Economy" has been a gold rush for services firms. With Veeva Systems (NYSE: VEEV) capturing over 80% of the global life sciences CRM market and trading at a ~$35B market cap, the ecosystem of implementation partners, data migration specialists, and managed services providers has flourished. However, a stark divergence in exit valuations has emerged in the 2025-2026 M&A cycle.

Pure-play Veeva services firms—those focused on implementation, configuration, and managed services—are trading at 10x to 12x EBITDA. While respectable, this model faces inherent scaling friction: revenue growth is linearly tied to headcount, and gross margins rarely exceed 45%. In contrast, "Vault Certified" ISVs (Independent Software Vendors) that build native applications on the Veeva Vault Platform are commanding 6x to 12x Revenue multiples. For a firm with $10M in revenue, this is the difference between a $20M exit (at 10x EBITDA with 20% margins) and an $80M+ exit.

The driver of this premium is the "Regulatory Moat." Unlike generalist B2B SaaS, applications built on Vault inherit Veeva's compliance architecture (21 CFR Part 11, GxP). Acquirers—specifically Private Equity firms consolidating the Life Sciences Commercial & R&D tech stack—pay a premium for this pre-validated integration because it removes the single biggest friction point in pharma software adoption: the 12-to-18-month security and compliance audit.

The migration from Salesforce to Vault CRM is not just a platform shift; it resets where ecosystem IP can be built, packaged, and valued.

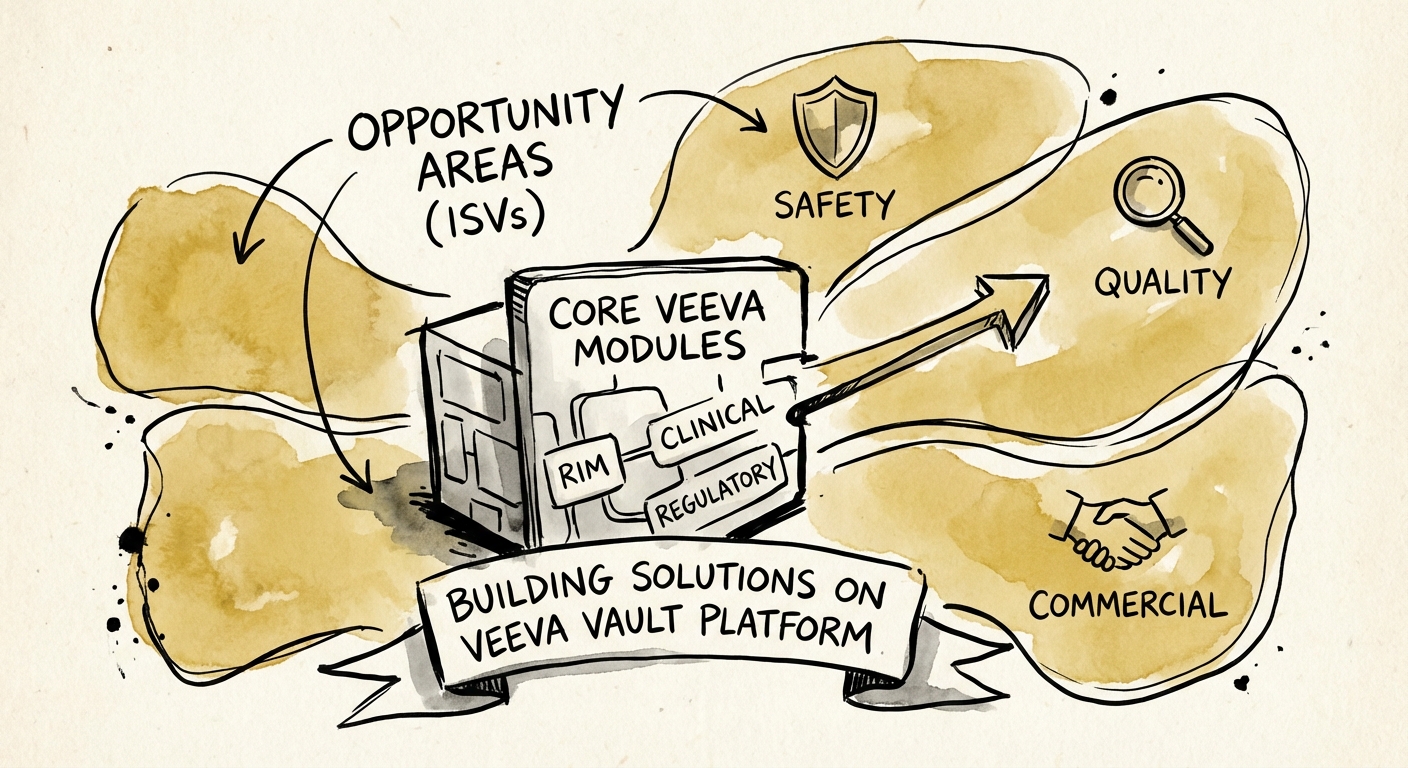

The 'White Space' Analysis: Where to Build in 2026

The most common mistake founders make is attempting to compete with Veeva's core modules. You will not beat Veeva at Clinical Data Management (CDMS) or Core CRM. The alpha lies in the "Edge Cases"—specialized workflows that are too niche for Veeva's $3B revenue engine to prioritize, but critical enough for top-tier pharma to buy.

1. The Salesforce-to-Vault CRM Migration Catalyst

Veeva's strategic decision to migrate its entire CRM customer base from Salesforce to the native Vault CRM by 2030 is the single largest ISV opportunity of the decade. This migration breaks thousands of legacy integrations and customizations built on the Salesforce Force.com platform. ISVs that build "bridge" solutions or native Vault replacements for these legacy Salesforce tools (e.g., specialized Key Opinion Leader mapping, sample management logistics, or field force gamification) will see explosive demand.

2. The 'Agentic' Safety & Quality Opportunity

With the release of the Veeva AI Partner Program and Direct Data API, the market is shifting from "Systems of Record" to "Systems of Intelligence." We are seeing a valuation premium for ISVs building AI Agents that sit on top of Vault Safety or Vault Quality. For example, an application that autonomously drafts narrative reports for adverse events using Vault data (and then routes them for human approval) commands a significantly higher multiple than a standard reporting dashboard. The "Agentic Premium" in HealthTech M&A is currently driving valuations toward the upper end of the 8x-12x revenue range.

Strategic Alignment: Positioning for the Exit

Building on Vault is not just a technical decision; it is a capital markets strategy. To realize the ISV premium, founders must structure their relationship with Veeva carefully to avoid the "Platform Risk" discount during due diligence.

- Certified Technology Partner Status: This is non-negotiable. PE buyers view "Silver" or "Gold" status as a proxy for technical debt reduction. It validates that your API usage aligns with Veeva's roadmap and won't break with the next release.

- Commercial Independence: While the Veeva App Store is a powerful channel, your revenue quality depends on direct paper. Acquirers scrutinize "Marketplace Dependency." A healthy mix is 30% Marketplace-sourced / 70% Direct-sourced revenue.

- The Data Rights Framework: Ensure your IP agreements with customers explicitly grant you rights to train models on anonymized metadata. In the 2026 M&A environment, your data moat is as valuable as your code.

The window to establish dominance on the native Vault platform is narrowing. As the migration to Vault CRM accelerates through 2026, the "incumbent" spots for the next generation of life sciences tools are being filled. For services firms, the move is clear: productize your most repeatable workflows now, or watch your valuation cap out at 10x EBITDA while your product-led peers trade at 10x Revenue.