The practical answer

- Short answer

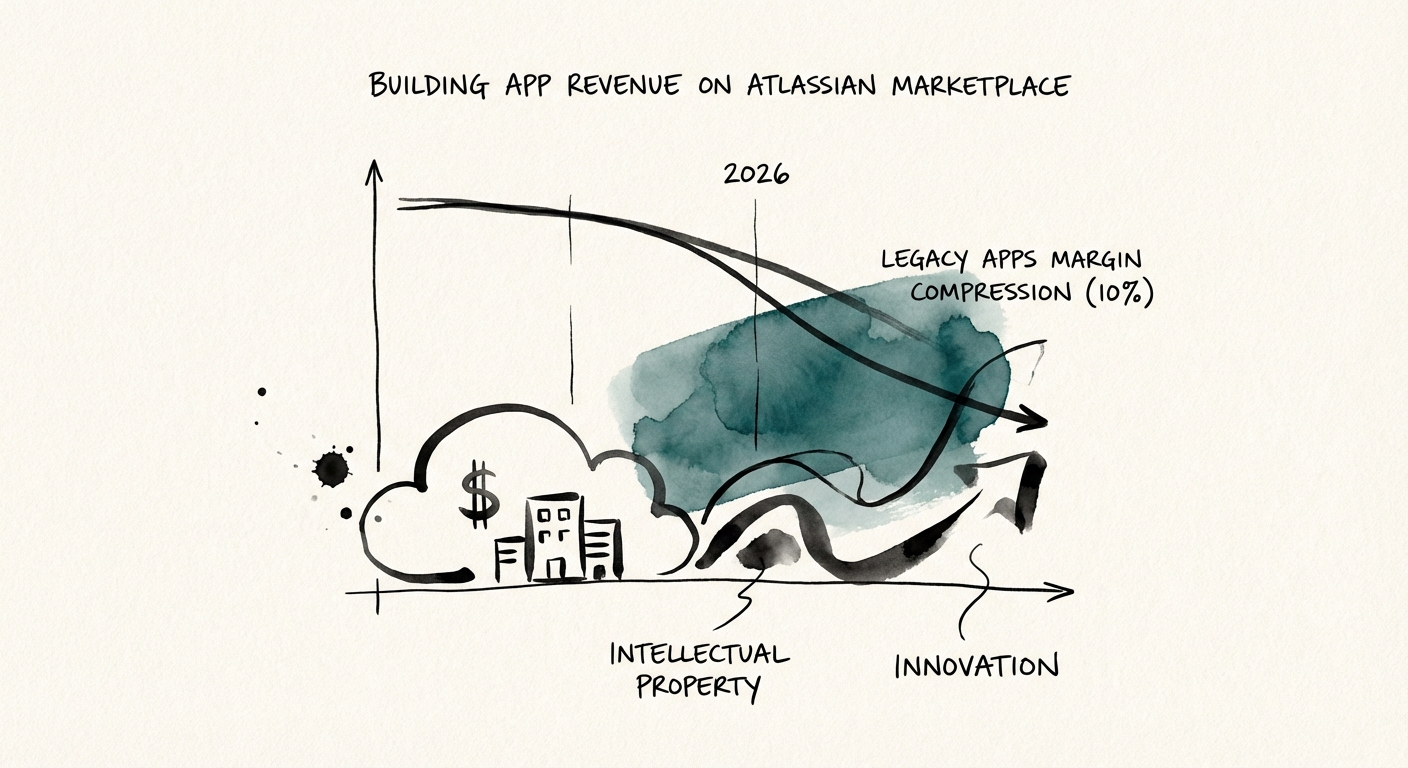

- New 2026 revenue share rules are splitting Atlassian ISV valuations. Learn why 'Cloud Fortified' Forge apps trade at 12x while legacy Connect apps face a 10% margin cliff.

- Best fit

- Industry: B2B SaaS. Function: Product Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 10% Gross margin reduction for legacy 'Connect' apps starting July 2026 due to new take rates.

The 2026 'Connect' Cliff: A Solvable Valuation Crisis

For the last decade, the Atlassian Marketplace has been the gold standard for B2B bootstrapping—a $1.8B ecosystem where a developer could build a "Connect" app and reach 300,000 customers with minimal overhead. That era ended as the 2026 marketplace economics changed.

Atlassian’s new revenue share structure creates a binary valuation event for every ISV in the ecosystem. The take rate for legacy "Connect" apps is rising from 15% to 20% in January, and then to 25% by July 2026. Conversely, apps built on the new "Forge" platform will see rates stabilize at ~17%, with a 0% revenue share on the first $1M of lifetime revenue.

This isn't just an operational detail; it is a valuation cap. If you are generating $5M ARR on the legacy Connect framework, your gross margins will structurally compress by 1000 basis points over the next 18 months. Private equity buyers, specifically the roll-up vehicles like Appfire and Tempo, are already pricing this risk into LOIs. They aren't paying 12x EBITDA for an asset with a built-in margin contraction; they are paying 4x-6x for the "migration burden" they will have to shoulder post-close.

If you are holding a legacy Connect app with high churn and no security badge, you are not ready for a strategic exit. You are ready for a distressed asset sale.

The 'Cloud Fortified' Premium: Why Security is the New Sales Enablement

In the Atlassian ecosystem, "features" are easily Sherlocked (replicated by the platform), but "infrastructure" commands a moat. The dividing line between a disposable feature and critical infrastructure is the Cloud Fortified designation.

Our analysis of recent ecosystem M&A activity shows a clear bifurcation in deal value:

- Standard Apps: Trade on SDE (Seller Discretionary Earnings) multiples. These are viewed as "features" susceptible to churn as Atlassian releases native updates (like Rovo AI).

- Cloud Fortified Apps: Trade on Revenue multiples. These apps have passed Atlassian’s rigorous security, reliability, and support SLAs.

The valuation driver here is Net Revenue Retention (NRR). Cloud Fortified apps are eligible for adoption by Atlassian’s Enterprise tier customers—the cohort migrating from Data Center to Cloud with 155% ROI expectations. These enterprise customers rarely churn. Consequently, Cloud Fortified apps frequently demonstrate NRR above 110%, while standard apps struggle to maintain 90% due to SMB churn. In due diligence, that 20% NRR gap translates to a 4-turn difference in EBITDA multiples.

The Exit Strategy: Pivot to Platform or Perish

The most successful exits in 2025/2026—such as Appfire’s acquisition of JXL—share a common trait: they are not just "Jira plugins"; they are multi-ecosystem platforms or deep process integrations.

To position your ISV for a premium exit, you must execute a "Defensive Rearchitecture" before you go to market:

- Migrate to Forge: You cannot sell a "Connect" app in 2026 without taking a valuation haircut. The buyer will deduct the cost of migration (technical debt) and the risk of the 25% take rate from your Enterprise Value.

- Secure the Badge: "Cloud Fortified" is not optional. It is the primary filter for PE-backed strategic acquirers who need to ensure your code won't trigger a compliance fire drill post-acquisition.

- Diversify the Surface Area: The "Sherlock" risk is highest for single-function apps (e.g., "Time Tracking for Jira"). Apps that bridge ecosystems—connecting Jira to Salesforce, or Confluence to Microsoft Teams—trade at premium multiples because they solve the "Context Switching" problem that Atlassian itself cannot fully address.

If you are holding a legacy Connect app with high churn and no security badge, you are not ready for a strategic exit. You are ready for a distressed asset sale. The window to fix this closes when the new rates take effect.