The practical answer

- Short answer

- Building on Adobe Exchange? Discover why ISVs trade at 8x revenue while service partners stall at 8x EBITDA. A strategic diagnostic for Adobe partners.

- Best fit

- Industry: MarTech / SaaS. Function: Product Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 8x-12x Target Revenue Multiple for Adobe ISVs with >110% NRR and 'Resell' status.

The Tale of Two Exits: Service vs. IP

In the Adobe ecosystem, not all revenue is created equal. For a founder running a Gold or Platinum Solution Partner firm, the path to $20M in revenue is often paved with headcount: hiring more AEM architects, more Marketo consultants, and more project managers. You are building a machine that converts human hours into billable outcomes. The market rewards this efficiency with a valuation of 8x to 12x EBITDA—a respectable exit, but one capped by the linear physics of professional services.

Contrast this with the 'Adobe ISV' model. A partner who builds a proprietary application on Adobe Exchange—whether it's a workflow automation for Workfront or a headless commerce plugin for Magento—is playing by a different set of rules. These firms are valued not on the profit left over after paying expensive consultants, but on top-line growth and recurring revenue quality. In 2025, high-performing B2B SaaS assets in specialized vertical ecosystems traded at 6x to 10x Revenue (ARR).

The Math of the Pivot

Consider two firms, both generating $10M in revenue:

- Firm A (Agency): $10M Revenue, 20% EBITDA margins ($2M). Valuation at 10x EBITDA = $20M Enterprise Value.

- Firm B (ISV): $10M ARR, growing 40% YoY. Valuation at 8x Revenue = $80M Enterprise Value.

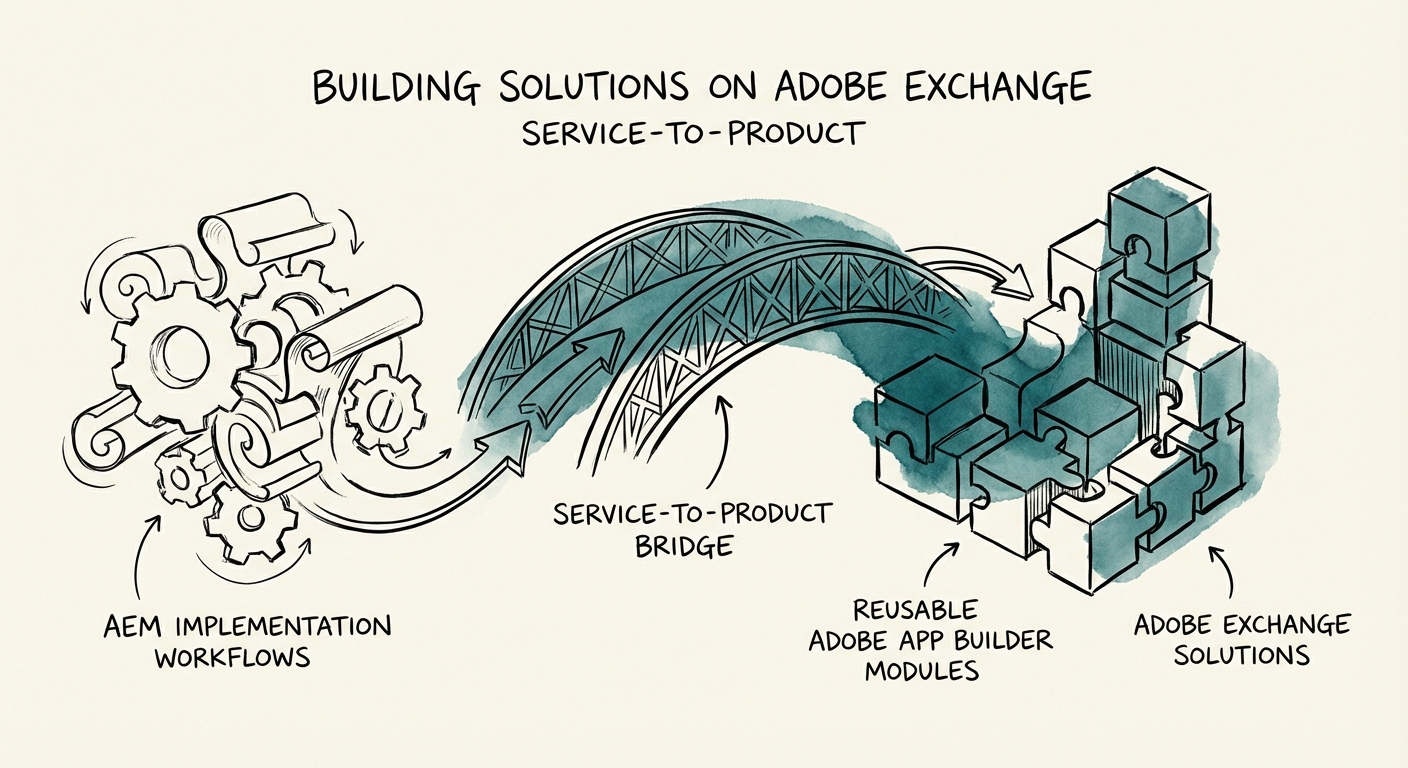

The strategic imperative for Adobe partners is clear: you do not need to abandon services, but you must extract Intellectual Property (IP) from your delivery capability. The 'Service-to-Product' bridge is the single most effective lever for multiple expansion in the mid-market.

You do not need to abandon services, but you must extract IP from your delivery capability. The 'Service-to-Product' bridge is the single most effective lever for multiple expansion.

The 'Connector' Trap vs. The 'Embedded' Premium

Not all Adobe Exchange apps command premium multiples. A common failure mode we see in Exit Readiness assessments is the 'Connector Trap.' This occurs when a partner builds a simple data pipe—moving leads from Marketo to a CRM, or assets from AEM to a DAM—and calls it a product. While useful, 'connectors' are increasingly commoditized by native integration platforms (iPaaS) and Adobe's own expanding feature set.

To unlock the ISV Premium, your solution must move from connecting data to acting on it. The most valuable ISVs in the Adobe ecosystem build Embedded Workflows. They don't just transfer data; they allow the user to complete a high-value task without leaving the Adobe interface.

The 'Sticky' Criteria for PE Buyers

Private Equity acquirers scrutinize three specific metrics when evaluating Adobe ISVs:

- Workflow Gravity: Does the user spend time in your panel? Apps that serve as a 'second screen' for AEM power users often see churn rates below 5%.

- Adobe App Builder Utilization: Innovative partners are leveraging Adobe App Builder to build cloud-native apps that run serverless within Adobe's infrastructure. This lowers COGS, improves security compliance, and signals deeper technical alignment to buyers.

- The 'Resell' Motion: Are you relying solely on your own sales team, or have you unlocked the ISV Resell motion where Adobe reps retire quota by selling your solution? Achieving 'Resell' status (like Sinch and others have) is a significant valuation accelerant because it lowers your CAC drastically.

Strategic Diagnostic: Are You Building a Feature or a Business?

Before investing engineering resources into the Adobe Exchange, run your product roadmap through this Exit Readiness Diagnostic. If you answer 'No' to more than two of these, you are likely building a low-value utility rather than a high-value asset.

The 5-Point ISV Assessment

- 1. The 'Native' Test: Can your app's core functionality be replicated by a proficient AEM architect in a 2-week sprint? (If yes, you are selling a script, not software).

- 2. The Data Moat: Does your application generate unique metadata or analytics that Adobe doesn't natively capture? (e.g., Granular content performance data inside Analytics).

- 3. The Expansion Path: Do you have a clear path to Net Revenue Retention (NRR) above 110%? (i.e., Can you sell more 'seats' or 'usage' as the customer's Adobe footprint grows?).

- 4. The Service Drag: Does every $1 of ARR require $2 of implementation services to deploy? (If so, you are still a service shop in disguise).

- 5. The Ecosystem Fit: Is your app aligned with Adobe's strategic growth vectors—specifically GenAI (Firefly) and Real-Time CDP? Buyers are paying a premium for apps that operationalize Adobe's AI capabilities.

For founders, the goal is not to stop doing services—services pay the bills. The goal is to use your service margins to fund the development of an asset that will one day be worth 4x more than the service business itself.