The practical answer

- Short answer

- Why RevOps consultancies trade at 12x EBITDA while marketing agencies stall at 5x. A diagnostic guide for HubSpot partners and PE investors on the 2026 valuation gap.

- Best fit

- Industry: B2B Tech Services. Function: Revenue Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 15x EBITDA multiple for niche tech-enabled consulting firms in 2025, compared to ~5x for generalist agencies.

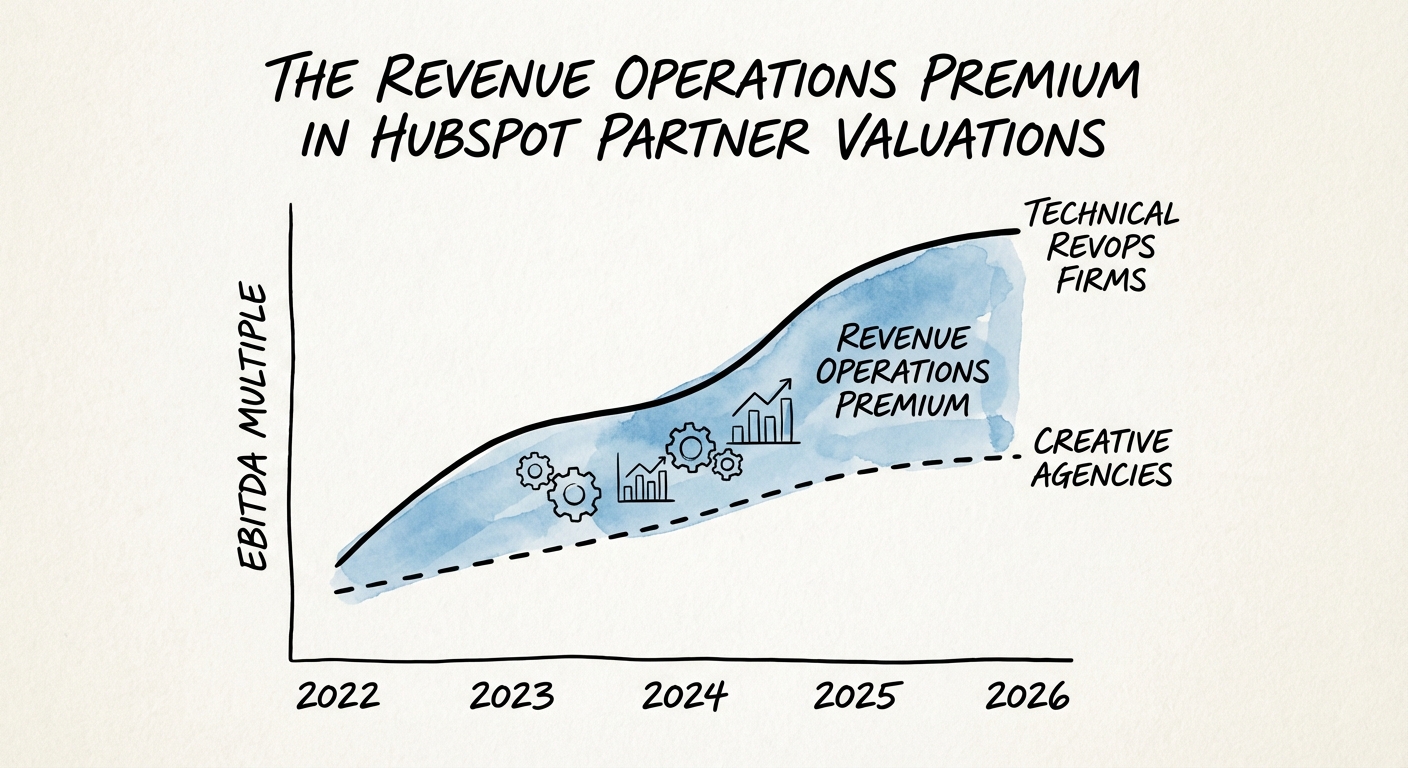

The Valuation Bifurcation: Campaigns vs. Architecture

In 2026, the HubSpot ecosystem is no longer a monolith. It has fractured into two distinct asset classes with vastly different exit profiles: Creative Agencies and Revenue Operations (RevOps) Consultancies.

For the last decade, “Diamond” status was the primary value driver. Today, Private Equity buyers have stopped looking at tier badges and started looking at the nature of revenue. The market data is brutal for generalists:

- Creative & Marketing Agencies: Trading at 4x–6x EBITDA. The commoditization of content by Generative AI has spooked investors. If your primary revenue stream is writing blog posts or designing landing pages, buyers view your moat as non-existent.

- Technical RevOps & System Integrators: Trading at 10x–15x EBITDA. These firms are viewed as “Tech-Enabled Services.” They own the infrastructure, the data model, and the integrations. They are the architects of the “Commercial Operating System.”

Why the gap? It comes down to replacement cost. A marketing agency can be fired with an email. A RevOps firm that built the CPQ logic, orchestrated the data warehouse sync, and manages the attribution model is nearly impossible to rip out without stalling revenue. PE firms pay for that permanence.

Marketing agencies are rented. Revenue Operations firms are installed. In the eyes of a private equity buyer, that distinction is worth 7 turns of EBITDA.

The “Agentic” Shift: The New 2029 Growth TAM

The valuation premium isn’t just about defense; it’s about the future growth story. IDC and HubSpot project the ecosystem opportunity to swell to $36 billion by 2029, but that growth isn’t coming from more email templates.

It is coming from AI Agents and Workflow Orchestration. 40% of the ecosystem’s growth will be driven by AI-powered solutions. The partners commanding premium multiples today are those positioning themselves as the builders of the “autonomous enterprise.”

When we advise PE sponsors on add-on acquisitions, we run a “Revenue Quality” diagnostic that separates low-value service revenue from high-value technical revenue:

- Low-Value Revenue (Commoditized): Content creation, social media management, basic SEO, ad management.

Valuation Impact: Drag. Treated as “pass-through” labor. - High-Value Revenue (Structural): CRM migration, data governance, API integration, CPQ implementation, AI agent training.

Valuation Impact: Multiplier. Treated as “IP-adjacent” revenue.

If you are a RevOps leader looking to exit, you must pivot your narrative from “marketing retainer” to “infrastructure management.” The former is an expense; the latter is an asset.

The Pivot Playbook: From 5x to 12x

If you are currently a HubSpot agency owner stuck in the “Generalist Trap,” you can engineer a higher multiple, but it requires a radical shift in your service mix over the next 18 months.

1. Audit Your Revenue Mix

Calculate what percentage of your revenue comes from “doing the work” (creative) vs. “building the machine” (RevOps). If technical services are under 30%, you are an agency. If they are over 60%, you are a consultancy. Shift the mix.

2. Productize Your Intellectual Property

Don't sell “consulting hours.” Sell “The [Your Firm] Architecture.” Document your standard operating procedures for data migration, lead scoring, and lifecycle stages. When a buyer sees documented IP, they see transferability. Revenue multiples are a myth; documented processes that guarantee EBITDA are reality.

3. Lock in Recurring Technical Revenue

Move clients from “retainers for hours” to “Managed RevOps Subscriptions.” Frame this as “Systems Uptime” and “Data Integrity Assurance.” Recurring revenue attached to system health trades at a premium because it looks like SaaS NRR (Net Revenue Retention).

The window to make this transition is narrowing. By 2027, the bifurcation will be complete. You will either be a low-margin content shop fighting AI, or a high-margin RevOps architect commanding a strategic premium.