The practical answer

- Short answer

- Usage-based SaaS trades at 24x vs 19x for seat-based peers in 2026—but diligence quietly reclassifies volatile usage as one-off services. How to defend it.

- Best fit

- Industry: B2B SaaS. Function: Revenue Operations

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 24x Average revenue multiple for AI-enabled, usage-based companies in 2025 (Bessemer Cloud 100).

The same dollar, two very different multiples

Picture a founder-CEO who sells an AI-heavy data product on pure consumption. Trailing twelve months: $14M. Growing 60% a year. She walks into a process expecting the headline number everyone's been quoting—AI-enabled, usage-priced companies trading at a premium to the old seat-based world. Per Bessemer Venture Partners' 2025 Cloud 100 benchmarks, that's roughly 24x revenue for AI-enabled, consumption-led companies versus about 19x for non-AI, seat-based peers. The growth case is just as flattering: data from Monetizely and OpenView shows usage-based models growing roughly 38% faster than rigid subscriptions.

Then the quality-of-earnings team opens her billing exports, and the number on the deal moves the other direction.

Here's the thing the multiple charts never tell you: the buyer is not valuing your pricing model. They're valuing how legible your revenue is to a spreadsheet. Seat-based SaaS is boring and legible—1,000 seats, recognized flat, churn is a clean percentage. Consumption revenue is the opposite. It's lumpy, it spikes, it goes quiet for a month, and to a diligence analyst that lumpiness reads as risk until you prove otherwise. The premium isn't free. It's a bet that you can make consumption look as predictable as a subscription while keeping the expansion upside that makes it grow faster.

So you end up living in two valuation worlds at once. The marketing world quotes 24x. The diligence world asks, line by line, "would I underwrite this dollar at full multiple, or treat it like a one-time charge?" Most founders never see the second conversation coming, because it doesn't happen in the pitch—it happens in a data room three weeks in, after the LOI, when re-trading is cheap for the buyer and expensive for you. If you want the mechanics of how the multiple itself gets built, our ARR multiple calculator walks through it.

The market pays 24x for consumption, but a quality-of-earnings analyst pays 1.5x for anything that doesn't show up on a predictable line every month. Your job before a process is to make your usage revenue boring enough to underwrite—without killing the expansion that earns the premium in the first place.

What the diligence team actually does to your usage revenue

They cohort it and they stare at the variance. Specifically, they're hunting for two things, and both can quietly halve your effective multiple.

The first is month-to-month swing. If a customer runs a giant batch job in March, nothing in April, and a medium load in May, your "recurring" revenue from that account isn't recurring—it's episodic. When a meaningful slice of your base swings hard month over month with no contractual floor underneath it, the analyst stops trusting the trailing-twelve-month figure as a run-rate. They'll normalize down to the trough, not the average, and the gap between those two numbers is real money. Say a $14M TTM book where a third of revenue is uncommitted and spiky—normalize that third to its floor and you've shaved a couple million off the base the multiple gets applied to. Same business, smaller anchor.

The second is the overage masquerading as ARR. This is the one that kills deals. Zone & Co reports that PE investors are increasingly hunting for "revenue leakage" in usage models—and the most common leak is a company counting a year of one-off overage charges as if it were contracted ARR. If you bill in arrears and recognize flat, or you've stacked unbilled overages into your ARR figure, the QofE will find the gap, and the buyer will reclassify those dollars as professional-services-style revenue. That bucket trades closer to 1.5x than 10x. I've watched processes stall right there: the "Usage ARR" line that anchored the whole pitch turned out to be a series of overages the buyer simply refused to underwrite at SaaS multiples.

The test to run on yourself before they run it on you

Pull twelve months of billing by account. For each customer, separate the contractually committed floor from everything billed above it. The committed floor is your defensible ARR—it survives diligence at full multiple. Everything above it is upside you have to earn the right to count. If the above-floor portion is most of your revenue, you don't have a recurring-revenue business with usage upside; you have a metered-utility business wearing a SaaS costume, and the multiple will reflect that. Before you build that bridge, sanity-check your recognition logic against our breakdown of how revenue recognition gaps stall deals, because a clean variance story with dirty recognition still fails.

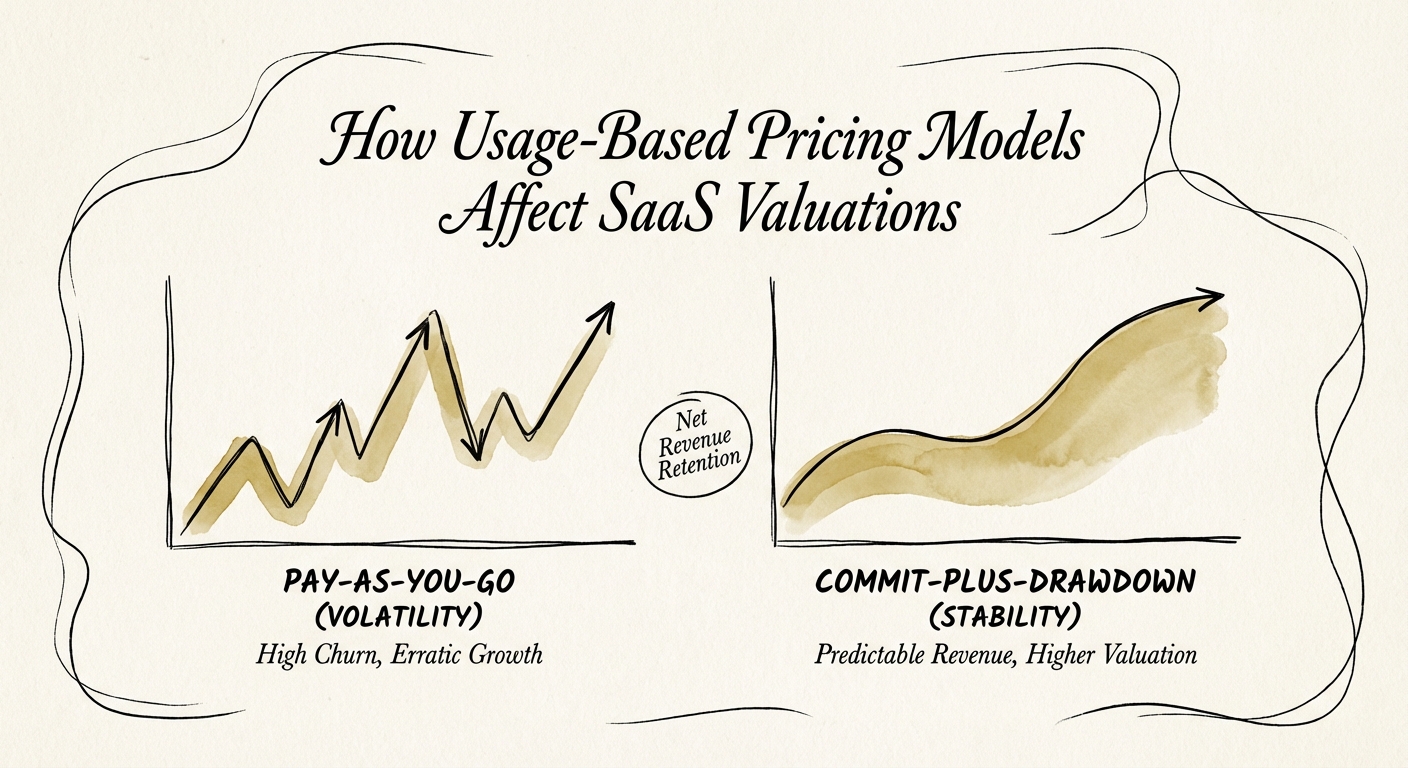

The fix: give them a floor to underwrite and a ceiling to dream on

The structural answer is not "go back to seats." It's the committed-drawdown contract—and it's where the data actually points. The 2025 Pricing Trends Report from Maxio found that hybrid models combining a subscription commitment with usage posted the highest median growth rate at 21%, beating both pure subscription and pure pay-as-you-go. Hybrid wins because it's the only structure that satisfies both valuation worlds from section one at the same time.

The shape is simple. Two parts, and the order matters:

- The committed floor. The customer pre-commits to a minimum annual spend—say a $100k commitment that buys a bucket of credits or units. You recognize this ratably as recurring revenue. This is the dollar the QofE team underwrites at full multiple, because it shows up the same every month whether they touch it or not. It's the part that makes a diligence analyst exhale.

- The metered ceiling. Usage above the committed bucket bills at the metered rate, or—better—trips an automatic mid-term true-up that resets the commitment higher. This is where your net revenue retention lives, where the expansion velocity that earns the 24x conversation actually comes from. You keep the upside; you just stop pretending it's contracted before it's contracted.

Done right, you convert volatile utility revenue into predictable SaaS revenue without capping the expansion. The diligence team gets a floor they can normalize against, so the volatility argument loses its teeth; you keep the path to 140% NRR that makes consumption businesses compound. The work you do Monday is concrete: re-paper renewals to carry a real minimum commitment, separate committed from metered in your billing system so the two are reportable on day one of a process, and stop reporting above-floor overage as ARR in your own board decks—because the version of your numbers the buyer trusts is the conservative one you can prove. If you want to push the retention side of that equation, start with net revenue retention vs. gross revenue retention.