The practical answer

- Short answer

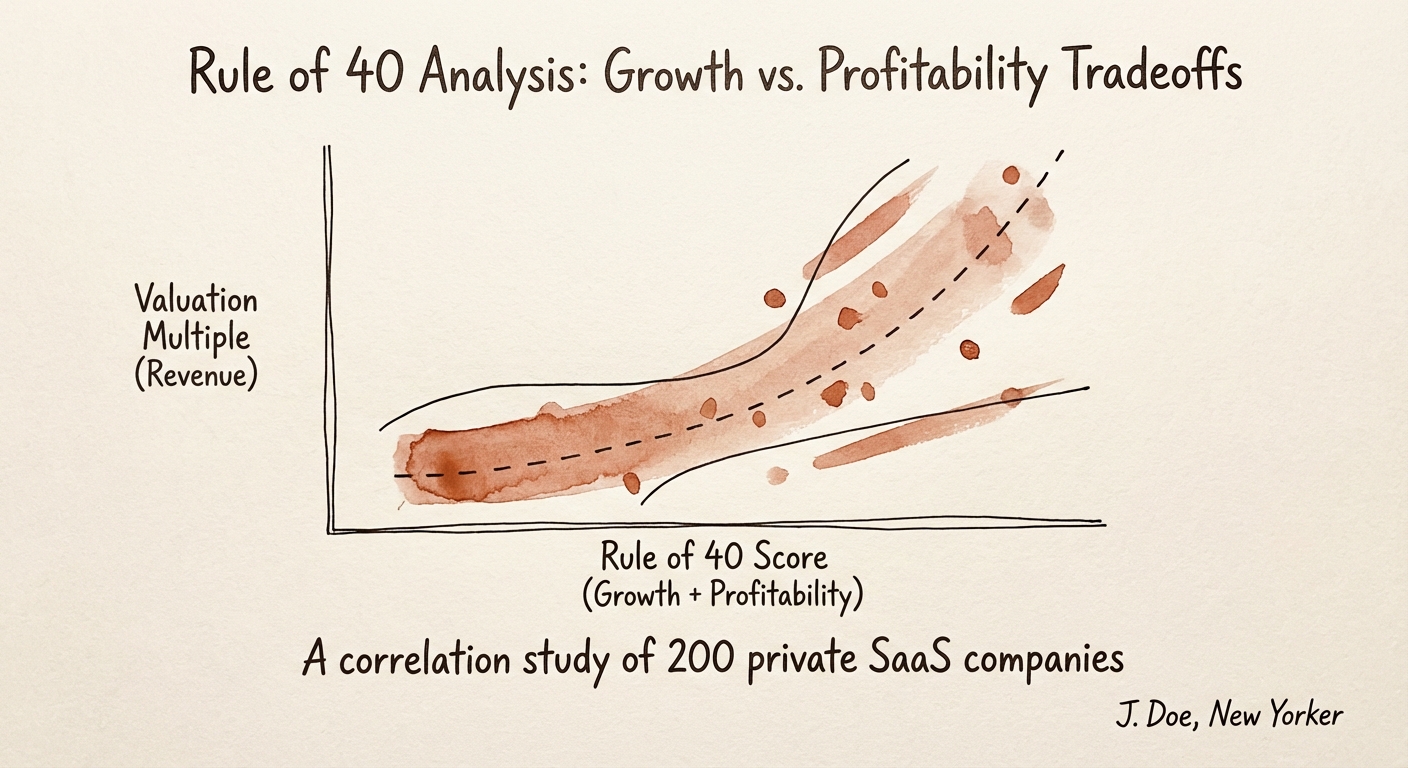

- In 2026, the Rule of 40 determines exit multiples. Learn why PE firms value 'Balanced 40' companies at a 121% premium over 'Growth at All Costs' peers.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 121% Valuation premium for companies beating the Rule of 40 vs. those that don't (RockingWeb 2025 Benchmarks).

The 'Growth at All Costs' Hangover

For a decade, the formula for a premium SaaS exit was simple: grow at 50%+, and the margins will follow. In 2026, that playbook is not just outdated; it is a liability. The market has bifurcated. While venture capitalists still chase the "Rule of X" (weighting growth 2x over profitability), private equity—the dominant acquirer for scaling B2B SaaS companies—has shifted to a "Weighted Rule of 40" that penalizes cash burn more heavily than ever before.

Recent data from 2025 benchmarks reveals a stark reality: median private SaaS growth rates have stabilized at approximately 26%, down from the heady 50%+ medians of the zero-interest rate policy (ZIRP) era. More importantly, only 11-30% of companies currently achieve a true Rule of 40 score (Growth % + Profit margin % ≥ 40%). Those that do are not just receiving a pat on the back; they are commanding a 121% valuation premium over their peers. The market is no longer paying for "hollow" growth bought with unsustainable burn.

The Composition Trap

The standard Rule of 40 suggests that 40% growth with 0% margin is equal to 20% growth with 20% margin. To a 2026 PE buyer, this is mathematically false. The "Hollow 40" (High Growth / Zero Margin) carries execution risk, funding risk, and integration complexity. The "Solid 40" (Balanced Growth / Healthy Margin) implies a self-sustaining engine. In our analysis of recent LOIs, companies with a balanced composition (e.g., 25% Growth / 15% EBITDA) consistently trade at higher revenue multiples than their burn-heavy counterparts, even if the total Rule of 40 score is identical.

The 'Growth at All Costs' playbook is finished. In 2026, you don't get credit for buying revenue with venture dollars. You get credit for building a machine that prints cash while it scales.

Diagnostic: Where Do You Fall on the Efficiency Matrix?

To prepare for a 2026 exit, you must map your company not just by the sum of your metrics, but by their composition. PE buyers categorize targets into four distinct quadrants during financial due diligence. Knowing where you stand determines whether you receive a 6x or a 12x offer.

1. The Venture Path (High Growth / Negative Margin)

Profile: Growth > 40%, Margins < -20%.

Valuation Driver: Bessemer's "Rule of X" applies here. If you are truly growing at 80%+, investors will tolerate burn. But if growth slows to 30% while burn remains high, you enter the "Valuation Death Zone."

Risk: High sensitivity to market sentiment. If the window closes, you have no runway.

2. The PE Powerhouse (Balanced Growth / Moderate Margin)

Profile: Growth 20-30%, Margins 10-20%.

Valuation Driver: This is the sweet spot for 2026 buyouts. These companies command the highest multiples because they offer "optionality"—the buyer can choose to pour gas on the fire or harvest cash flow without fixing a broken P&L first.

Action: Optimize CAC Payback to prove efficiency.

3. The Cash Cow (Low Growth / High Margin)

Profile: Growth < 10%, Margins > 30%.

Valuation Driver: Valued on a multiple of EBITDA rather than Revenue. Often trades at a lower absolute dollar value but offers the highest certainty of close.

Risk: Being labeled a "declining asset" if retention slips.

4. The Danger Zone (Low Growth / Low Margin)

Profile: Growth < 20%, Margins < 10%.

Valuation Driver: Distressed asset pricing. Buyers will model a "turnaround" scenario, deducting the cost of RIFs and operational fixes from the purchase price.

Strategic Pivot: From Burn to Balance in 12 Months

If you find yourself in the "Danger Zone" or arguably even the "Venture Path" without the requisite 50%+ growth to justify it, you have approximately 12 months to pivot your financial profile before testing the market. The goal is to migrate toward the "PE Powerhouse" quadrant.

1. Audit Your 'Hollow' Revenue

Not all revenue counts toward the Rule of 40 in the eyes of a buyer. Service revenue with 20% gross margins drags down your efficiency score. Audit your SaaS Quick Ratio. If you are buying revenue through aggressive paid spend with a CAC Payback > 18 months, stop. It inflates your growth rate but destroys your valuation multiple.

2. The Rule of 40 'Add-Back' Reality

Founders often try to game the Rule of 40 by using "Adjusted EBITDA" heavily laden with add-backs. In 2026, buyers are skeptical. While one-time legal fees are acceptable adjustments, "capitalized software development" that looks like ongoing R&D is often rejected. Aim for a "Clean Rule of 40" based on Operating Cash Flow (OCF) rather than creative EBITDA. A lower, cleaner score is often valued higher than an inflated, messy one.

3. Pricing as a Margin Lever

The fastest way to impact both sides of the Rule of 40 equation is pricing. A 10% price increase flows 100% to the bottom line (improving Margin) and increases top-line velocity (improving Growth). In a market where new logo acquisition is harder, Net Revenue Retention (NRR) expansion through pricing power is the hallmark of a premium asset.