The practical answer

- Short answer

- Earnouts are bridging the valuation gap in 33% of SaaS deals, but the average payout is just 21 cents on the dollar. Here is how to design a structure that actually pays.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 33% Deals including earnouts to bridge valuation gaps in 2024-2025.

The Valuation Gap and the "Paper" Premium

In the current SaaS M&A market, a dangerous disconnect exists. Founders, anchoring on 2021 comparable transactions, often enter negotiations expecting revenue multiples of 8x or higher. Strategic acquirers and PE firms, disciplined by the higher cost of capital in 2025, are writing offers closer to 4.1x revenue or 14x EBITDA. The mechanism used to bridge this chasm is the earnout—contingent consideration paid out over 12 to 36 months post-close.

According to recent data from SRS Acquiom, earnouts now appear in approximately 33% of non-life sciences deals, a significant uptick driven by valuation uncertainty. On paper, the math looks attractive: a $50M upfront payment plus a $20M earnout allows the founder to tell their board they achieved a $70M exit. It validates the "premium" valuation the seller demanded.

However, the data reveals a brutal reality: the average earnout pays just 21 cents on the dollar. For every $10M of contingent value you negotiate into the LOI, you can statistically expect to see only $2.1M. The rest is lost to integration friction, misaligned metrics, and the buyer’s operational changes. If you are banking on the earnout to make the deal economics work, you are not selling your company; you are buying a lottery ticket with your own equity. To beat these odds, you must move beyond "standard" terms and design a structure that survives contact with the buyer's post-merger integration plan.

If you are banking on the earnout to make the deal economics work, you are not selling your company; you are buying a lottery ticket with your own equity.

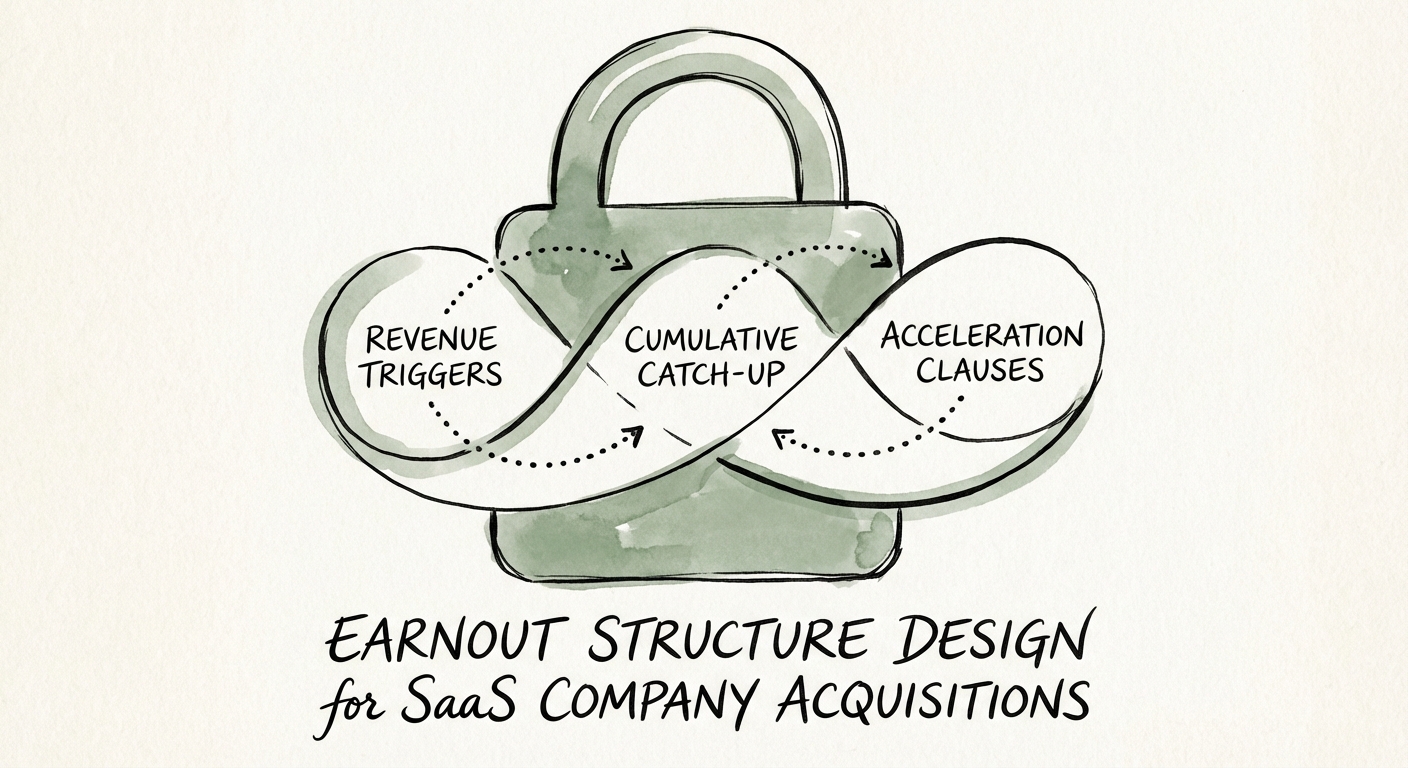

Designing the "Triple-Lock" Structure

The primary reason earnouts fail is metric ambiguity. A buyer’s definition of "EBITDA" or "Net Revenue" post-close will almost certainly differ from your definition pre-close. To secure your payout, you must negotiate a "Triple-Lock" structure that isolates your performance from the buyer's interference.

1. Top-Line over Bottom-Line

Never accept an EBITDA-based earnout if you are a growth-stage SaaS company. Post-acquisition, the buyer will load your P&L with corporate overhead, integration costs, and "synergy" expenses that depress EBITDA. Structure your earnout based on Gross Revenue or ARR (Annual Recurring Revenue). Specifically, define ARR to include price increases implemented by the buyer, but exclude churn caused by the buyer's decision to sunset products or change service levels.

2. The Cumulative Catch-Up

Avoid binary "cliff" targets where missing a milestone by $1 means earning $0. Instead, negotiate a cumulative catch-up provision. If you miss the Year 1 target but exceed the Year 2 target, you should be able to "catch up" and earn the full amount. This protects you against the inevitable friction of the first 6 months of integration, where sales velocity often dips as teams adjust to new systems.

3. The "Deemed Achieved" Clause

Your legal agreement must include acceleration triggers. If the buyer terminates you without cause, sells the company again, or fundamentally alters the business model (e.g., switching from direct sales to channel sales), the earnout should be deemed achieved at 100%. Without this, you are handing the buyer an option to fire you to save millions in deferred purchase price.

The "Commercially Reasonable Efforts" Defense

The legal battleground for earnouts is the "Commercially Reasonable Efforts" (CRE) clause. Buyers will push for "absolute discretion" to run the business post-close. You must resist this. Recent Delaware Chancery Court rulings, such as Fortis Advisors v. Johnson & Johnson, have resulted in billion-dollar damages against buyers who failed to use commercially reasonable efforts to achieve earnout milestones.

However, relying on litigation is a failure state. Instead, define CRE explicitly in your purchase agreement. It should mandate that the buyer cannot reduce the marketing budget below a certain percentage of revenue, cannot reassign your engineering team to other portfolio products, and must maintain your pricing structure within a specific band. If they breach these operational covenants, the earnout creates a defensive liability that forces them to the negotiating table.

Finally, demand a separate P&L for the earnout period. If your product is bundled into a larger suite, revenue recognition becomes a black box. You need a clear, pre-agreed methodology for allocating revenue from bundled deals to your specific earnout metrics. Without this, the buyer's "suite strategy" will cannibalize your exit value.