The two LOIs on your desk are not in the same currency

Picture the moment most B2B software founders are actually trying to optimize for: two letters of intent, side by side. Offer A is $40M, all cash at close. Offer B is $50M total — $35M at close, $15M tied to an earnout you hit over the next two years. Your brain does the only math it knows how to do under adrenaline. Fifty is bigger than forty. Offer B wins.

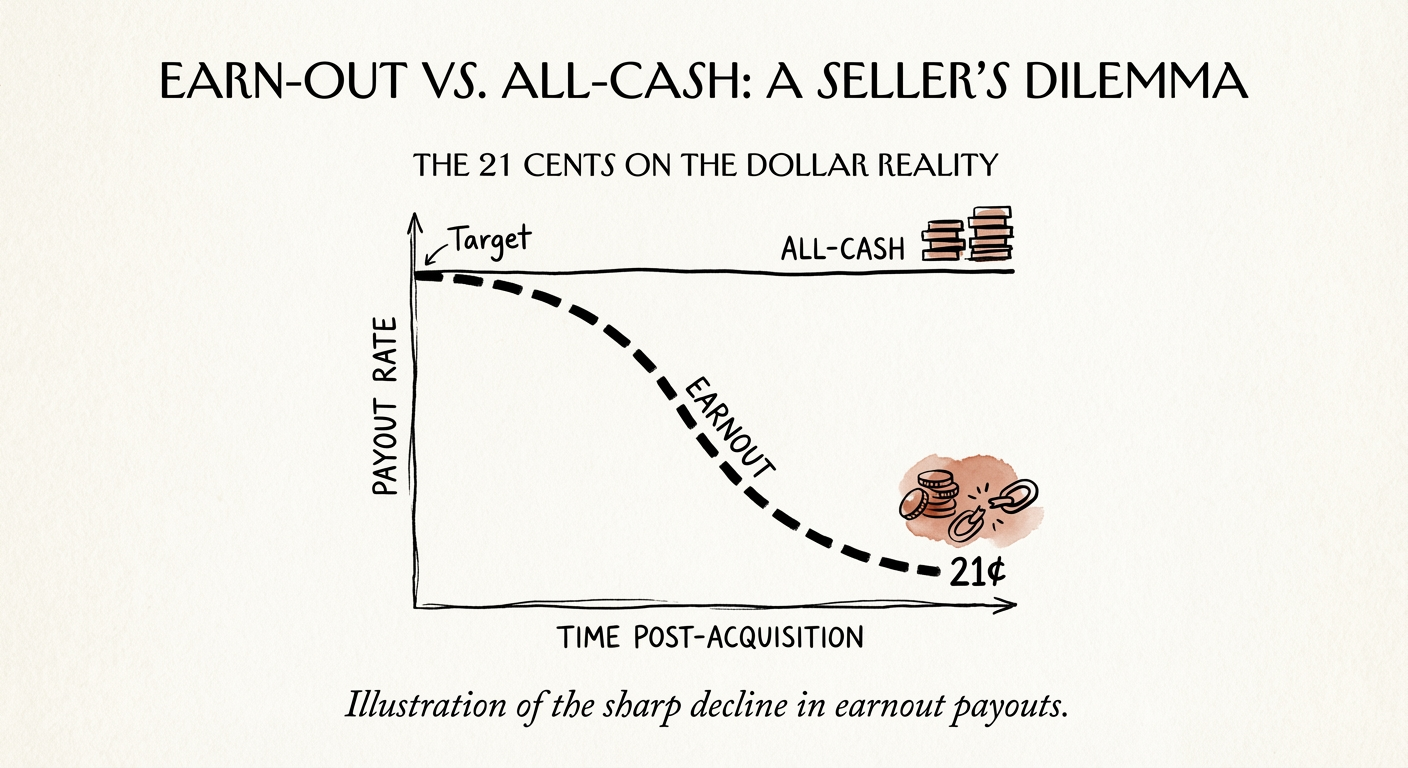

That instinct is the single most expensive reflex in a founder exit, because the two numbers are denominated in different currencies. The $40M is dollars. The $15M earnout is a lottery ticket priced at face value. And the 2025 data on what those tickets actually pay is brutal: across private-target deals outside life sciences, earnouts pay out an average of roughly 21 cents on every promised dollar, per the SRS Acquiom 2025 M&A Deal Terms Study. Even when something does land, sellers commonly collect only about half of the maximum they were dangled.

Run your $15M earnout through that lens and it stops being $15M. As a risk-adjusted expected value it's closer to $3M — and the variance around that number is enormous, because whether you hit it depends less on your product than on a buyer's portfolio cash needs eighteen months from now. So the real comparison isn't $50M vs. $40M. It's $40M of certainty against roughly $38M of hope. The reason this matters more in 2025 than it did three years ago is volume: earnouts now appear in a large and rising share of private deals as buyers use them to bridge stubborn valuation gaps, a trend documented by both Goodwin Procter and Womble Bond Dickinson. More founders are being handed this structure than ever, and most are scoring it wrong.

Why the SaaS earnout dies even when the product is fine

The 21-cent number isn't bad luck. For a B2B software company specifically, the structure is built to fail in ways that have nothing to do with whether your roadmap shipped. Here is what happens to your earnout the Monday after the wire clears.

You lose the only lever that actually moves ARR. The day before close you could approve three new sales hires, greenlight a paid-acquisition test, or reprice a tier to chase net revenue retention. The day after, you're a division head. Hiring goes through a shared talent function. Marketing spend competes against the rest of the buyer's portfolio. Your earnout is measured on new ARR, but you no longer control the inputs to new ARR. That gap — full accountability for the metric, zero authority over the spend — is precisely where earnouts go to die.

"Commercially reasonable efforts" is the vaguest phrase in your purchase agreement. The buyer promises to use commercially reasonable efforts to support your targets. In practice that language lets them freeze your budget the quarter another portfolio company needs cash, and still be in contract compliance while doing it. You signed a number; they kept an option.

Integration eats the clock you're being timed against. Migrating your reps onto the acquirer's CRM, comp plan, and pricing book reliably slows sales velocity for two to three quarters — fields get re-mapped, deals stall in re-trained pipelines, your best AE spends six weeks in onboarding instead of closing. The friction is temporary. Your two-year earnout window is not; it keeps ticking straight through the slowdown. That is why a "discounted" all-cash offer is frequently the mathematically superior LOI: you are trading a paper $15M with a 21-cent realization rate for real dollars that no integration plan can quietly switch off. The narrow exception — short windows, a single un-gameable metric like gross revenue — is the whole subject of Earnouts That Actually Pay Out.

What to do with both LOIs on Monday

Two moves. First, reprice Offer B before you compare it. Take the earnout dollars, multiply by a realistic realization rate (start at the ~21-cent base case and adjust up only if the structure is genuinely clean), add the cash-at-close, and put that number next to the all-cash offer. Now you're comparing currencies that match. Most founders are stunned to find the "lower" all-cash deal wins outright — which is the actual case for taking 10-15% off a headline price to get 100% certainty. Clean exit, no two-year tail of stress, no litigation risk, no forcing yourself into an employee mindset you exited specifically to escape.

Second — if the valuation gap is genuinely too wide to close with cash and you have to take the structure — refuse the standard terms and negotiate three things into the purchase agreement, not the side letter:

- Tie it to revenue, never EBITDA. You can defend top-line ARR. You cannot defend a bottom line the buyer's controllers reshape with allocated corporate overhead, "management fees," and integration costs charged against your P&L. EBITDA earnouts in a freshly acquired software business are designed to evaporate.

- An acceleration clause that pays in full if the buyer flips the company, terminates you without cause, or materially changes the GTM motion or pricing your targets assumed.

- Budget guarantees as a signed exhibit. Specific headcount, specific marketing dollars, attached to the agreement — not a verbal assurance from the deal team that won't be in the room when budgets get cut. The full version of this list is The Acquirer's Checklist.

Your exit is about freedom, not the highest score on the LOI. All cash is freedom on Friday. An earnout is a job with a bonus the data says you probably won't collect. Price both honestly, then choose.