The practical answer

- Short answer

- International revenue isn't always an asset. Discover why 'accidental exports' create a 20% valuation discount and how to restructure global revenue for a premium exit.

- Best fit

- Industry: B2B Tech. Function: Finance & Strategy

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 20% Valuation discount applied to 'unstructured' international revenue streams in PE due diligence.

The 'Global' Growth Trap in Private Equity Due Diligence

For years, the slide in the board deck labeled "International Expansion" was a guaranteed applause line. It signaled total addressable market (TAM) expansion, product-market fit across borders, and the coveted "global platform" status. In 2026, however, that same slide often triggers a 15-20% valuation discount during Private Equity due diligence.

Why has the narrative flipped? Because in a market obsessed with Revenue Quality over Revenue Growth, unmanaged international revenue is viewed as a liability, not an asset. PE buyers are no longer impressed by a "Rest of World" revenue bucket that aggregates 12% of ARR from 40 different countries with no local support, no tax compliance, and unhedged currency exposure. This is what we call the "Accidental Exporter" trap.

When an acquirer looks at your international revenue mix, they are assessing three specific risk vectors:

- Compliance Debt: Do you have tax nexus in jurisdictions where you haven't filed? (The cost of cleaning this up often exceeds the revenue itself).

- Currency Volatility: Is your 20% growth in Japan actually a 5% contraction when adjusted for Yen volatility?

- Data Sovereignty: With 2026's stricter data residency laws, does your "global" customer base require a replatforming event to avoid GDPR or sovereignty fines?

If your international revenue looks like "accidental exports" rather than a "structured expansion," buyers will treat it as low-quality revenue. They will strip it from the valuation multiple, or worse, use the potential liability to re-trade the entire deal.

In 2026, PE buyers don't buy 'global reach.' They buy 'global compliance.' Unstructured international revenue is just a lawsuit waiting to be acquired.

The Diagnostic: Distinguishing 'Trash' Revenue from 'Premium' Revenue

Not all international revenue is created equal. In our valuation analysis for Revenue Quality Audits, we categorize international revenue into three tiers. Each tier commands a drastically different valuation multiple.

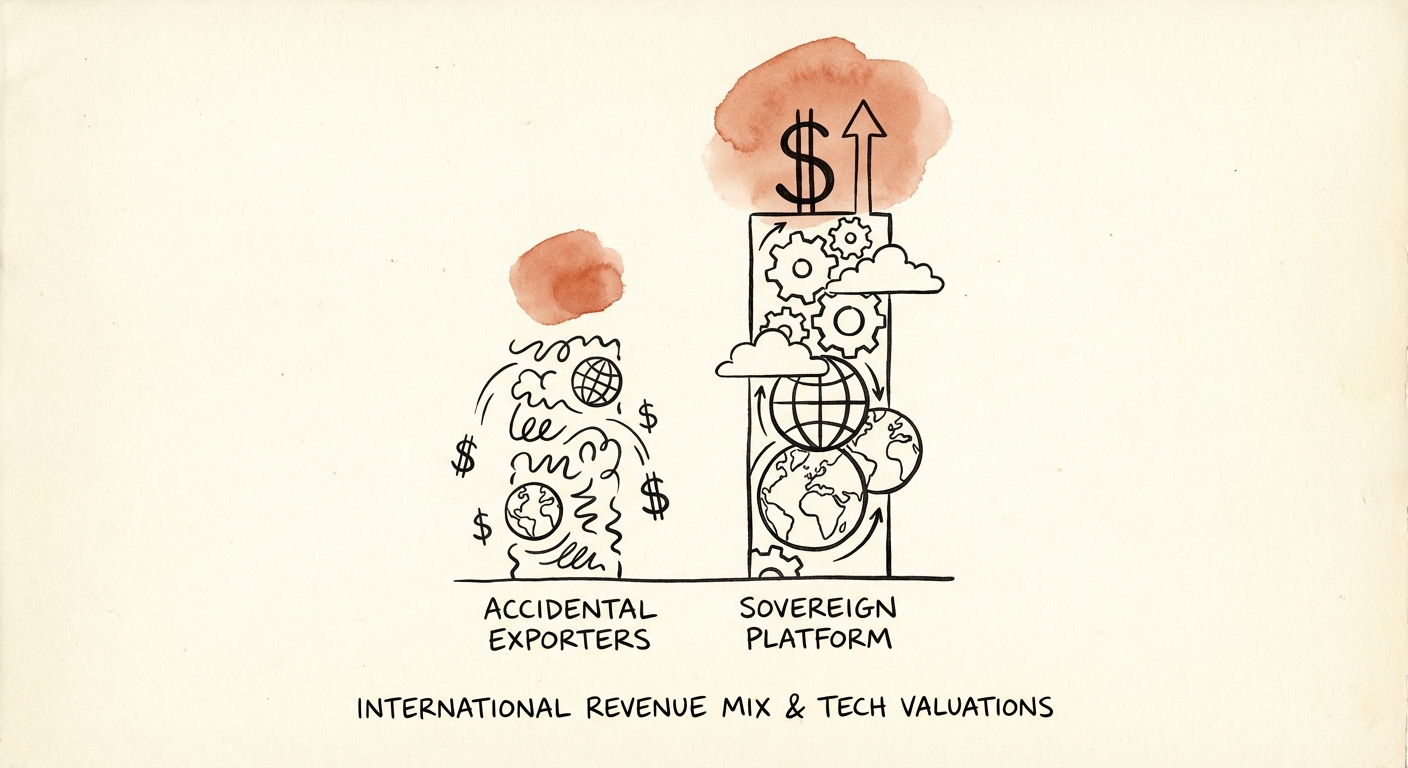

Tier 3: The 'Rest of World' Bucket (Valuation Detractor)

This is the most common scenario for Series B and C companies. You have 15% of revenue coming from non-core markets, but 0% of your operational infrastructure is dedicated to them. You have no local entity, you bill in USD (passing FX risk to the customer, increasing churn), and you rely on "catch-all" terms of service.

Valuation Impact: Buyers often apply a 20% discount to this revenue stream or exclude it entirely from the recurring revenue calculation used for the multiple. It is viewed as "at risk" of regulatory churn.

Tier 2: The 'Regional Hub' Model (Valuation Neutral)

You have structured your expansion into key hubs (e.g., London for EMEA, Singapore for APAC). You have local entities, you bill in local currencies (GBP, EUR, AUD), and you have basic FX hedging in place. You have a compliance framework that covers GDPR and local labor laws.

Valuation Impact: This revenue trades at parity with your domestic revenue. It is considered "durable," but it doesn't necessarily command a premium unless it shows superior unit economics.

Tier 1: The 'Sovereign Platform' Model (Valuation Premium)

This is the gold standard for 2026. Your international revenue isn't just compliant; it is sovereign. You have infrastructure that guarantees data residency (e.g., German data stays in Frankfurt). You have specific "In-Country" value propositions that defend against local competitors. As noted in our analysis of the Sovereign Premium, these assets are scarce.

Valuation Impact: This revenue can command a 12x-14x multiple because it represents a defensive moat. A PE firm knows they cannot easily replicate this infrastructure, making your company a strategic platform acquisition.

Fixing the Mix: How to Protect Your Exit Multiple

If you are planning an exit in the next 18-24 months, you must audit your international revenue mix now. You cannot fix tax nexus or data residency issues during the 60-day exclusivity window of a deal.

1. Exit or Partner Out of Long-Tail Markets (The 15% Rule)

If a country contributes less than 5% of your revenue but creates 50% of your compliance headaches, exit that market deliberately or move those customers to a partner model. Alternatively, move these "long-tail" customers to a Merchant of Record (MoR) model. An MoR takes on the liability of tax collection and compliance in exchange for a percentage fee. This converts "compliance debt" into a predictable "cost of goods sold," which buyers prefer.

2. Hedge the Balance Sheet, Not Just Cash Flow

PE buyers in 2026 are hyper-sensitive to FX risk. A 1% increase in exchange rate volatility can lead to a 15-20% drop in bilateral equity flows. If you are billing in foreign currencies without a hedging strategy, you are asking a financial buyer to speculate on Forex markets. Implement a systematic hedging program for any currency representing >10% of revenue.

3. The 'Data Residency' Audit

Before opening your data room, conduct a technical audit of where your international customer data lives. If you are selling to EU customers but hosting entirely in US-East-1, you are handing the buyer a "price reduction" card. Moving to a multi-region architecture (or at least having the capability documented) turns a liability into a roadmap item.

International revenue is a lever. Pulled correctly, it proves scalability. Pulled carelessly, it triggers the compliance alarms that kill deals. In 2026, the difference between a 6x exit and a 10x exit often lies in the details of where your money comes from.