The practical answer

- Short answer

- Stop applying your SaaS multiple to services revenue. Learn the 2026 Sum-of-the-Parts (SOTP) valuation framework to calculate the true value of your hybrid business.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 7.4x Median Public SaaS Revenue Multiple (Jan 2025)

The 'Blended Multiple' Hallucination

The single most expensive mistake founders make when valuing a B2B SaaS company is applying their ARR multiple to their total revenue. If you have $10M in ARR and $5M in implementation services, you do not have a $15M SaaS company. You have a hybrid asset, and sophisticated buyers will dismantle your P&L to value it as such.

In 2026, the valuation gap between pure-play SaaS and professional services has calcified. According to 2025 data from Aventis Advisors, the median private SaaS revenue multiple stands at 5.1x, while public counterparts command 7.4x. In stark contrast, professional services revenue—specifically non-recurring implementation fees—typically trades at 0.8x to 1.5x revenue or, more commonly, 8x to 12x EBITDA.

When you blend these revenue streams into a single "Revenue" line item in your deck, you invite a buyer to perform a "Sum-of-the-Parts" (SOTP) analysis that often results in a valuation 20-30% lower than your expectation. If your implementation services are operating at low margins (below 30%), they act as a valuation anchor, dragging down your high-margin ARR simply by diluting the overall gross margin profile below the critical 77% benchmark.

Implementation services can support enterprise adoption, but they hurt valuation when they become low-margin revenue disguised as software ARR.

The 30% Gross Margin Threshold

Not all service revenue is created equal. In the eyes of a Private Equity sponsor, implementation revenue falls into one of three buckets, each with a distinct impact on valuation.

1. The CAC Subsidization (Negative to 0% Margin)

If you run implementation at break-even or a loss to close deals, buyers do not view this as revenue; they view it as disguised Customer Acquisition Cost (CAC). This revenue is assigned a 0x multiple. Worse, the losses are often treated as operating expenses that reduce your EBITDA, potentially lowering the valuation of the entire business if you are being valued on profitability.

2. The 'Services Drag' (1% to 29% Margin)

Implementation services with positive but low margins are the most dangerous for valuation. They are profitable enough to stay on the P&L but inefficient enough to drag your Total Gross Margin below the 77% median benchmark for SaaS companies. 2025 data from Benchmarkit indicates that the median gross margin for professional services in SaaS companies is 30%. Falling below this line signals operational inefficiency and forces buyers to price the risk of scaling a labor-intensive delivery model.

3. The Profit Center (30%+ Margin)

When implementation margins exceed 30%, this revenue stream is treated as a legitimate, value-accretive asset. However, it is still not valued at SaaS multiples. Instead, it is valued as a distinct cash-flow generating business unit, typically receiving a multiple on its contribution margin (EBITDA). This is the only scenario where implementation services actively defend the deal value rather than eroding it.

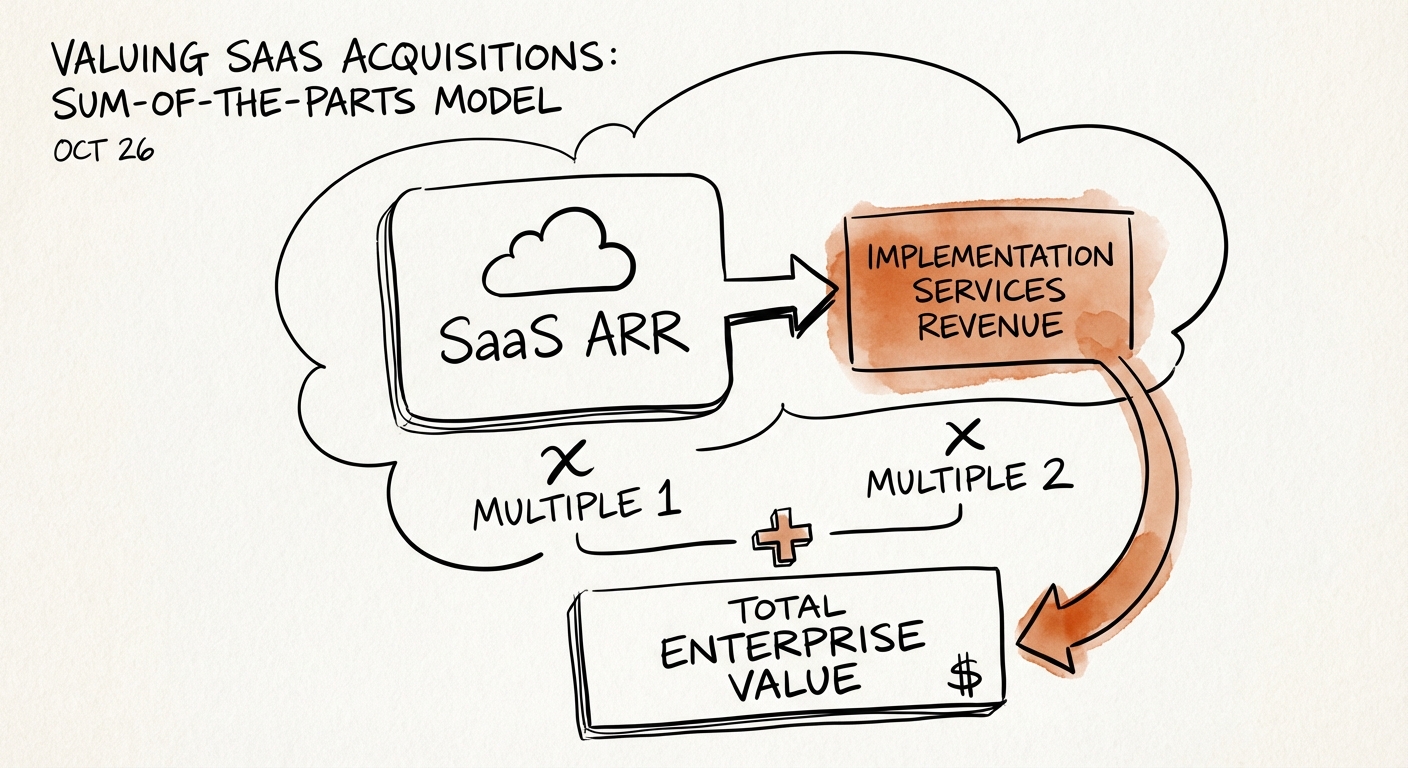

The 2026 Hybrid Valuation Framework (Sum-of-the-Parts)

To accurately forecast your exit value, you must decouple your revenue streams. We call this the "SOTP Diagnostic." Here is how a PE firm will mathematically value a hybrid company with $10M ARR and $5M Services Revenue:

The Founder's Math (The Hallucination)

$15M Total Revenue × 8x SaaS Multiple = $120M Enterprise Value

The PE Buyer's Math (The Reality)

Part A: SaaS Valuation

$10M ARR × 8x Multiple = $80M

Part B: Services Valuation

$5M Services Revenue @ 35% Margin = $1.75M EBITDA

$1.75M EBITDA × 10x Multiple = $17.5M

Total Enterprise Value: $97.5M

The difference is $22.5M—a nearly 20% "haircut" that appears during the Letter of Intent (LOI) phase. To close this gap, you must either convert implementation revenue into recurring subscription revenue (managed services) or aggressively optimize service margins to command a premium service multiple. As detailed in our ARR Multiple Calculator, shifting even $1M from "Services" to "ARR" can impact Enterprise Value by $6M to $8M.

Founders must act now to reclassify revenue. If your "implementation" includes ongoing support, break it out. Recurring support contracts can often argue for a higher multiple (4x-6x) compared to one-off projects, bridging the gap between the services valuation matrix and pure software valuations.