The practical answer

- Short answer

- A $15M ARR SaaS founder thinks they're worth $120M. The buyer's math says $45M. Here's the actual calculator PE firms run on your retention, efficiency, and growth.

- Best fit

- Industry: B2B SaaS. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 63% Valuation Premium for NRR >120%

The headline you read is not the check you'll cash

Picture a founder running a $15M ARR B2B SaaS business who is certain it's worth $120M. The math feels simple: an AI startup just raised at 50x revenue, a public cloud index is trading near 8x, so "conservatively, 10x." The money is already mentally spent.

Then a buyer runs their own number. It comes back at $45M. Same company, same revenue, same week. That $75M gap isn't a negotiation tactic — it's the difference between the multiple the press writes about and the multiple a check actually clears at.

That gap is wider in 2025 than it's been in a decade. The Centaurs — the $100M+ ARR club Bessemer tracks in its Cloud 100 benchmarks — and a handful of AI-native firms still command rich double-digit multiples. Everyone else got a reality check. The market stopped paying for "growth at all costs" and started paying for efficient growth, full stop.

Here's the number that should reset your expectations: SaaS Capital's 2025 index puts the median public SaaS multiple around 6.7x ARR — and that's for liquid, audited companies at scale. If you're private and under $50M in revenue, the liquidity discount is real and unforgiving. Unless you're growing north of 40% a year, your baseline isn't 10x. It's 3x to 5x. That's the difference between generational wealth and a disappointed cap table.

The good news: a multiple isn't a verdict handed down by the market. It's an output of a formula. And once you can see the inputs, you can engineer them.

If you're growing 18% and burning cash, you're in the death zone — not fast enough for the venture multiple, not profitable enough for the buyout one. The market has no slot for you.

The three dials a buyer turns before they make an offer

Private equity and strategic acquirers don't pluck multiples from the air. They start from a base and turn three dials — retention, efficiency, and growth — each up or down. Get all three right and you trade at 8x. Miss them and the same revenue trades at 4x. Here's what each dial is actually worth.

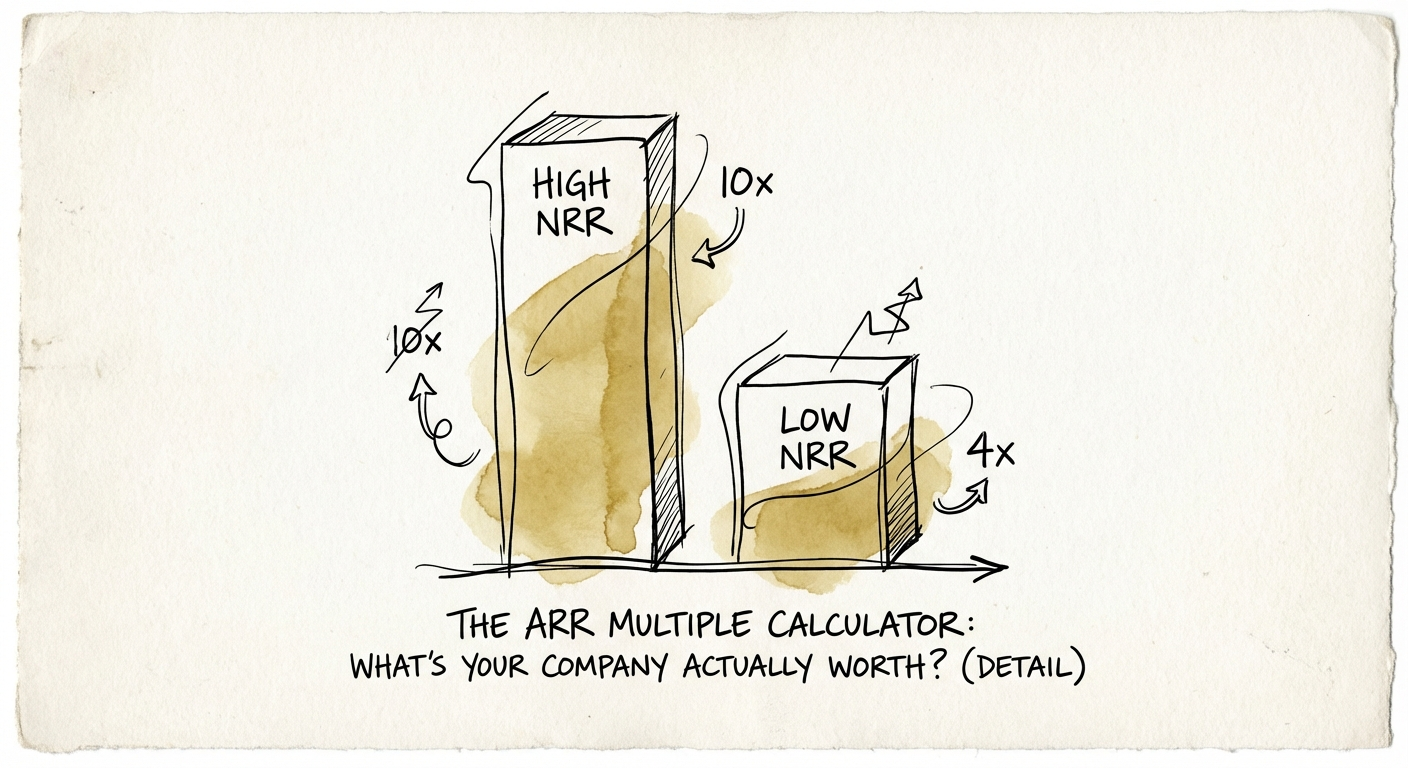

Dial 1: Net Revenue Retention — the 63% swing

Buyers don't value $1 of revenue. They value $1 of durable revenue. A dollar from a churning customer is worth a fraction of a dollar from an account that expands every year, and they price it that way. Software Equity Group's data on NRR makes the spread brutal: companies above 120% NRR carry roughly a 63% valuation premium over the median — averaging around 9.3x — while companies under 100% NRR collapse to about 3.1x. That's a 3x difference in enterprise value driven by a single retention number. If your NRR is 95%, you're not "slightly leaky." You're being priced as a distressed asset filling a bucket with a hole in it. Why 120% NRR is the metric that actually moves the number.

Dial 2: Rule of 40 — about 1.1x per ten points

In 2021 you could buy growth with cash and call it a strategy. In 2025 that same burn kills deals. Rule of 40 — growth rate plus profit margin — became the primary screen for a premium multiple. The rough conversion: every 10-point improvement in your Rule of 40 score adds roughly 1.1x to your multiple. Move from a 20 to a 50 and you've nearly tripled your exit value without adding a dollar of ARR. The catch is that almost nobody clears the bar — CloudZero's 2025 report pegs the median SaaS company's Rule of 40 score at just 12%. Crack 40 and you're instantly in the top decile of assets a buyer will see all year.

Dial 3: Growth rate — the three buckets you get sorted into

Growth still matters, but it's tiered, and the tiers are stark. Under 20% growth, you're a cash cow or a turnaround case valued on EBITDA, not revenue — 3x to 5x. Between 20% and 40%, you're a healthy grower at 5x to 7x. Above 40%, the revenue-multiple logic finally kicks in and you can reach 7x to 10x and beyond. The trap is the middle of the bottom: growing 18% while burning cash puts you in the death zone — not fast enough for the venture multiple, not profitable enough for the buyout one. The market has no slot for that company, so it discounts it from both directions at once.

Run the calculator on yourself, right now

Close the TechCrunch tab and open your own dashboard. Here's the same back-of-envelope model a buyer runs in the first meeting. Start at a base of 4x, then adjust:

- NRR: above 110%? Add 1.5x. Below 100%? Subtract 1.5x.

- Rule of 40: above 40? Add 2x. Below 10? Subtract 1x.

- Growth: above 40%? Add 2x.

Now run two real shapes. A $20M business growing 15%, with 95% NRR and -10% margins lands at 4 − 1.5 − 1 = 1.5x. That's a $30M valuation and, honestly, a company that's hard to sell at any price. A $20M business growing 35%, with 115% NRR and 15% margins (a Rule of 40 of 50) lands at 4 + 1.5 + 2 = 7.5x — a $150M valuation. Same revenue line. Five times the outcome. The entire spread lives in three operating metrics you control.

What to do Monday if you don't like your number

If the math came back ugly, you generally have 12 to 24 months to change it before you go to market. This is operational engineering, not better marketing, and the sequence matters:

Plug the bucket before you pour anything in. If NRR is under 100%, stop hiring sales reps — you can't out-acquire churn. Put the money into Customer Success and product. Here's how to tell whether your Customer Success function is actually broken.

Then pick a lane on efficiency. If you're not growing past 40%, you have to be profitable; the middle is the death zone. Audit OpEx line by line and engineer toward efficient growth. See why median firms trade at a discount on efficiency alone.

Then write it all down. When you go to market, the buyer's Quality of Earnings review will hunt for any number that depends on tribal knowledge — and re-trade you on every one they find. The cleanest path to protecting your multiple in diligence is documentation that survives questioning.

Your valuation isn't fate. It's a formula. Solve for the three variables and the exit price takes care of itself.