The practical answer

- Short answer

- In EdTech, a signed district PO isn't recognized revenue. Here's how ASC 606, the summer cash drought, and quiet district shrinkage restate ARR in diligence.

- Best fit

- Industry: EdTech. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 12-15x EBITDA Multiple for AI-Enabled EdTech

Run the July payroll test before you run the model

Pull the target's bank statements and look at the eight weeks between mid-June and mid-August. In most EdTech businesses selling to K-12 districts, that window shows collections at a near-standstill while payroll, hosting, and rent keep marching. If the company survived last summer on a line of credit instead of operating cash, you have not found a sticky SaaS asset. You have found a business that books revenue in the spring and spends it surviving until the fall.

That single observation explains why valuations in this sector spread so wide. Premium, AI-enabled platforms with genuine recognized recurring revenue clear double-digit EBITDA multiples, while content libraries and "digital classroom" tools struggle to clear single digits — a split the 2025 deal data lays out plainly (Finro, EdTech Valuation Multiples; Bolt Search, Education M&A 2025). The gap is rarely about growth rate. It is about whether the ARR on the teaser is the same ARR a Quality of Earnings team will sign off on.

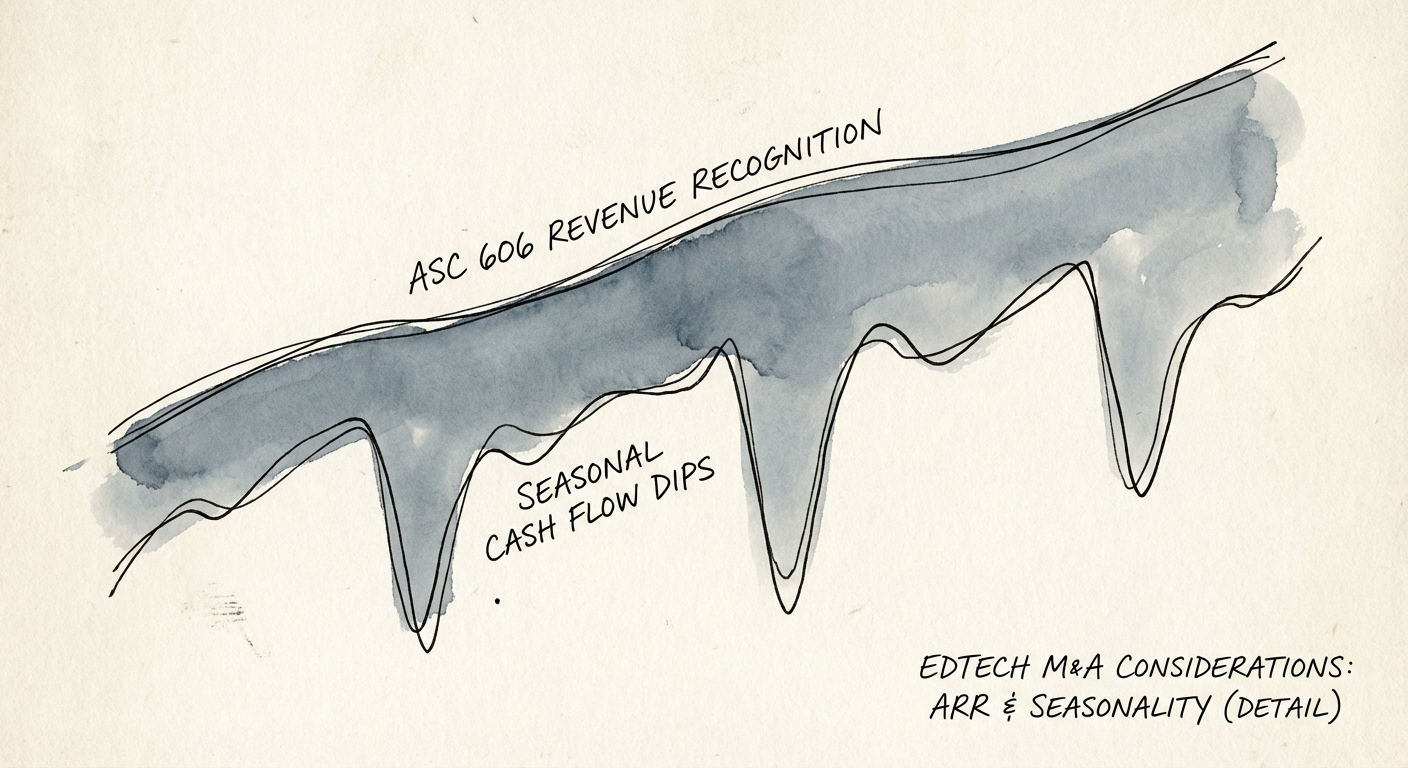

Here is where founders and their controllers consistently overstate the asset: they treat a signed district purchase order as recognized ARR. It is not. Under ASC 606, revenue follows the transfer of control, and an EdTech contract almost never delivers control evenly. Say a district signs a $50k deal in May. If $10k of that is on-site professional development delivered in August and $10k is implementation and rostering done before the school year, those are distinct performance obligations recognized when delivered — not smoothed across twelve months. Restating bookings into compliant recognized revenue is the most common way buyers walk the number down during diligence, and it is entirely defensible. We unpack the mechanics in the revenue recognition trap.

In EdTech, a signed purchase order is a promise, and in July when usage is zero and collections have frozen, you can't make payroll with promises. The diligence team prices the promise, not the press release.

Why a June 30 fiscal year hides the churn

Nearly every U.S. school district closes its books on June 30, so EdTech sales teams are trained to chase "budget flush" deals in May and June — spend it or lose it. The result is a booking spike every calendar Q2 that flatters the trailing-twelve and conveniently buries whatever happened in the three quarters before it. If you read aggregate ARR growth, you will miss the story. You have to read it on a cohort basis.

The number that matters is Net Revenue Retention by cohort, not logo retention. Districts almost never cancel outright; canceling a platform mid-year is politically painful and operationally messy. Instead they renew the logo and quietly cut the seat count, drop a module, or decline the price step-up. Logo retention reads 95% and everyone relaxes — while net dollars are bleeding. Median B2B SaaS NRR sat around 106% in 2025, and elite assets run above 120% on real site and module expansion (Userlens, B2B SaaS Retention Benchmarks). A K-12 target stuck near 95% net is contracting under cover of a healthy-looking logo number.

Then stack the bundling problem on top. A typical $50k district deal splits roughly into $30k software, $10k implementation and rostering, and $10k professional development. Smooth-method accounting books about $4,166 of MRR for twelve clean months. Compliant recognition pushes the $20k of implementation and PD into August and September, when it is actually delivered. That produces lumpy, seasonal EBITDA — and if you anchored your offer to a TTM EBITDA built on the smooth method, you are overpaying for one-time setup fees dressed up as recurring software. Worse, those adjustments often erase the working capital you assumed was there, leaving you to inject fresh equity post-close just to cover the summer. That is the trap behind adjusted EBITDA in a services acquisition.

Three checks before you sign the LOI

If you are underwriting or holding an EdTech asset, three diligence moves separate the real recurring revenue from the seasonal mirage.

Reconcile rostered seats against active logins. Pull last month's usage telemetry and compare paid seats to students who actually logged in. A district paying for 5,000 seats with 500 monthly active users is not a renewal — it is a budget-line item waiting for a board to notice. Engagement is the leading indicator: usage is what survives the next budget vote, and the dead seats are phantom revenue that vanishes at renewal.

Pressure-test the mega-district. EdTech concentration has a particular shape: lose a single large district and you lose more than the contract value — you lose the reference logo that closes the next ten deals. When one district represents more than 10% of ARR, discount the multiple accordingly and model the loss explicitly, not as a footnote. Our customer concentration thresholds guide sets the bands.

Demand a restated, season-adjusted P&L before the LOI. Require recognized revenue under ASC 606, with implementation and PD stripped out of the recurring line and the summer collection gap shown in plain view. You are buying the true recurring margin, not the spring-loaded version. The market is rewarding genuine recurring infrastructure and pricing content libraries far lower — so confirm which one you are actually holding before the wire goes out.