The practical answer

- Short answer

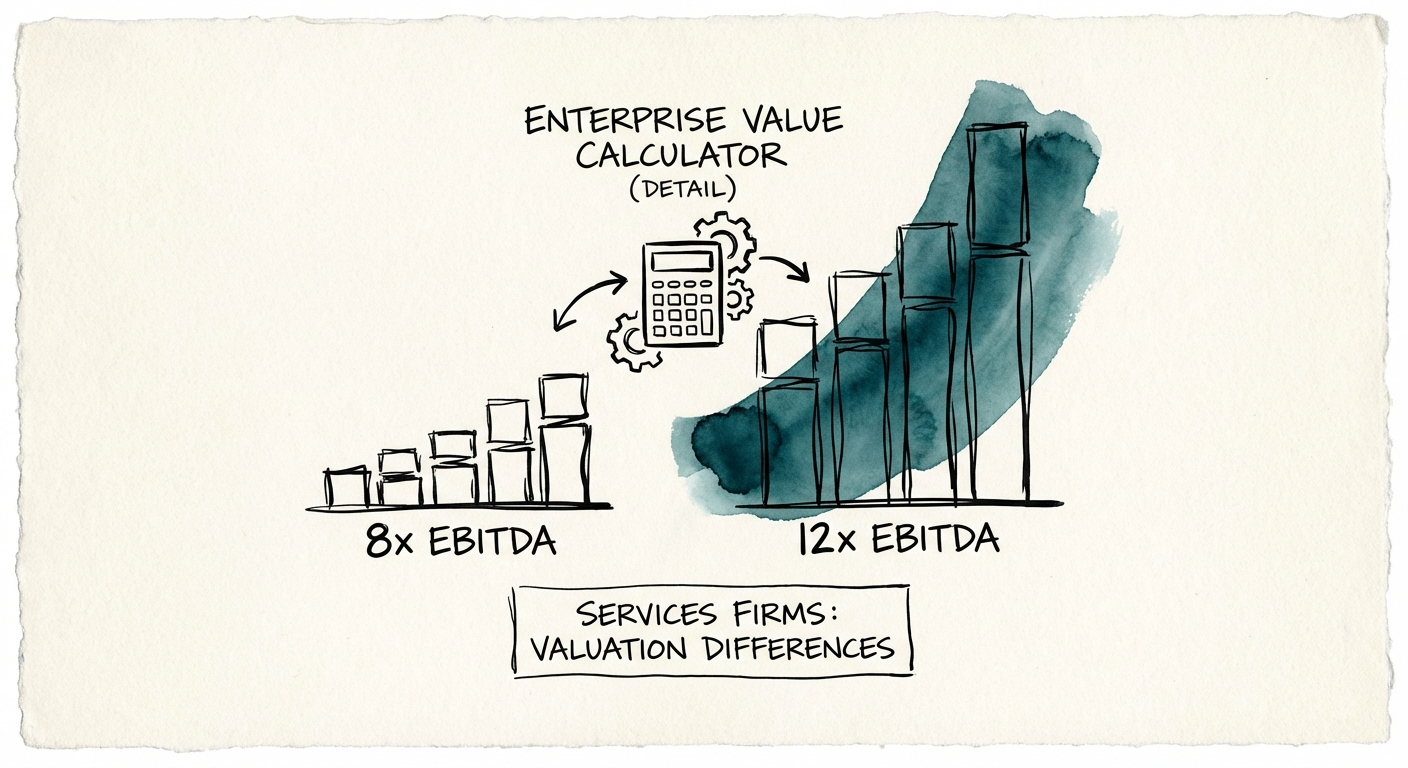

- Founders often mistake revenue multiples for valuation. Discover the 2026 Enterprise Value formula for services firms and how to move from 8x to 12x EBITDA.

- Best fit

- Industry: Professional Services. Function: Finance

- Operating path

- Exit Readiness → Operational Excellence → Transaction Advisory Services

- Key metric

- 8.8x Median EV/EBITDA Multiple for IT Services (2025)

The Napkin Math Hallucination

Every founder has done the math on a napkin. You take your annual revenue, multiply it by the valuation multiple you read about on TechCrunch (usually a SaaS company trading at 10x revenue), and stare at a life-changing number. If you are doing $10M in revenue, you assume you are sitting on a $100M asset.

Then you hire an investment banker, and the hallucination collapses. They don't look at your top line; they look at your bottom line. And they don't apply a revenue multiple; they apply an EBITDA multiple.

For a service business in 2026, the reality is stark. While SaaS firms might trade on revenue growth, professional services and IT consulting firms trade on profitability and transferability. If you are running a $10M revenue firm with industry-average margins, your enterprise value isn't $100M. It’s likely closer to $8M to $12M. And if you—the founder—are still selling 50% of the deals, you can expect 40% of that value to be locked up in a three-year earnout that you might never see.

This is the Valuation Gap. It is the difference between what you think your business is worth based on ego and effort, and what a private equity buyer thinks it is worth based on risk and cash flow. To close that gap, you need to stop calculating based on revenue and start engineering your Quality of Earnings.

You quadrupled your exit value without adding a dollar of revenue. That is the power of operational engineering over financial engineering.

The Real Enterprise Value Formula

To understand your true exit value, you must use the formula buyers actually use. It is not complex, but it is unforgiving:

Enterprise Value (EV) = (Adjusted EBITDA × Quality Multiple) - Debt + Cash

Variable 1: Adjusted EBITDA

Most founders focus on the Multiple, but the Margin is where the battle is lost. According to SPI Research's 2025 Benchmark, the average professional services firm saw EBITDA margins drop to 9.8% this year. That means a $10M firm generates just roughly $1M in EBITDA. If you are running at average efficiency, your base value is already capped.

However, 'Adjusted EBITDA' allows you to add back one-time expenses—like your personal auto lease or that failed marketing experiment. But be warned: buyers will aggressively scrutinize these add-backs. See our guide on calculating true Adjusted EBITDA to see what actually counts.

Variable 2: The Quality Multiple

This is where the "Founder Discount" lives. Market data from Aventis Advisors shows that while the median IT services multiple in 2025 is roughly 8.8x EBITDA, elite firms are trading at 13.0x or higher.

What separates an 8x firm from a 13x firm? Three factors:

- Founder Independence: If you leave for a month, does revenue drop? If yes, subtract 2 turns from your multiple.

- Revenue Recurrence: Managed services contracts trade at premium multiples; 'eat-what-you-kill' project work trades at a discount.

- Delivery Standardization: Custom, hero-led delivery scares buyers. Documented, repeatable systems attract them.

If you are a $10M firm with 10% margins ($1M EBITDA) and heavy founder dependency (6x multiple), your exit value is $6M.

If you optimize operations to reach 20% margins ($2M EBITDA) and systematize sales to command a premium multiple (12x), that same $10M revenue firm is now worth $24M. You quadrupled your exit value without adding a dollar of revenue.

Engineering Your Multiple Expansion

You cannot simply "negotiate" a higher multiple. You must build a business that demands one. The transition from a founder-led shop to a platform asset requires a specific operational overhaul.

1. Fire Yourself from Delivery

The single biggest drag on valuation is Key Person Risk. If the buyer fears the business collapses without you, they will de-risk the deal by lowering the cash-at-close. Implement the Founder Extraction Playbook immediately. Every hour you spend delivering service is an hour you are lowering your firm's multiple.

2. Fix Your Utilization

In 2025, billable utilization dropped to 68.9% industry-wide, well below the 75% target for healthy firms. This inefficiency bleeds EBITDA. A firm with 68% utilization is running a charity for its employees. A firm with 78% utilization is a cash flow engine. Tighten your resource management and scoping accuracy.

3. Productize Your Revenue

Buyers pay for predictability. Shift your mix from 100% project-based revenue to at least 30-40% recurring or re-occurring revenue. This stabilizes forecasts and proves that client retention isn't dependent on your personal Rolodex.

Your valuation is not a lottery ticket; it is a report card on your operational maturity. Stop hoping for a strategic buyer to save you with a nonsensical revenue multiple. Do the work to build a 20% EBITDA business that runs without you. That is how you turn a job into an asset.